4月8日,瑞银分析师Joni Teves和Elena Amoruso发布报告称,目前很难确定单一的黄金主要买盘来源,买盘较为分散,一方面黄金市场的多头头寸显著上升,但距离历史高位仍有距离,全球实物黄金ETF持续呈现出流出趋势,另一方面,央行在黄金上涨的过程中积极购入,但对多数央行来说,黄金占总储备的比例仍然很低,央行购金需求仍有继续上涨的空间。

4月8日,瑞银分析师Joni Teves和Elena Amoruso发布报告称,目前很难确定单一的黄金主要买盘来源,买盘较为分散,一方面黄金市场的多头头寸显著上升,但距离历史高位仍有距离,全球实物黄金ETF持续呈现出流出趋势,另一方面,央行在黄金上涨的过程中积极购入,但对多数央行来说,黄金占总储备的比例仍然很低,央行购金需求仍有继续上涨的空间。Source: Wall Street News

UBS believes that the sources of gold purchases are currently scattered, including hedge funds and central banks. The motivations for buying gold include: 1. The monetary policy of the Federal Reserve and the risk of inflation; 2. The geopolitical situation; and 3. Concerns about the US financial situation. In the long run, the correlation between gold, real interest rates, and the US dollar still holds true.

The price of gold continued to reach record highs. As of press release, spot gold had risen in the short term, once again reaching a record high of 2356.06 US dollars/ounce. Wall Street investment banks all pointed out in their reports that gold price trends cannot be analyzed according to previous pricing models, so who is the “mysterious force” that is driving the sharp rise in gold prices in this round?

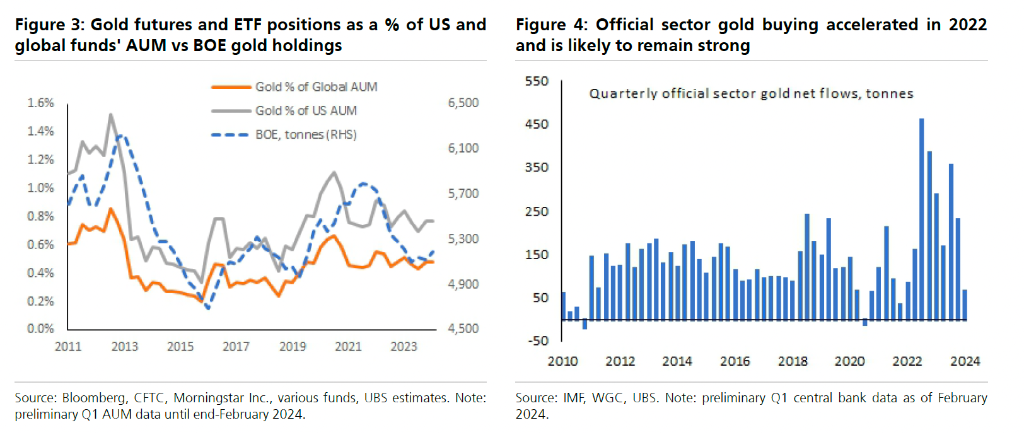

On April 8, UBS analysts Joni Teves and Elena Amoruso released a report saying that it is currently difficult to determine a single source of gold purchases. On the one hand, long positions in the gold market have risen significantly, but they are still far from historical highs. Global physical gold ETFs continue to show an outflow trend. On the other hand, central banks are actively purchasing as gold rises, but for most central banks, the share of gold in total reserves is still very low, and there is still room for central bank gold purchase demand to continue to rise.

On April 8, UBS analysts Joni Teves and Elena Amoruso released a report saying that it is currently difficult to determine a single source of gold purchases. On the one hand, long positions in the gold market have risen significantly, but they are still far from historical highs. Global physical gold ETFs continue to show an outflow trend. On the other hand, central banks are actively purchasing as gold rises, but for most central banks, the share of gold in total reserves is still very low, and there is still room for central bank gold purchase demand to continue to rise.

According to UBS analysts, investors are currently motivated to buy gold by the following three points:

1) The Federal Reserve's monetary policy and inflation risk. As long as the Fed maintains a dovish stance, the risk of rising inflation means that real interest rates may fall further, and market concerns about future inflation being high for a long time have intensified, making gold more attractive as a traditional inflation hedge.

2) The geopolitical situation has made investors avoid risks when buying gold.

3) The potential impact of the US presidential election on fiscal policy. As the election approaches, concerns about the US fiscal situation may surface, and investors are choosing to increase their gold holdings.

UBS said that the recent trend of gold completely “deviates” from the real interest rate trend, and the pricing model (including key factors to consider: the US dollar exchange rate, actual interest rate, and fluctuation indicators such as MOVE and VIX) can no longer explain the rise in gold prices.

However, UBS believes that in the long run, the correlation between gold, actual interest rates, and the US dollar still holds. The US real interest rate still represents the opportunity cost of holding gold, and the US dollar is the main currency for gold pricing, so the “derailment” between gold and macro fundamentals will not exist forever.

Who is buying the gold?

UBS indicated in the report that it is currently difficult to determine a single major source of buying. Since February, there has been a marked increase in commodity trading advisor (CTA) purchases, and the number of open gold futures contracts has increased by 24%, but the level is still only around 63% of the all-time high:

Whether we look at total speculative net positions or fund managers' net positions, these positions are only 57% and 50% of their all-time highs, respectively. At the same time, gold ETFs are still declining, showing a net outflow trend. There is no active strategy for recommending the allocation of gold in the private wealth management sector, and quite a few investors have little exposure to gold.

UBS notes that the above information has several important implications. First, the data shows that gold purchases are scattered rather than concentrated in a certain market segment or a small number of participants. Many investors who are optimistic about gold have not actually opened positions since the fourth quarter of last year, and many have wait-and-see attitudes about gold and await a correction in gold prices.

Second, there may be market participants who buy gold in ways that are difficult to track with public data, such as OTC transactions or physical transactions. Third, a broad and scattered investor base means the market is more resilient, which in turn helps keep the price of gold at a higher level.

UBS stressed that the central bank's demand for gold cannot be ignored. The specific purchase scale will be announced in a few months, but global central banks have had strong demand for gold purchases over the past 13 years, with gold purchases accounting for 27% in the past two years:

Purchases in 2022 and 2023 account for about 30% of the mine's supply, which is higher than the average of about 15% in the previous 10 years. Despite this, we believe there is room for this trend to continue to rise. For many central banks, gold's share of total reserves is still very low.

Wall Street saw this earlier. UBS pointed out in a report released earlier that the current statistics showed that the central bank's net purchase volume from January to February was about 65 tons:

Among them, data released by China's State Administration of Foreign Exchange shows that in March, China purchased about 5 tons of gold, bringing the total purchase volume in the first quarter to 27 tons. China has been increasing its gold reserves for 17 consecutive months and is currently the largest buyer among central banks, followed by Turkey and India.

Why buy now

UBS pointed out that investors have increased their gold positions for several reasons. First, some investors expect real interest rates in the US to fall as the Federal Reserve begins a cycle of interest rate cuts. If the Federal Reserve maintains a dovish stance, the risk of rising inflation indicates that real interest rates may fall further, which will be more beneficial to gold. Supply-driven increases in oil and commodity prices are likely to exacerbate these concerns.

Second, the global geopolitical situation has increased the reasons investors might want to hold gold. Since there are so many variables in geopolitics, it seems reasonable to use gold as a hedge against any potential escalation of geopolitical risks in this environment.

Finally, among the many elections held this year, the November US presidential election is likely to receive more and more attention from gold market participants. As investors consider the potential impact on fiscal policy, concerns about America's rising debt and budget deficits are likely to surface.

UBS believes that any of these factors may not seem sufficient in themselves to be a sufficient reason, but taken together, they provide quite sufficient reasons for investors to increase their gold holdings.

Will the “derailment” between real interest rates and the US dollar persist for a long time

UBS previously pointed out that, as shown in the chart below, the model results show that the recent gold trend completely “deviates” from the real interest rate trend. When real interest rates have declined since this year, the beta coefficient between the price of gold and 10-year US inflation-protected treasury bonds (TIPS, real interest rates) is negative; however, when real interest rates rise, this coefficient turns positive, which contradicts the traditional understanding (that is, the rise in real interest rates causes the price of gold to fall).

According to UBS, the residual analysis shows that the model cannot explain most of the recent rise in gold prices. In addition to traditional influencing factors such as the US dollar exchange rate, real interest rates, and uncertain indicators, there may be other important driving forces that have driven the recent rise in gold prices.

UBS notes that the relationship between gold and macro variables is not permanently broken. As can be seen from a re-examination of the gold pricing model, the sensitivity of gold to actual yield has declined in the past few years compared to historical levels. When real interest rates are high (such as now and in the early 2000s), gold is often less sensitive to it.

UBS believes that these relationships still hold in the long run. The real interest rate in the US represents the opportunity cost of holding gold, and the US dollar is the main currency for gold pricing, so there is an inherent negative correlation.

Editor/jayden