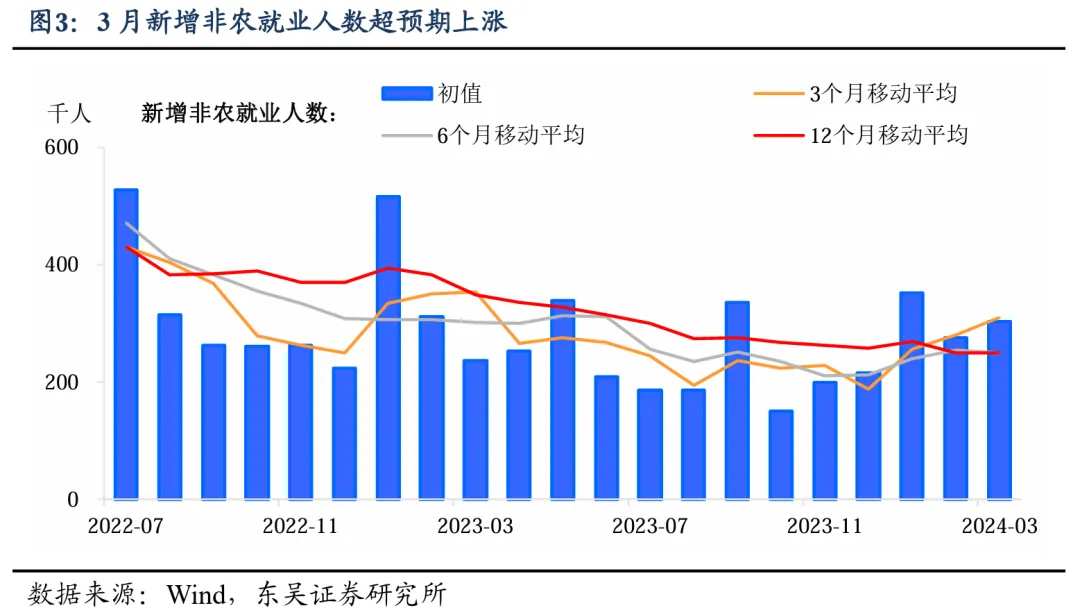

What happened to this market? The “hot” non-agricultural data brought about a sharp rebound in US stocks and gold, which once again set a new historical record. In March, 303,000 new non-farm payrolls were added (vs. 214,000 expected), and the employment data for January and February was revised overall. However, the expected market turmoil did not come, and US stocks rose at the opening. Gold even hit a new high of $2,330 per ounce, highlighting the “unbelief” in non-farm payrolls data. How do you understand this “disbelief”? We think it can be interpreted on three levels:

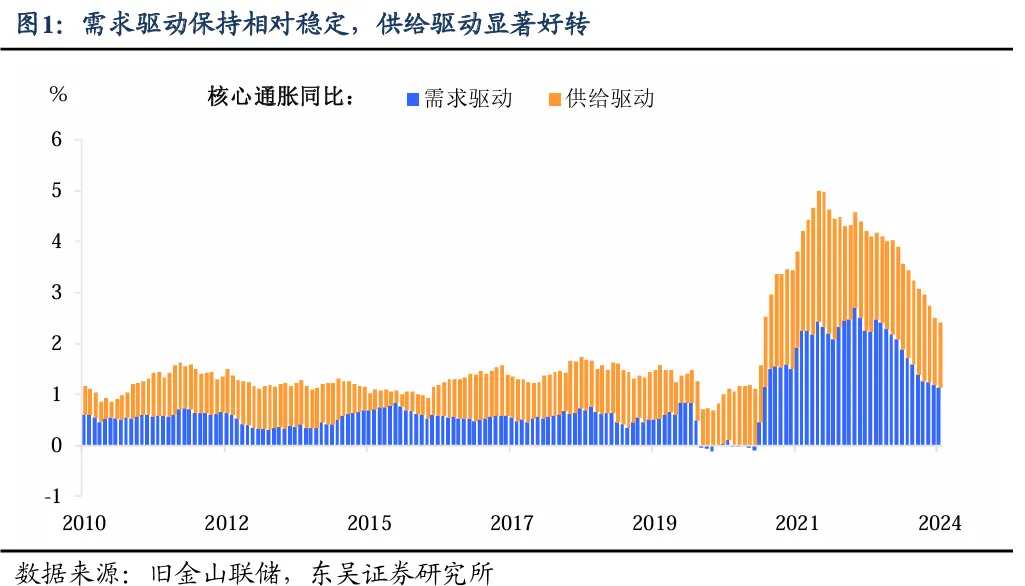

First, in the current job market, supply-side factors are probably even greater. In his recent speech, Federal Reserve Chairman Powell tends to believe that the economy is driven by the supply side. This is reflected in March's non-farm payrolls data: labor supply increased, wage growth declined — the March employment data did not break the framework for Powell's interest rate cuts this year.

Second, the Federal Reserve's current “policy balance” may be more inflation-oriented, while the importance of employment has decreased. This was reflected in a recent speech by the Federal Reserve's voting committee — downplaying the labor market and putting more emphasis on inflation. As a result, strong labor-market performance may not be as important as it was in the past.

Third, the “moisture” of non-agricultural data is rising. On the one hand, not long ago, the Philadelphia Federal Reserve “acknowledged” that the US employment data was distorted, overestimating 800,000 people for the full year of 2023; on the other hand, in the election year, the US White House placed extreme emphasis on employment data — Biden said in a statement issued after the data was released that the March non-farm payrolls report was “a milestone in America's recovery.” The quality of US employment data this year is still worth paying attention to.

Well, what is the specific performance of this data. Looking at the labor market, we think it is worth paying attention to in terms of total volume and structure. Looking at the details:

In terms of total volume, the labor market adds momentum to the supply side of the economy. The number of new non-farm payrolls increased by 303,000 in March, up from the previous 12-month average monthly increase of 231,000. In addition to this, the number of new jobs added in January-February was raised, totaling 22,000 more than before the revision; the labor participation rate also increased further. The number of people employed in the combined household survey increased by 498,000 in March after continuing to decline in the previous three months, which confirms the strong momentum of employment growth.

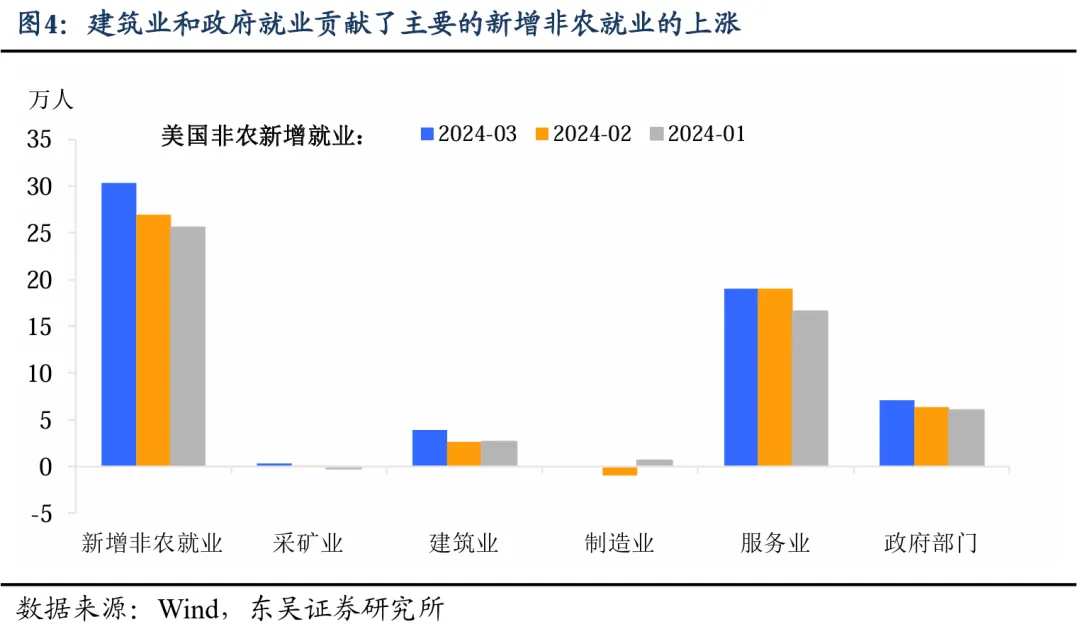

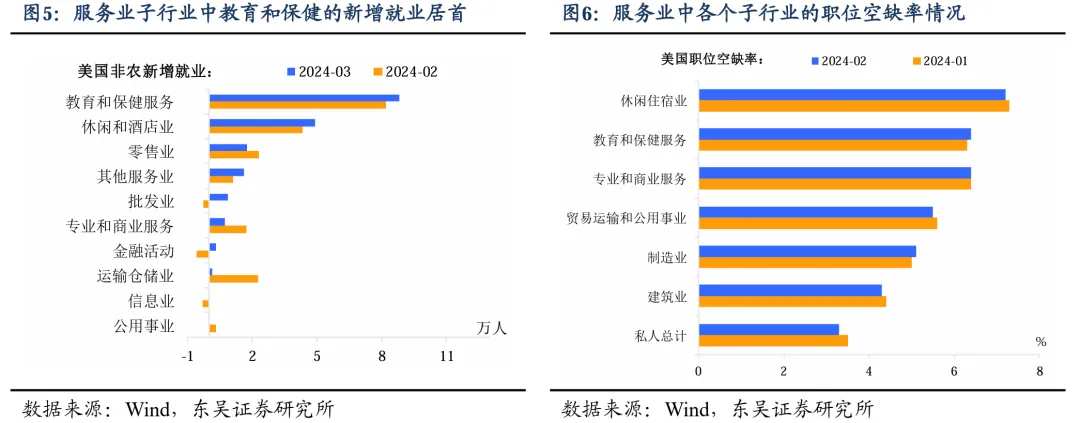

Structurally, the rise in new non-farm payrolls was concentrated in three sectors: health services, government, and construction. Specifically, the healthcare sector increased by 72,000 people in March, and government departments added 71,000 people. Other significant growth areas include construction, which increased by 39,000 in March. In the service sector, the leisure and hospitality industry increased by 49,000, and the growth of new jobs in education and health services, leisure and hospitality was a major factor in the increase in such employment.

Judging from job vacancy data, education and health services are still the industries with the most job vacancies, and labor supply and demand are tight. Of all industries, only manufacturing employment remained unchanged. After falling to 10,000 in February, the number of people employed in manufacturing remained the same in March.

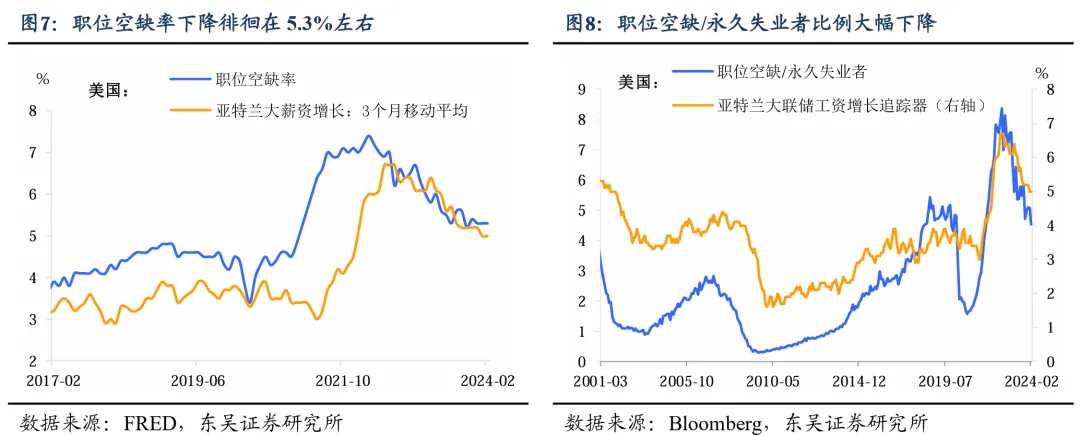

Job vacancies and non-temporary layoffs need to be further cooled down. The imbalance between supply and demand is the main reason for the tight labor market. Overall, the job vacancy rate remained hovering at 5.3% in March, which shows that it is not difficult to find a new job even if you get laid off, so this is enough to prevent the unemployment rate from continuing to rise in a self-reinforcing manner. And the ratio of job vacances/non-temporary layoffs is a good explanation for wage inflation. Although this ratio has declined sharply from a higher point, it needs to continue to slow down to further cool wage inflation.

The year-on-year wage growth rate declined. Wage levels are closely watched by the Federal Reserve and viewed as a sign of whether they would increase inflationary pressure. Specifically, the average salary rose 4.1% year on year in March, slowing by 0.2 pct compared to February, the slowest growth rate since mid-2021; average salary rose 0.1 pct to 0.3% month-on-month, all in line with expectations. Among them, the hourly wage growth rate for leisure hotels, education and medical care, and other services all declined from the previous month.

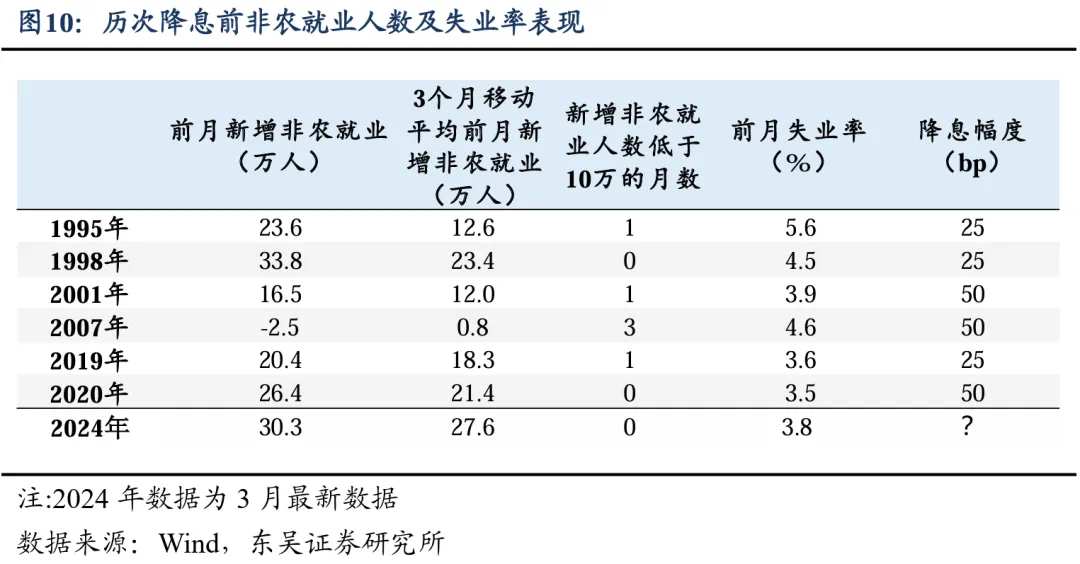

The impact of the stabilization of the agricultural sector in March was only the Federal Reserve's patience, not determination. If you look at it from a historical perspective, in the first 3 months of interest rate cuts, in most cases, the number of new non-farm payrolls was less than 100,000. For example, in 1995, although the non-farm payrolls data performed well, the unemployment rate was 5.6% at the average level for half a year; for example, in 2001, all economic indicators in the US deteriorated before interest rate cuts, and the moving average of non-farm payrolls fell to 120,000 people in the three months before the interest rate cut. What is more extreme is that in 2007, before interest rate cuts, the number of non-farm payrolls was continuously lowered after revisions, and non-farm payrolls fell to a negative value in August.

Currently, we believe that non-agricultural data is an important factor in the Fed's decision to cut interest rates, but it is not decisive. Due to the “supply story” behind the current job market, the impact of non-farmers in March may have made the Federal Reserve more “patient”, and at the same time, inevitably, its internal differences will also grow larger — Powell's supply narrative vs. Waller's demand narrative, so we need to pay more attention to the performance of US inflation after the employment data was released.

edit/new