Does Japan want another financial attack on Pearl Harbor?

Since the Bank of Japan withdrew from negative interest rates and the YCC policy on March 19, the yen has once again approached a 34-year low — the key 152 mark, and market predictions for the Bank of Japan's further entry into the market to intervene are heating up.

At the same time, commodities continued to perform strongly. The number of non-farm payrolls in the US surged by 300,000 in March, and interest rate cuts in the first half of the year may be hopeless.

Following the current weakening of the yen, Japan's Minister of Finance, Shunichi Suzuki, issued a strong warning that the authorities might take “decisive measures - this is very rare in previous Japanese official statements, and only occurred at the end of October 2022.

In November of last year and October 2022, the exchange rate of the yen against the US dollar reached around 152 points twice.

Say goodbye to negative interest rates, why did Japan raise interest rates for the first time?

Since 2016, due to the existence of negative interest rates and the support of the YCC policy, the yen has always been the most ideal currency for arbitrage transactions in the world. The core of arbitrage trading is “volume compensation”, with sufficient capital, as long as there is a certain stable interest spread. The reason why the yen has been the protagonist of arbitrage trading for many years depends on the one hand on extremely low borrowing costs, and on the other hand, on long-term monetary policy stability. Over the past few decades, the market's consistent expectations of the Bank of Japan's monetary easing have been very stable.

Before the Federal Reserve raised interest rates, the ability of Japanese companies to generate foreign exchange from exports could still offset the shorting pressure on the yen. After the European and American central banks, led by the Federal Reserve, began a wave of rapid interest rate hikes in 2022, the Bank of Japan still insisted on a negative interest rate policy. In 2022, then-Bank of Japan Governor Kuroda repeatedly stated that the Bank of Japan will continue to maintain an easing policy until inflation stabilizes at the target level of 2%.

But now, once the foreign exchange is converted to yen, it is not enough to offset the impact of the depreciation of the yen. Based on the BIS actual effective exchange rate index, the yen depreciated all the way to the lowest level since statistics were available after the COVID-19 pandemic. Compared with the depreciation of nearly 30% before the pandemic, the purchasing power of the yen declined significantly.

On the one hand, Japan's high dependence on external energy, particularly restrictions on nuclear power after the Fukushima nuclear accident, led to an increase in energy import costs and increased economic and monetary pressure.

According to EIA data, Japan's single-day liquefied natural gas imports increased by nearly 40% from 2010 to 2014. Increasing energy imports once turned Japan's trade balance negative, leading to increased pressure on the yen to depreciate. Especially at the beginning of the year, among major commodities, the prices of crude oil, coal, copper, and silver rose one after another

On the other hand, the environment in which the yen is located has changed over the past two years

Foreign exchange brought about by huge trade surpluses and return on investment was not enough to offset the impact of the depreciation of the yen after conversion to yen. According to Japan's Mizuho Bank's estimates based on current account balance and reinvestment income, interest, and dividends held in foreign exchange form, capital earned overseas in 2022 did not significantly return to Japan.

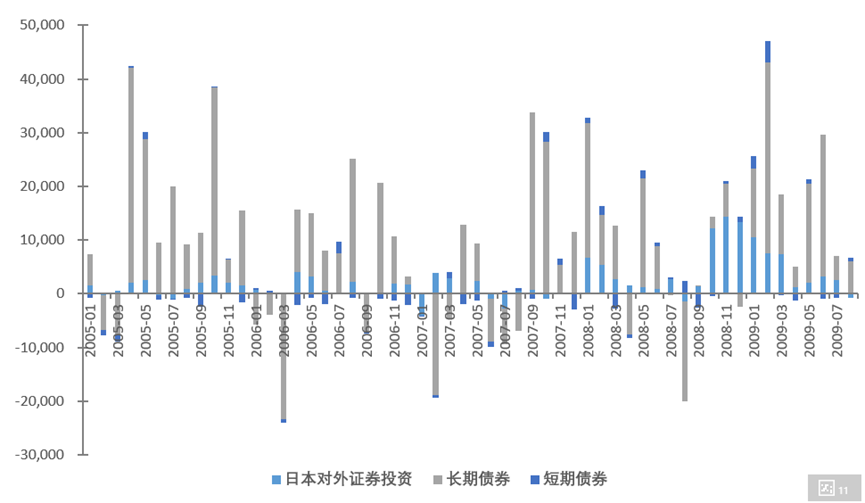

Furthermore, the continued outflow of local capital is also weakening the yen, including Japanese retail investors buying overseas stocks through NISA accounts, and domestic institutions increasing their holdings of overseas bonds

According to data from the Japan Investment Trust Association, since April 2021, Japanese investors have injected nearly 9.9 trillion yen into trust funds investing in foreign stocks, which is more than double the amount they have invested in domestic stock funds.

According to the latest data released by Japan's Ministry of Finance, Japanese investors made a net purchase of 1.8 trillion yen of foreign bonds in February. In terms of foreign stocks and funds, Japanese investors made net purchases of 245.2 billion yen, and the yen continued to weaken due to the trend of capital flows overseas.

In response to the economic slowdown, the Bank of Japan implemented loose monetary policies including negative interest rate policies and yield curve control (YCC). At the same time, the stability of the foreign exchange market is maintained through large-scale purchases of yen. In 2022 and 2023, the Bank of Japan directly interfered with the exchange rate by selling US bonds in the foreign exchange market in an attempt to curb the further depreciation of the yen.

It was the Bank of Japan's immediate substantive exchange rate intervention that caused the yen exchange rate to be contained on the basis that the Bank of Japan's monetary policy had not changed, and the strength of yen depreciation in the short term was weakened.

In November 2023, the yen once again faced the test of “life and death.”

In the second half of 2023, while Japan “walked slowly” to relax the YCC upper limit, the US rapidly increased its issuance of US debt in the third quarter. Interest rates on US bonds once rose above “5,” and the spread between the US and Japan once again suppressed the yen exchange rate.

This time, the Bank of Japan's primary choice was oral intervention while cooperating with a certain scale of yen purchases (the total purchase of yen by the Ministry of Finance of Japan from September to October 2023 reached 20 billion US dollars)

In terms of verbal intervention, the Bank of Japan chose the interest rate method rather than the exchange rate method this time. Ueda's relatively hawkish rhetoric this time has fueled speculation that the Bank of Japan will officially withdraw from negative interest rates, reducing the selling power of yen in the foreign exchange market.

On March 19, the Bank of Japan announced that it would raise the policy interest rate by 10bp to 0%, and only nominally withdrew from the yield curve control policy that had maintained 17 years. Since there was no more information beyond expectations, the yen arbitrage trading was not significantly affected, so the yen continued to fall after a short choice and has once again reached the “life and death mark” of 152

Before, when Japan did not withdraw from negative interest rates, the Bank of Japan could use the voice of “raising interest rates” to weaken the yen bears and then actively interfere in the foreign exchange market. Furthermore, compared to the situation when the Bank of Japan raised interest rates last time in 2006, it did not trigger a large-scale return of overseas capital, and higher overseas earnings are still attractive.

So now that the boots have landed, how will the Bank of Japan deal with the pressure to depreciate the yen?

Now, the point of the market game has come to when the Federal Reserve will cut interest rates this year, and how drastically.

Since 2023, US private sector consumption and investment have been showing resilience due to the wealth effect, and the GDP month-on-month discount rate for the fourth quarter of 2023 was further raised to 3.4%.

Judging from current economic data and inflation data, the possibility of a “soft landing” where US inflation falls back but the economy does not slow down significantly is increasing.

In this context, if liquidity risk continues to be within a manageable range, there is still a possibility that the timing of the Fed's interest rate cut this year will be further delayed, and the general direction of the next trend in the US dollar index may also be delayed. As far as the yen is concerned, there may be continued negative external pressure.

In the context of a strong dollar, it may be difficult for the Bank of Japan to completely reverse the decline in yen by relying only on “verbal intervention+market entry intervention”.

As far as Japan itself is concerned, even if wage inflation currently rises, the burden left over from its fiscal monetization path over the years determines that the Bank of Japan's interest rate hike is very limited. If interest rates are too high, the yen may face a credit crisis.

Seen in this way, the Japanese authorities seem to have no choice but to interfere in the foreign exchange market due to ongoing external pressure, and on the other hand, a weak economy that relies on depreciation of the exchange rate, and on the other.

There may also be a slight turning point

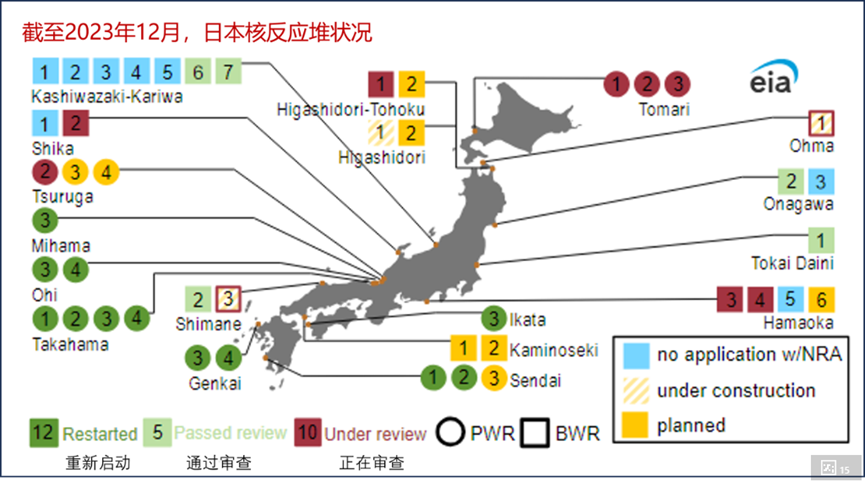

After the Fukushima Daiichi nuclear accident in 2011, Japan largely abandoned nuclear power. By 2013, all of Japan's remaining 48 nuclear reactors had been shut down.

Since 2015, Japan has been promoting the restart of nuclear programs, but progress has been relatively slow.

However, due to recent increases in the volume and price of energy imports, the trade deficit has been accompanied by a depreciation of the yen. As a result, the Japanese authorities have been speeding up the process of restarting nuclear power plants since 2022.

Japan's Minister of Economy, Trade, and Industry Nishimura predicts that operating a nuclear power plant can buy less than 1 million tons of liquefied natural gas (LNG) from overseas in a year, while reducing LNG imports can improve the trade balance and ease the pressure of yen depreciation.

As the restart of nuclear power plants progressed, nuclear power began to replace imports of liquefied natural gas. In 2023, Japan's liquefied natural gas imports fell 8%, and in terms of procurement costs, the 2023 expenditure of 6.5 trillion yen (about 44 billion US dollars) was also 23% lower than in 2022.