Source: Wall Street News

Bank of America also supports Powell's view that it reserves the possibility of cutting interest rates in June rather than predicting data in advance, thus avoiding the risk of unnecessary financial market tightening.

Divisions within the Federal Reserve over policy direction are intensifying, particularly between two key players, Powell and Waller.

Last week, Federal Reserve Chairman Powell and Governor Waller each delivered major speeches on interest rate prospects. The former continues to show a dovish attitude, saying that if economic activity continues to weaken, the Federal Reserve will cut interest rates. The latter, on the other hand, showed a stronger hawkish attitude, saying that recent inflation data was “disappointing” and that there was no need to cut interest rates during the year.

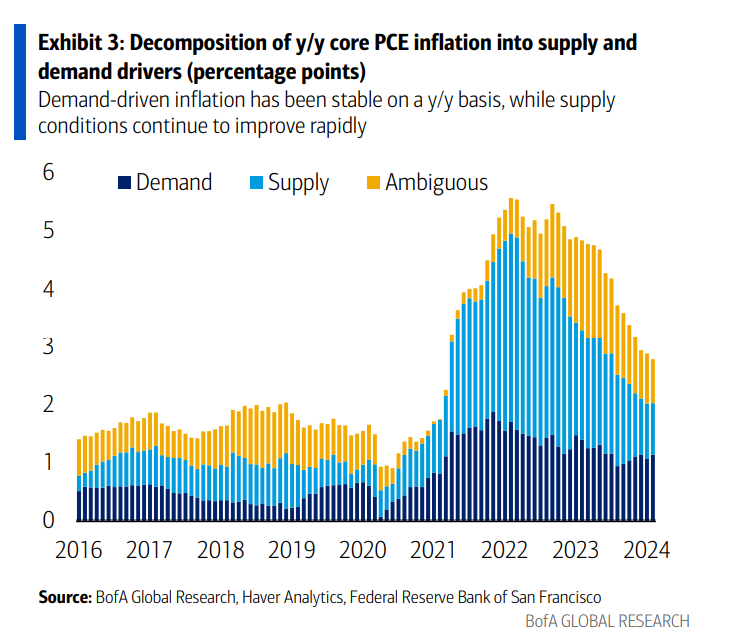

In response, Bank of America's Aditya Bhave analyst team released a research report on Tuesday local time, pointing out that due to the year-on-year base effect of core PCE inflation, it was favorable until May, but 6 of the 7 months at the end of the year were unfavorable. If the Federal Reserve does not provide sufficient reasons to cut interest rates in June, it may have to wait until March 2025 to start cutting interest rates.

In addition, the inflation rate remains relatively low, and the Bank of America supports Powell's view that it reserves the possibility of cutting interest rates in June rather than predicting data in advance, thus avoiding the risk of unnecessary financial market contraction.

Powell continues to show a dovish stance

Bank of America believes that Powell's remarks last Friday were generally balanced, but the overall position is still dovish. The key issue now is to determine the timing of interest rate cuts rather than the possibility of raising interest rates.

Powell's policy response shows clear asymmetry: if economic activity weakens, the Federal Reserve will consider cutting interest rates, but while economic activity remains strong and inflation does not rise, the Fed will not shift to a more hawkish position.

By implication, we think Powell's basic assumption is that strong future economic growth will be driven entirely by supply rather than demand. The data needed to prove that demand was growing at an accelerated pace. This is in line with Powell's emphasis on labor supply expansion.

Notably, although Powell said that the Federal Reserve is in no hurry to cut interest rates, he said that core PCE inflation in February “basically met our expectations,” implying that he is optimistic about the progress of reducing inflation.

In other words, the downward trend in inflation has not been disrupted.

Finally, Powell also discussed the differences in the FOMC during Friday's event. Powell said that the differences “are not a problem” and that “life continues.”

In response, Bank of America wrote:

These comments are interesting because we are beginning to see a growing rift within the Commission. We believe this is a natural phenomenon, as policy differences tend to widen as decision points approach.

Waller is full of eagles

Waller showed a stronger hawkish attitude in his speech last Wednesday, saying there is no need to cut interest rates during the year. He believes that the risk of delaying interest rate cuts is far lower than cutting interest rates too early. Unlike Powell and Governor Cook, Waller believes that current policy risks are unbalanced.

Bank of America pointed out that Waller also paid less attention to supply-side factors, and did not even mention the promotion of labor supply by immigration and increased labor participation, but this has always been the focus of Powell's discussions.

Waller is more concerned about strong consumption than Powell, probably because he believes inflation is demand-driven rather than supply-driven.

After Waller's speech, industry insiders analyzed it from different perspectives. Some people have explained that Waller believes that the current financial environment is still very tight.

Waller pointed out that he will closely monitor the easing of the Financial Condition Index because it is mainly due to the stock market — Mag 7 in particular. He also pointed out that the tightening of credit spreads may only be due to an increase in private credit borrowing.

He believes that the current financial environment is very tight because real interest rates are still very high. (Powell's previous speech at the press conference was interpreted by the market as a possible further relaxation of the financial environment)

Three reasons for the deepening differences within the Federal Reserve

Bank of America believes there are three main reasons for the differences between Powell and Waller:

First, there are differences of opinion about whether the strong impetus for the economy is supply-side (with deflationary effects) or demand-side (which may lead to inflation). In his speech last week, Powell focused on the supply side, while Waller focused on the demand side.

It is worth mentioning that supply-side issues took center stage at the March Federal Reserve (FOMC) meeting, as can be seen from the economic forecast summary:

Growth expectations for the next three years have been raised sharply, but inflation and policy interest rates have risen only moderately, and there has been little change in the unemployment rate.

Second, there are differences on how to balance the Federal Reserve's dual objective (that is, return to the 2% inflation target while ensuring a soft landing).

Some policymakers may be willing to accept a longer path back to 2% inflation to ensure a soft landing. Others may give higher priority to returning inflation to target, even if that means a greater slowdown in activity.

Third, some policymakers are more concerned about the “risk of a jump” in the policy path that may occur.

Bank of America pointed out that due to the year-on-year base effect of core PCE inflation, it was favorable until May, but 6 of the 7 months at the end of the year were unfavorable. If the Federal Reserve does not provide sufficient reasons to cut interest rates in June, it may have to wait until March 2025 to start cutting interest rates.

In the three months starting in May, the base effect averaged more than 0.3% per month, while from June to December, the average base effect was less than 0.2% per month.

For overall PCE inflation, the average monthly base effect for the three months ending in May was 0.18%. This figure is expected to be 0.17% per month in the second half of 2024.

As far as the Federal Reserve is concerned, the current annual growth rate of overall PCE inflation is relatively low at 2.5%, while the core inflation rate is 2.8%. This is a positive sign as inflation remains relatively low.

Will the Federal Reserve start cutting interest rates in June?

Does this risk of a jump mean the Fed should start cutting interest rates in June?

One view is that the Federal Reserve should “hit the iron while it's hot” to start easing interest rates. Even if interest rates are cut three times this year, interest rates will still be viewed as restrictive by most estimates.

Not cutting interest rates this year may risk major financial tightening. The 10-year yield may return to 5%, and there are heightened concerns about regional banks, commercial real estate, and high-yield credit.

Another view is that when the financial market lowered expectations of interest rate cuts earlier, the financial environment actually did not tighten.

Currently, Bank of America believes that Powell favors the first camp rather than the second camp.

Our view is that he is capable of persuading most Federal Reserve members to support his views. Looking back at his comments about differences within the Commission, he seemed comfortable with policy decisions that were not unanimous. Given Powell's moderate stance, this increases the possibility that interest rates may be cut in June.

What does this mean for policy predictions? Bank of America stated:

On a year-over-year basis, demand-driven inflation remained relatively stable, while supply-side drivers improved markedly. This is consistent with Powell's view.

However, if you look at the 6-month base period, demand-driven inflation has accelerated in recent months, this is more in line with Waller's concerns, although the calculation of the 6-month growth rate may be affected by seasonal factors.

Based on comprehensive considerations, the Bank of America maintains the forecast that it will cut interest rates three times this year, and is expected to cut interest rates starting in June. However, if there is an increase of 30 basis points or more in the next two core PCE data, especially if economic activity remains strong, then the possibility of interest rate cuts in June may decrease.

editor/tolk