The S&P Dow closed down slightly, and the NASDAQ rose slightly; among the “Seven Sisters” of technology, only Tesla closed up sharply, rising nearly 5%; Meta fell to a record high level; the chip stock index went up 2 times, and TSMC's US stock closed up 1%, but Nvidia fell 1%. China's stock index stopped falling three times in a row. Ideal Auto rose nearly 5%, and Baidu fell more than 3%. The 10-year US Treasury yield hit a four-month high of 4.5% during the intraday period.

The US dollar index retreated; the yen's intraday decline pushed to its low level since 1990. The offshore renminbi rose more than 100 points in the intraday period, close to breaking 7.24. At one point, Bitcoin rallied by nearly $4,000 and rushed to $73,000.

Crude oil ended six consecutive gains and fell to a five-month high. Gold hit a record intraday high for 7 days. Luntong rebounded to a two-year high, and Lunxi rose nearly 3.7% to a 14-month high.

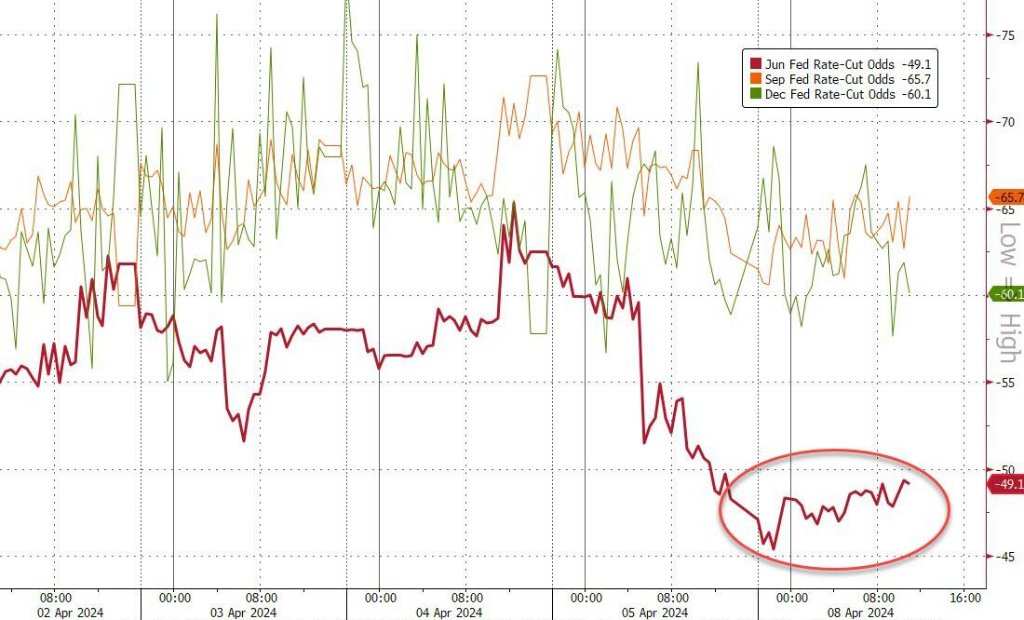

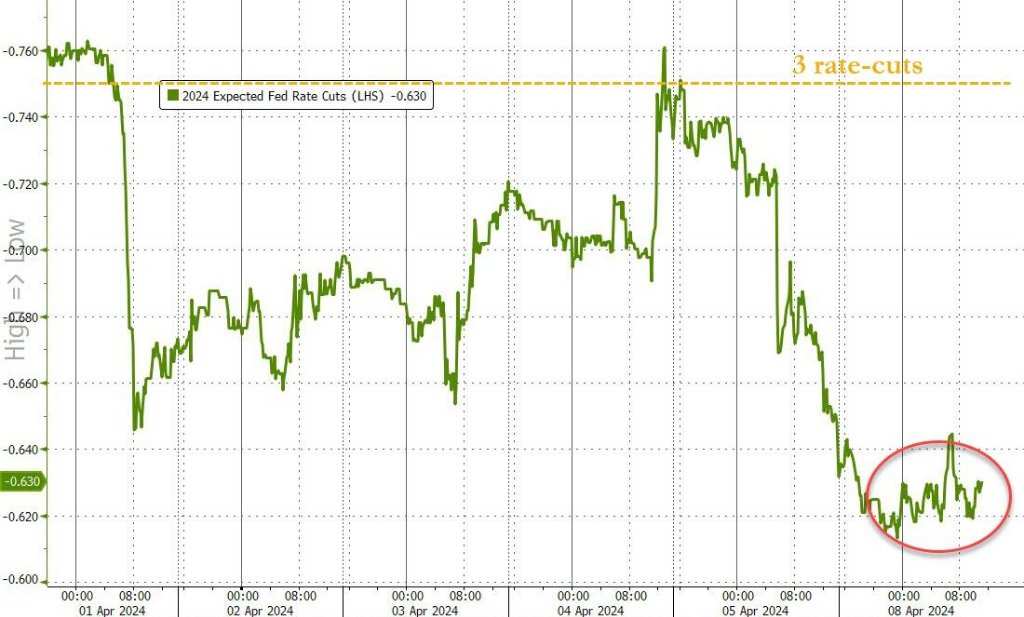

Data released last week, such as strong growth in non-farm payrolls that exceeded expectations, have repeatedly hit the market's expectations of interest rate cuts. In Monday's intraday, the price of the swap contract showed that investors expect the Federal Reserve to cut interest rates by a total of about 60 basis points this year, which means they are most likely to cut interest rates twice before starting to cut interest rates until September. Futures market pricing shows that investors expect the probability of cutting interest rates in June to fall below 50%. The price of US Treasury bonds fell further, and the yield on US bonds with various maturities was high since the end of November last year.

On Monday, the benchmark 10-year US Treasury yield not only refreshed the four-month high set last week, but also boosted 4.50%. Some investors believe 4.5% is the main threshold that may determine whether yields will return to last year's high. Many Wall Streeters expect the 10-year US Treasury yield to rise above 4.5% in the near future. Once it reaches 5%, it is likely to trigger an adjustment in US stocks. The CPI to be released this Wednesday will determine whether this yield will remain within 4%-4.5% or rise sharply.

After the opening of the US stock market, US bond yields recovered some of the gains, and the downward pressure on US stocks declined. Major US stock indexes all turned down during the intraday period and were unable to maintain the momentum of last Friday's rebound. Most of the tech giants fell. Nvidia, which rebounded last Friday, retreated, and dragged the chip stock index back down for a while. And after CEO Musk announced that the autonomous taxi RoboTaxi will be released on August 8, Tesla rebounded strongly.

In the foreign exchange market, investors are waiting for the CPI announcement. The US dollar index turned down intraday. The “one-day trip” rebounded after the US employment report was released last Friday. Various non-US currencies such as the RMB rose, and the yen was still falling. Japan announced on Monday that real wages for February fell 1.3% year on year, falling 23 months in a row, setting a record for the longest continuous decline, reflecting the pressure on consumer spending due to rising prices. The yen once fell below 151.90 against the US dollar, extremely close to the low since 1990 set more than a week ago. The next test may trigger the Japanese government to interfere in the foreign exchange market at 152.00.

However, the rebound of cryptocurrencies, which declined last week, was more volatile than major currencies. Bitcoin reached the $70,000 mark and once rose above $72,700, close to the historical intraday high set by rising above $73,700 on March 14. Some commentators mentioned that the fourth halving in Bitcoin history is expected to arrive around the 20th of this month. The halving of Bitcoin mining block rewards designed to limit supply is seen as a benefit that may stimulate the rise in currency prices and fuel bull market expectations.

Among commodities, gold continued its trend of hitting record highs in the market for a week. According to commentators, in addition to the tense geographical situation in the Middle East and other regions, demand from central banks around the world is also driving gold prices to continue to rise. China announced over the weekend that March gold reserves have increased for 17 consecutive months, and India, Turkey, Kazakhstan, and some Eastern European countries are also buying gold this year.

However, international crude oil, which has continued to rise in the last week, has left a five-month high. Crude oil fell by more than 2% in the intraday period, then narrowed most of its declines. Investors are concerned about the risks of fuel supply in the Middle East. Market participants assessed that Israel's withdrawal of troops from the southern Gaza Strip over the weekend was a step towards easing the conflict between Palestine and Israel. There are reports that Israel and Hamas have sent a delegation to Cairo to conduct cease-fire negotiations, but there are also reports that no progress has been made in the negotiations. According to CCTV reports, Israeli Prime Minister Binyamin Netanyahu said on Monday evening local time that the Israeli army would enter Rafah, the southernmost tip of the Gaza Strip, to launch an attack.

The S&P Dow fell slightly among the “Seven Sisters” of technology, only Tesla closed up two consecutive gains, but Nvidia fell back and the China General Stock Index rebounded

The three major US stock indexes collectively opened higher and turned down several times during the session. The Dow Jones Industrial Average, which opened more than 12 points higher, rose nearly 110 points at the beginning of the session, turned down half an hour after opening, then turned down at the end of early trading. It fell more than 46 points at the beginning of midday trading, then turned higher in midday trading. The S&P 500 index, which opened more than 0.1% higher, quickly turned down at the beginning of the session. After turning up in early trading, it rose nearly 0.3% to a new high. At the end of early trading, it turned down and fell by more than 0.1%. It turned slightly higher in midday trading, and both the Dow fell again at the end of the session. The Nasdaq Composite Index, which opened more than 0.2% higher, turned down in the short term at the beginning of the session. It rose nearly 0.5% when it hit a new high in early trading. After turning down at the beginning of the midday session, it fell nearly 0.2%, and turned slightly higher in midday trading.

In the end, among the three major indices, only the NASDAQ closed higher for two consecutive trading days, with an increase of 0.03%, far less than the 1.24% increase last Friday, which reached 16253.96 points. S&P closed down 0.04% to 5202.39 points, unable to continue to break away from the closing low since March 15 caused by last Thursday's fall. The Dow closed down 11.24 points, or 0.03%, to 38892.80 points. It was unable to continue to bid farewell to the closing low since March 5, when it fell for four days in a row last Thursday.

The small-cap stock index Russell 2000, which is mainly value stocks, closed up 0.5%, outperforming the market. After falling back to its closing low since March 19 last Thursday, it continued to rise for two days. The Nasdaq 100 Index, which focuses on technology stocks, closed down 0.05%, and the Nasdaq Technology Market Capitalization Weighted Index (NDXTMC), which measures the performance of technology constituents in the NASDAQ 100 Index, closed down 0.16%, underperforming the market. They all fell back last Friday after leaving the closing low since March 15.

Among the major sectors of the S&P 500, six closed down on Monday. Last week, the best-performing energy sector fell by more than 0.6%, healthcare fell nearly 0.4%, Nvidia's IT fell more than 0.3%, industrial and essential consumer goods fell by about 0.2%, and communications services fell slightly. Among the five sectors that closed higher, interest-rate sensitive real estate rose by more than 0.8%, Tesla's non-essential consumer goods rose by nearly 0.8%, utilities rose by more than 0.6%, finance rose by nearly 0.4%, and materials rose slightly.

Including Microsoft, Apple, Nvidia, Google's parent company Alphabet, Amazon, Facebook's parent company Meta, and Tesla, the tech giants “Seven Sisters” had mixed ups and downs in the intraday period; only Tesla closed higher. Tesla, which fell back to its low level since March 15 last Friday, rebounded, rising more than 5% in early trading and closing 4.9%, reversing the 3.6% decline on Friday.

Among the six major FAANMG technology stocks, Alphabet opened high, rising more than 1% in early trading, closing 1.4%, and rising for two consecutive days after falling back to a one-week low last Thursday; Amazon, which had a high opening of 1.2% at the beginning of the session, then regained most of its gains and closed up 0.07%, breaking the closing high since July 2021 caused by last Friday's rebound; while Meta, which had a record high of closing for five days last Friday, turned down 1.5% at the beginning and closed down 1.5%; Microsoft's early trading session, which rebounded 1.8% last Friday, opened and closed down 1.5%; It turned down again, closing down 0.2%, and did not continue to break away from the 3 that was refreshed last Thursday Closed at a low level since January 18th; Apple, which rebounded last Friday, closed down nearly 0.7%, breaking the low since October 27, 2023 set last Thursday; Netflix, which rebounded last Friday to a high level since November 2021, initially turned down and closed down 1.2%.

Chip stocks, which rebounded last Friday, continued to rise slightly overall. The high-opening Philadelphia Semiconductor Index and semiconductor industry ETF SOXX turned down in the short term at the beginning of the session. They rose more than 1% in early trading and briefly turned down again in midday trading, closing up more than 0.1% and nearly 0.3% respectively, continuing to break away from the closing low since March 19, which fell about 3% last Thursday. Among chip stocks, Nvidia rose more than 0.9% at the beginning of the session, then quickly turned down more than 1%. At the beginning of the afternoon session, it fell more than 1.5% and closed down about 1%; AMD, which fell by more than 2% in early trading, turned down slightly in early trading and fell 0.3%; Intel closed down 1.9%; Micron Technology, which rose nearly 5% at the beginning of the session, turned down 0.5% in midday trading; and the media claimed that after receiving a total of 11.6 billion US dollars in funding and loan funding from the US government to build a chip factory in the US, TSMC US stocks rose nearly 3.3% in early trading 1%; Arm, which turned upward in early trading, closed up more than 3%; Qualcomm closed up more than 1%.

AI concept stocks generally declined. At the close, SoundHound.ai (SOUN) fell more than 3%, ultra-micro computers (SMCI) and BigBear.ai (BBAI) fell more than 2%, Astera Labs (ALAB), known as “Little Nvidia,” which sells data center interconnect chips, fell about 2%, C3.ai (AI) fell nearly 0.8%, Oracle (ORCL) fell more than 0.4%, Adobe (ADBE) fell nearly 0.2%, and Palantir (PLTR) rose nearly 0.2%.

Popular Chinese securities had mixed ups and downs. The high-opening Nasdaq Golden Dragon China Index (HXC) rose more than 0.8% in early trading and turned down in the short term in midday trading, closing up less than 0.1%, stopping three days of continuous decline. KWEB, a Chinese general ETF, closed up nearly 0.4%, while CQQQ closed down more than 0.4%. Among the new car builders, Ideal Auto rose 4.8% at the close, while NIO Auto, which had risen nearly 2% in early trading, fell by nearly 0.5% at the end of the session. Xiaopeng Motors, which had fallen nearly 3% in early trading, fell more than 0.1 percent, and Xiaomi Fan, which had fallen at the beginning of the session, fell 0.2%. Among individual stocks, Station B rose nearly 2% at the close, Tencent fan rose nearly 0.3%, NetEase rose nearly 0.2%, Alibaba rose less than 0.1%, while Baidu fell more than 3%, JD fell 0.3%, and Pinduoduo fell 0.2%.

The bank stock index rose sharply, outperforming the market. The overall banking index KBW Bank Index (BKX) closed up nearly 1.3%, rising for two consecutive days; the regional banking index KBW Nasdaq Regional Banking Index (KRX) closed up 1.5% for three consecutive days. The regional bank stock ETF SPDR S&P Regional Bank ETF (KRE) closed 1.7%, rising for two consecutive days, all breaking new highs since April 1.

Among individual stocks with high volatility, cloud computing service provider Fastly (FSLY) closed 7.8% after being upgraded by Piper Sandler, believing that its strong valuation and stable fundamentals brought attractive risk/return biases; after J.P. Morgan upgraded the rating to increase holdings and thought investors should bottom up, GE Vernova (GEV), an energy company spun off by General Electric, rose more than 6% and closed up 5.9% in the intraday market; Jefferies upgraded the rating from neutral to buy, and believed that its valuation was in the commodity sector After the appeal, Latin American lithium producer Sociedad Quimica y Minera (SQM) rose nearly 6% in the intraday period and closed up 4.6%.

In terms of European stocks, Germany announced on Monday that the February factory output increased 2.1% month-on-month, and the year-on-year decline did not expand and narrow to 4.9% as expected. Commentary said the data raised hopes that the German economy did not shrink again in the first quarter. Data from Germany, the largest economy in the Eurozone, is improving, supporting the rebound of pan-European stock indexes, which stopped two consecutive gains last Friday. The European Stoxx 600 index evened out about half of last Friday's decline, breaking out of its closing low since March 20, which was refreshed last Friday. Most of the major European countries' stock indexes rose. German, French and British stocks, which fell last Friday, and Italian stocks, which fell for two days, both rebounded, but none of them were able to fix last Friday's decline. The Spanish stock index fell slightly, falling for 2 days in a row.

Among various sectors, higher copper prices drove the basic resources of mining stocks to close by nearly 2%; the automotive sector rose by more than 1.3%, and the industry rose by more than 0.8%. Among individual stocks, after Citi raised the rating from neutral to buying, German fashion e-commerce company Zalando surged 7.4%, leading the stock share of Stoke 600; after the media said Motive Partners considered an offer, fund distribution company Allfunds rose 5.3%; and after Warner Music Group said it would not make a takeover offer, French digital music company Believe fell 9.2%.

The 10-year US Treasury yield hit a four-month high of 4.5% in the intraday test

The yield on the 10-year benchmark treasury bond rose above 4.46% before the US stock market. It rose more than 6 basis points during the day, and later recovered most of the gains. At the beginning of the market, the US stock market fell 4.41% to a new low, taking back almost all of the intraday gains. It was about 4.42% at the end of the bond market, rising about 2 basis points during the day, rising for 2 consecutive trading days.

The 2-year US Treasury yield, which is more sensitive to interest rate prospects, rose 4.79% to 4.80% before the US stock market, breaking more than 4 basis points during the day. The US stock market fell 4.76% to a new daily low, taking back most of the intraday increase. By the end of the bond market, it was about 4.79%, rising about 4 basis points during the day, and rising for 2 consecutive days after three consecutive days of falling.

The dollar index fell back and the yen forced Bitcoin to rise to a low level since 1990, once rising by nearly $4,000 and rushing towards $73,000

The ICE dollar index (DXY), which tracks the exchange rate of the dollar against a basket of six major currencies, including the euro, rose above 104.40 in early Asian trading and rose more than 0.1% during the day. European stocks both hit 104.40 before and during the day. US stocks maintained a decline after turning down before the market. US stocks fell below the 104.10 refresh day low in midday trading and fell close to 0.2% during the day, beginning to approach the low of the market since March 21, when it was refreshed at 103.9215 last Thursday.

By the close of the US stock market on Monday, the US dollar index was above 104.10, falling more than 0.1% during the day, falling back after rebounding last Friday and falling on the fourth day in the last five trading days; the Bloomberg US dollar spot index, which tracks the exchange rate of the US dollar against ten other currencies, fell more than 0.1%, falling back to the same low level since March 20 after closing last Friday.

Among non-US currencies, the yen fell further after falling last Friday. According to the low level since 1990, the US dollar rose above 151.90 against the US stock market, extremely close to the high level since July 1990 set at 152.00 on March 28. It rose more than 0.2% during the day, and US stocks closed above 151.80; EUR/USD rose above 1.0860 at midday trading. It rose nearly 0.3% during the day, and began to rise close to the high level since March 21, which was refreshed at 1.0880 last Thursday. US stocks were slightly below 1.1.80's closing time. 0860; GBP/USD US stocks rose above 1.2660 in midday trading and rose more than 0.2% during the day. They began to approach the high level since March 21, when they rose above 1.2680 last Thursday. US stocks were above 1.2650 at the close.

The offshore renminbi (CNH) had a new daily low of 7.2549 against the US dollar in early Asian trading. US stocks continued to rise after rising before the market. US stocks rose to 7.2410 in midday trading, close to rising to the high level since March 26, when 7.2401 was refreshed last Friday, and rebounded 138 points from the daily low. At 4:59 Beijing time on April 9, the offshore RMB was 7.2422 yuan against the US dollar, up 56 points from the end of the New York session last Friday. It has been rising for two consecutive days. It has risen on the fourth day in the last five trading days.

Bitcoin (BTC) hit the pre-market mark of 70,000 US dollars. European stocks rose above 71,000 US dollars in early trading, and US stocks rose above 72,700 US dollars before the market, breaking the intraday high since rising to a record high of $73,700 on March 14, rising nearly 4,000 US dollars, or nearly 6% from the intraday low below $69,000 in early Asian trading. US stocks initially fell below $72,000. US stocks were above $71,700 in the last 24 hours.

Crude oil ended six consecutive gains and fell to a five-month high

International crude oil futures generally maintained a downward trend throughout Monday. At a new intraday low in the Asian market, US WTI crude oil fell below 84.70 US dollars and fell nearly 2.6% during the day. Brent crude oil fell below 88.80 US dollars, falling more than 2.6% during the day. Later, the decline narrowed. US oil rose in the short term at the beginning of the US market.

In the end, crude oil fell back to its five-month high after five consecutive days of harvesting, and closed down for the first time in the last seven trading days. WTI crude oil futures for May closed down $0.48, or 0.55%, to $86.43 per barrel; Brent crude oil futures for June closed down $0.79, or 0.87%, to $90.38, and both declined after breaking the monthly contract closing high since October 20, 2023 for two consecutive days.

US gasoline and natural gas futures continued to rise and fall with mixed ups and downs. NYMEX's May gasoline futures closed down about 1.4% to $2.7486 per gallon, continuing to fall from the high level since August 2023, which was refreshed last Thursday; NYMEX's May natural gas futures closed up 3.31% to $1.844 per million British thermal units, rising for two consecutive days, approaching the high level since the March 6 report of $1.929, which was refreshed last Tuesday.

Luntong rebounded to a two-year high, Lunxi rose nearly 3.7%, and gold hit a record intraday high for 7 days

London basic metals futures collectively closed higher on Monday. Renxi, which led the rise, rose nearly 3.7%. For the first time since the end of January last year, it closed above 29,800 US dollars, rising for five consecutive days. Lun Al and Lun Ni have been rising for six consecutive days. Lun Aluminum has hit new highs since late February last year for 4 consecutive days, and Lunn Nickel hit new highs in three weeks. Luntong, lun zinc, and lun lead, which fell last Friday, rebounded. Luntong broke the closing high since June 2022 set last Thursday. Lunzinc hit a new high since May last year, and lun lead hit a new high of more than three weeks.

New York gold futures reached a low of 2321.7 US dollars on the new day of early trading in the Asian market, falling about 1% during the day. After the Asian market turned up, it rose to 2372.5 US dollars, and rose nearly 1.2% during the day. Since then, overall gains have been maintained. European stocks and US stocks have declined slightly in the intraday period.

Spot gold rose from an intraday low of nearly $2,300 to nearly $2,344 in early Asian trading. It rose about 1% during the day, and futures both hit record highs for seven consecutive trading days, and European stocks fell below $2,340 intraday.

In the end, futures and spot gold set new closing record highs for two consecutive trading days and on the 8th of the last nine trading days.

At the end of the US stock market, COMEX's June gold futures were reported at $2357.6, up 0.52% during the day. By the close of the US stock market, spot gold was slightly below $2,340, up nearly 0.4% during the day.

Editor/Jeffrey