Aimeike, known as the “medical beauty”, seems to have recently faced quite a few challenges in the A-share market. Since April, its stock price has retreated nearly 15%, and its PE (TTM) has fallen to 34.67 times, setting a new low since listing. Naturally, this situation has attracted widespread attention in the market. (Data as of the close of April 9)

However, when we delved deeper into the company's recently released financial data, we saw a different picture.

According to the 2023 annual report and the forecast for the first quarter of 2024, Aimec showed a steady growth trend. In 2023, the company achieved revenue of 2,869 billion yuan, a year-on-year increase of 47.99%. At the same time, net profit to mother also reached 1,888 billion yuan, an increase of 47.08% over the previous year. This performance record set the second highest growth rate since the company went public. In the first quarter of 2024, the company expects to achieve operating income of 803 million yuan to 826 million yuan, up 27.5% to 31% year on year; net profit to mother is expected to be 510 million yuan to 534 million yuan, up 23% to 29% year on year; deducted non-net profit is expected to be 513 million yuan to 537 million yuan, up 33% to 39% year on year, and the performance is impressive.

So, in the current uncertain external environment, why did this leading company in the medical and aesthetic industry, despite holding two steady growth reports, experience a retracement in valuation? Where did the market's concerns come from? Faced with this situation, how should we view its subsequent development? These questions are definitely worth exploring and thinking about in depth.

What are the market's concerns?

Compared to the peak of the medical and aesthetic industry, which reached nearly 100 times the PE valuation, today's medical aesthetics have returned to a valuation of around 30X, and are not the “bastards” sought by the market today. However, this internal concern can be viewed from the three levels of demand-side, supply-side industry conditions, and related enterprises.

Concern 1: The external economic environment is weak, consumer confidence is insufficient, and the “luxury consumption” medical and aesthetic industry can continue to grow.

Conclusion: Medicine and beauty beta are strong, and are still in the first consumption gradient, and there is plenty of room to improve penetration.

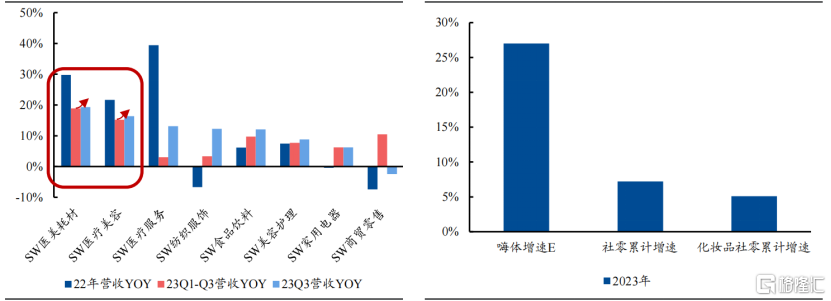

On the one hand, since 2023, medicine and beauty have shown strong resilience in the consumer sector.According to WIND data, whether looking at the growth rate in the first three quarters or the third quarter of 2023, the revenue growth rate of medical aesthetics and medical and aesthetic consumables in China was superior to other consumer circuits, and the Q3 growth rate based on a normal or even slightly higher base was slightly higher than in the first half of the year, making it more resilient.

On the other hand, the overall penetration rate of China's medical and aesthetic industry is still low, and changes in the economic environment have not changed the trend of increasing penetration rates.According to Frost & Sullivan data, the penetration rate of the medical and aesthetic population in China in 2021 was only 2.0%, far lower than other developed countries. Take Aimeike's core product as an example. As an example, it is still the only mainstream neck line removal product on the market. The “Hi Body” brand's advantages have increased, and the penetration rate continues to grow. According to the announcement, the revenue of the company's “Hi Body” mainly solution injection products increased by 29.22% in 2023, which is significantly higher than the cumulative growth rate of Social Zero in 2023 and the cumulative growth rate of Cosmetics Company Zero. According to Cinda Securities's forecast, considering the continuous increase in the penetration rate of medicine and beauty, the revenue of Hi-Sports products is expected to reach nearly 4.8 billion yuan in 2030, with a compound growth rate of 18% from 2025 to 2030.

Chart 1: The growth rate of the medical and aesthetic circuit revenue (left) and the revenue growth rate of the “Hi Sports” brand (right)

Data source: Cinda Securities, compiled by Gelonghui

Concern 2: Stricter regulations and the impact of intense upstream and downstream competition in medicine and beauty on related enterprises.

Conclusion: Under the guidance of compliance, the future industry may focus on the lead, presenting a pattern of strong players.

In recent years, domestic medical and aesthetic supervision policies have been introduced one after another to crack down on illegal medical and aesthetic institutions and the phenomenon of operating beyond scope, and strictly regulate medical and aesthetic publicity and service practices, rectify the chaos in the medical and aesthetic industry, clear up illegal agencies, and regulate the industry towards a healthier development path. In the long term, it will help the industry to further concentrate on leading compliance agencies.

Facing leading medical and aesthetic institutions, the channel advantages of Aimeike are being highlighted, showing a pattern of strong people being strong. Currently, Aimeike has more than 400 sales and marketing personnel across the country, covering more than 7,000 medical and aesthetic institutions in China. Cinda Securities pointed out that the profit structure of the medical and aesthetic industry chain is expected to begin to be reshaped, and high-quality downstream enterprises will get more profit margins, whilePlatform-based companies that are the first to build and reshape the pattern are expected to get a “bigger cake,” and Aimeike is expected to become a platform-based company that reshapes the pattern in this way.

Aimeike's backbone:

Lay out a blue ocean circuit and bet on potentially popular items

In fact, in addition to concerns about the supply and demand side of the medical and aesthetic industry, the market is also concerned about whether there are new growth points for the future development of representative companies.

Judging from the product layout, as a leading medical and aesthetic company, in addition to being able to cover current water, filling, supplementation, and support needs, the company is considering joint treatment layout through self-development or BD cooperation models to explore the Blue Ocean circuit, pointing to more star products and even star treatments with higher ceilings, and transforming into a platform-based company.

On the one hand, in order to meet the diverse needs of the market, the company continues to upgrade, iterate or expand the indications for some of the products already on the market, and continues to implement a matrix series approach:(1) Expansion of indications for Yimei One Plus One; (2) iteration of implantation line products; (3) Expansion of Bonida's indications. Among them, the company focused on Bonida, with a differentiated layout for long-term bone filling. The price of the terminal has been stable since launch, verifying its product strength, the effectiveness and forward-looking nature of its high-end positioning style. It is expected that it will be approved for Bonide's chin indications in 2024.

On the other hand, the company continues to create popular products, open up market space upward, and draw a new performance growth curve.

For example, in the botulism pipeline, the company is expected to be approved for listing in 2025, and the release of potentially major single products can be expected. The efficacy of botulinum toxin varieties has the characteristics of scarcity, large market space, high entry barriers, and a high sales ceiling for a single product. Currently, only a few institutions have obtained approval. Huons, an agent that loves Meike, has entered the registration and application stage, and is expected to usher in a broad market space through differentiated competition.

In today's popular weight loss market, Ameke's strategic layout of multiple pipelines such as deoxycholic acid and simeglutide not only covers a wide range of aesthetic and medical needs, but also satisfies the diversified demands of topical and systemic, Japanese formulations, and weekly formulations. Its rich pipeline layout is unique in the field of weight management, demonstrating the company's deep R&D strength and market insight. Looking forward to the future, these pipelines are expected to bring the second and third growth curves of the company's performance, further open up broad revenue space, and inject strong impetus into the continued growth of performance. As market potential continues to be unleashed, Aimeike is steadily moving towards the goal of being a 10 billion consumer healthcare company, showing impressive development prospects.

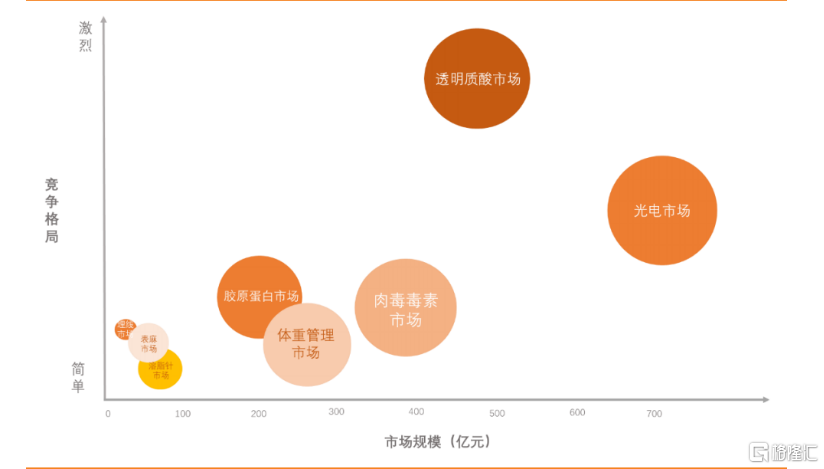

Overall, the market space for Aimeike's backers is full of imagination.According to Tianfeng Securities's forecast, in 2030, the company's optoelectronics market and hyaluronic acid market will reach 50+ billion yuan, and the collagen market, weight management market, and botulinum toxin market will also exceed 10 billion yuan.

Chart 2: Market conditions in which Aimeike products are being developed

Data source: Tianfeng Securities, compiled by Gelonghui

Note: The horizontal axis is the predicted market space for each market in 2030, and the vertical axis is the competitive pattern of each market at this stage

Summarize

Not sure, it's still a microcosm of the current environment. But it's undeniable that there are still plenty of investment opportunities to be explored.

As one of the most decisive tracks in consumption, the main theme of the future of the medical and aesthetic industry is still the increase in penetration rate. There may be differentiation among them, but leading companies are expected to use their advantages to run out of their own alpha. Aimeike is a typical example.

From the Hi-Sports series becoming a billion-dollar single product to a subsequent series of pipeline swords pointing to the 10 billion dollar market, Aimeike has shown a path of success that can be replicated. Behind this path is not only the company's management's forward-looking perception of the market, understanding of the medical and aesthetic market, and strong channel advantages, but also a reflection of its intrinsic value.

The intrinsic value of Aimeike is also projected in the details of the company's financial report. According to retrospective annual report data, thanks to good cost control and strong brand effects, Imeke deducted non-net profit at a year-on-year growth rate of more than 30% in the past 7 years, and the Q1 growth rate continued in 2024, and is expected to increase by more than 30% year-on-year. The company's net sales margin after deduction was over 60% in the past 3 years, and the performance was strong.

As mentioned earlier, Aimeike's stock price has been declining continuously since April, but at the same time, Smart Capital seems to have discovered that its price does not reflect the company's intrinsic value. According to WIND data, since April, Aimeike has received capital purchases from North China for many consecutive days, with net purchases reaching 63.14 million yuan in the past 5 days. Referring to the brokerage agency's consistent target price of 439.15 yuan, the current Aimeike has great potential for upward development and is worth watching for a long time.