① As of March 2024, the total number of charging infrastructure units nationwide was 9.312 million units, an increase of 59.4% over the previous year; ② Leading companies with scale advantages, technical advantages, or the ability to make parts in the whole process are expected to achieve lower cost and higher cost performance, and enjoy the growth dividends of overseas markets.

Finance Association, April 13 (Editor Wei Qi) On the 12th, the Ministry of Finance, the Ministry of Industry and Information Technology, and the Ministry of Transport issued a notice to launch pilot work to repair shortcomings in county charging and switching facilities. In 2024-2026, in accordance with the principle of “planning first, scenario guidance, scientific order, and adaptation to local conditions”, the “100 counties, thousands of stations, 10,000 piles” pilot project will be carried out to strengthen the planning and construction of NEV charging and switching facilities in key villages and towns. The central financial administration will arrange incentive funds to support pilot counties in carrying out pilot work. The provincial (autonomous region, municipality directly under the Central Government) level should give full play to its role of coordination and implement specific tasks in detail. Relevant local departments at all levels should actively introduce relevant policies on land, electricity prices, service fees, etc., and form policy synergies to effectively fill the shortcomings in public charging and switching infrastructure in rural areas, and strive to achieve “full coverage of rural and rural areas” of charging and switching infrastructure.

Since the beginning of the year, charging pile support policies have continued. At the beginning of March, the National Development and Reform Commission and the Energy Administration issued guidance on the high-quality development of distribution grids under the new situation, requiring that by 2025, the carrying capacity and flexibility of distribution networks will be significantly improved, with about 500 million kilowatts of distributed new energy and the ability to connect about 12 million charging stations. At the February 29 meeting of the State Information Office of the Ministry of Communications, Wang Gang emphasized the need to accelerate the construction of charging infrastructure systems along highways. In 2024, it is planned to add 3,000 charging stations and 5,000 charging parking spaces in service areas.

Vehicle companies are rapidly iterating on new energy products, which strongly supports market sales. The China Automobile Association expects sales of 11.5 million new energy vehicles to reach 11.5 million units in 2024, +20.0% over the same period last year. Capital Securities believes that in terms of charging piles, the country continues to promote the development of electric vehicles and the electrification of urban buses. At the same time, the overall pile cars are currently relatively low, and charging piles still have a lot of room for growth.

According to data released by the China Charging Federation, public charging stations increased by 83,000 in March 2024 compared to February 2024, and increased 48.6% year-on-year in March. As of March 2024, member organizations within the alliance have reported a total of 2.909 million public charging piles, including 1.278 million DC charging piles and 1.631 million AC charging piles. From April 2023 to March 2024, an average of 79,000 new public charging stations were added every month. As of March 2024, the total number of charging infrastructures nationwide was 9.312 million units, an increase of 59.4% over the previous year.

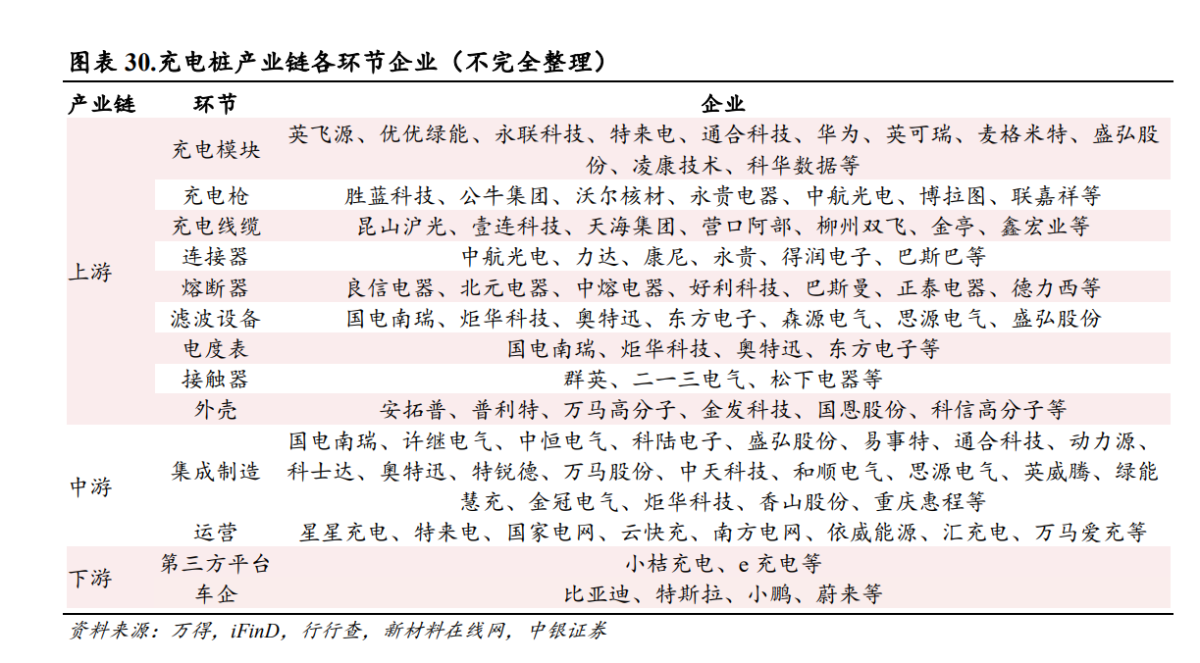

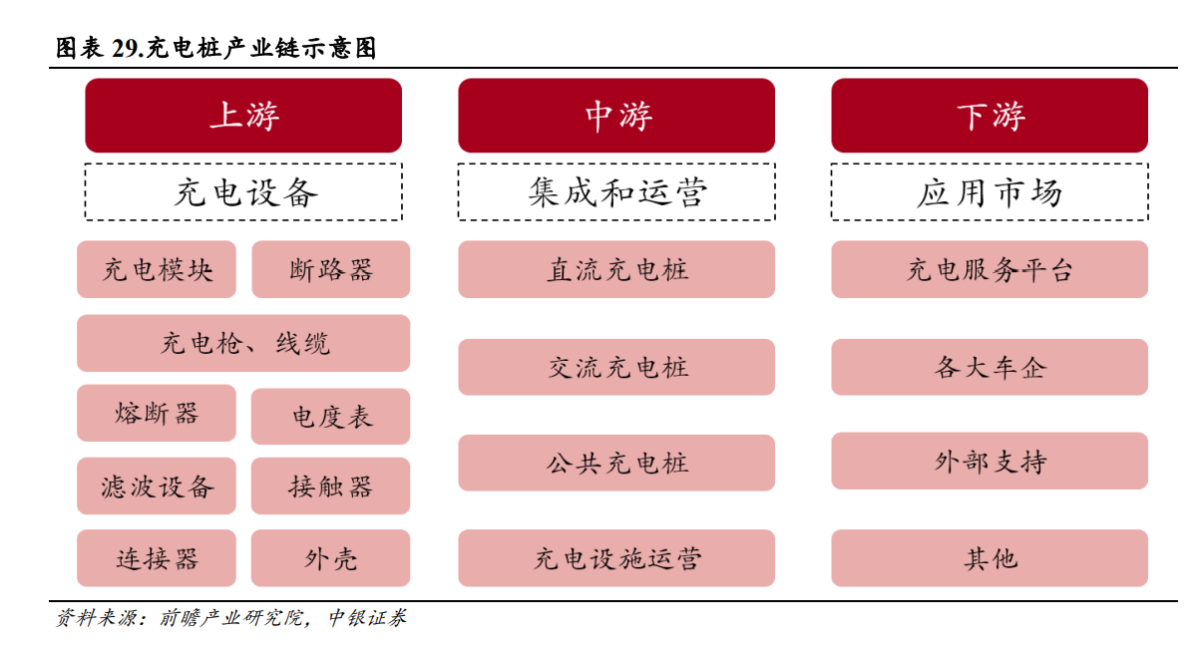

According to the different division of labor in the industry, the charging pile industry chain can be roughly divided into three links: upper, middle, and downstream. Upstream in the industrial chain are manufacturers of charging pile components, mostly standardized electrical products, such as charging modules, motors, chips, contactors, circuit breakers, housings, plug sockets, cable materials, etc.; the middle stream of the industrial chain is the integrated manufacture and operation of charging piles, responsible for the construction and operation of charging piles and charging stations, providing charging pile services, which can coordinate upstream and downstream and meet customer needs, and provide an effective and reasonable overall operation plan. Midstream construction and operation is an asset-heavy industry. Early construction requires a large amount of capital, and capital dependency is high. It also directly faces downstream consumers, so it is a core link in the industrial chain; downstream are NEV companies, including NEV and commercial vehicle manufacturers.

According to the BOC Securities Research Report, leading companies with scale advantages, technical advantages, or the ability to self-manufacture components are expected to achieve lower cost and higher cost performance and enjoy overseas market growth dividends; the module sector has a technical threshold, high power and high efficiency are the future development direction, leading companies are relatively leading in high-power technology; the Matthew effect in the operation process is remarkable. As market space opens up and economic efficiency improves, leading companies are expected to take the lead in benefiting. I recommend Yingjie Electric, Shenghe Technology, and Teruide. It is recommended to focus on Daotong Technology, Green Energy Huichong, Juhua Technology, and Xinneng Technology.

According to the BOC Securities Research Report, leading companies with scale advantages, technical advantages, or the ability to self-manufacture components are expected to achieve lower cost and higher cost performance and enjoy overseas market growth dividends; the module sector has a technical threshold, high power and high efficiency are the future development direction, leading companies are relatively leading in high-power technology; the Matthew effect in the operation process is remarkable. As market space opens up and economic efficiency improves, leading companies are expected to take the lead in benefiting. I recommend Yingjie Electric, Shenghe Technology, and Teruide. It is recommended to focus on Daotong Technology, Green Energy Huichong, Juhua Technology, and Xinneng Technology.

The Huaxi Securities Research Report believes that the development of vehicles and charging facilities complement each other and promote each other. In the future, with the increasing number of new energy vehicles and policy impetus, domestic infrastructure construction such as charging and switching is expected to continue to advance. At the same time, it is expected that the high-quality development of charging infrastructure will pay more attention to optimization in terms of rational layout, high usage efficiency, and more efficient charging time. On the one hand, it will drive demand release in key regions, and on the other hand, it will promote the update and application of technologies such as fast charging. Continued optimism: 1) On the equipment side, under the trend of increasing demand for charging piles, the equipment side such as modules and complete piles is expected to be directly driven to achieve an increase in sales. 2) On the operational side, charging operations are part of the NEV aftermarket. As demand for equipment accelerates, operators' profitability is expected to increase.

Listed companies in the upper, middle and downstream industrial chain of charging piles are shown below: