① Rongchang Biotech plans to increase 2.55 billion yuan for new drug research and development projects to ease the tight R&D and operating capital situation; ② Sales expenses in 2023 will be 775 million yuan, up 75.90% year on year, and R&D expenses during the same period were 1,306 billion yuan, up 33.01% year on year; ③ To get out of the situation of being surrounded by strong enemies as soon as possible, Rongchang Biotech needs to make additional efforts to develop new drugs.

“Science and Technology Innovation Board Daily”, April 3 (Reporter Zheng Bingxun) Rongchang Biotech (688331.SH, 9995.HK) has always relied on two marketed products, taitacip (RC18) and verdicitumab (RC48). Faced with questions from the outside world about lack of cash flow, Rongchang Biotech once issued a special announcement at the beginning of the year refuting that the rumor did not match the facts.

However, just over two months later, Rongchang Biotech itself completed self-proof of its tight cash flow situation with a “fixed increase plan.”

Rongchang Biotech recently announced that it will issue up to 707.632 million A-shares to no more than 35 specific investors. The total capital to be raised will not exceed 2.55 billion yuan, all of which will be used for “new drug research and development projects”. The innovative drugs involved include RC18, RC48, RC28, RC88, RC148 and RC198.

In response to this increase, Rongchang Biotech said, “It will help speed up clinical and pre-clinical research on the company's R&D pipeline project and promote the listing process of related products at home and abroad, and ease the tight situation of the company's R&D and operating capital.”

▌Too shy, making money is far less fast than spending money

In fact, there are signs that Rongchang Biotech's funding situation is already tight, but it is even more urgent after entering 2024.

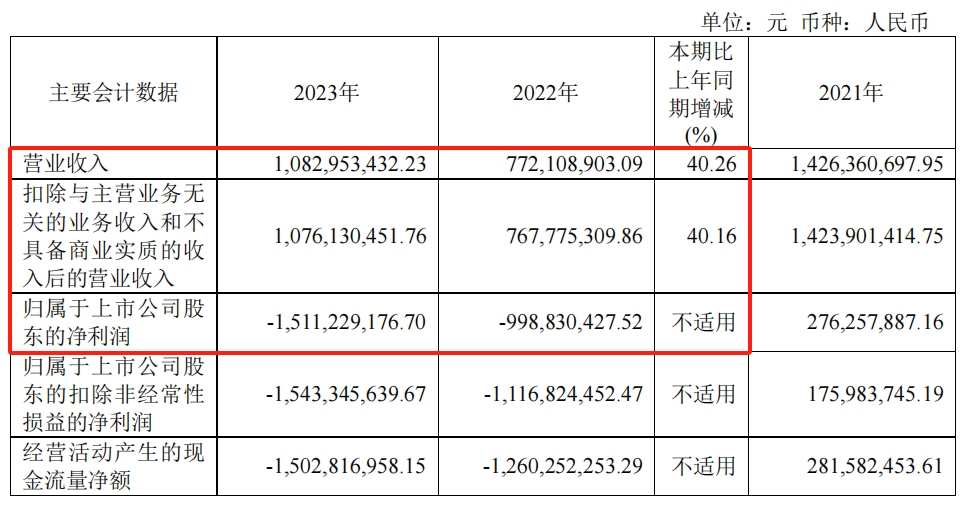

According to the 2023 financial report, Rongchang Biotech achieved annual revenue of 1,083 million yuan, an increase of 40.26% over the previous year, and a net loss of 1,511 million yuan to mother, an increase of 512 million yuan in losses over 2022. In response to this situation, Rongchang Biotech pointed out that the main reason is that the continuous promotion of various R&D pipelines has drastically increased R&D expenses, and commercialization activities have increased expenses.

Specifically, Rongchang Biotech's sales expenses in 2023 were 775 million yuan, up 75.90% year on year, and R&D expenses during the same period were 1,306 billion yuan, up 33.01% year on year. The sum of these two expenses alone far exceeds the overall revenue, which has also led to the rapid consumption of cash on Rongchang Biotech's account.

By the end of 2023, Rongchang Biotech had a cash and cash equivalent balance of only $727 million. Compared with $2,069 billion at the beginning of the year, even without considering other supplements, it consumed at least $1,342 billion in one year. If R&D investment in 2023 is used as a reference, Rongchang Biotech will face the difficult situation of “cooking without rice” in 2024.

Furthermore, Rongchang Biotech still has 284 million yuan in short-term loans and 841 million yuan in long-term loans. Together, the two account for 20.35% of total assets in 2023.

From this, it is not difficult to understand why Rongchang Biotech urgently needs a fixed increase to ease the tight funding situation.

Currently, Rongchang Biotech's “livelihood” depends entirely on the two approved products, taitacip (RC18) and verdicitumab (RC48). Taking 2023 as an example, Rongchang Biotech received about 1.05 billion yuan in revenue from biopharmaceuticals, accounting for 97.50% of the main revenue.

As an investor, the “Science and Technology Innovation Board Daily” reporter learned from Rongchang Biotech Company personnel that in 2023, Taitaxip contributed about 520 million yuan in sales revenue, and revenue from viducitumab was about 530 million yuan. In 2022, revenue from these two products was 330 million yuan and 405 million yuan, respectively.

Verdicitumab once brought unlimited “glory” to Rongchang Biotech — it is not only China's first original antibody conjugate drug (ADC), targeting HER2, but it is also the first ADC drug in China to receive dual certification as a breakthrough therapy by the US FDA and the China Drug Administration. Once upon a time in 2021, Rongchang Biotech reached a cooperation with Seagen using verdicitumab, and is expected to receive up to 2.6 billion US dollars in potential payments and win the title of “domestic ADC leader”.

However, based on the above sales, the sales growth rate of tetracip and verdicitumab in 2023 is about 57.58% and 30.86%. Following this development, it is likely that verdicitumab will be overtaken by tetracip in 2024.

“The growth rate of the product depends on competition in the market. For one indication, the market space for later products is not that large compared to competing products,” Rongchang Biotech said in response to the growth rate of verdicitumab. The other party also revealed that tetracip switched from conditional approval to full approval in China at the end of 2023. Coupled with the volume of products brought about after price cuts during previous health insurance negotiations, it boosted sales growth.

According to financial reports, the production volume of Taytacip in 2023 was 859,400 units, and sales volume was 782,300 units. Sales increased 59.37% year over year, and the production and sales rate was 91.02%. In the same period, the production volume of verdicitumab was 265,600 units, and the sales volume was 173,700 units. Sales increased 15.24% year over year, and the production and sales rate was 65.40%.

However, an anonymous investor told the “Science and Technology Innovation Board Daily” reporter, “Judging from the current sales volume of Rongchang biological products, the degree of commercialization is actually not very good, and the company has many research lines, especially multiple phase III clinical trials at the same time, which consumes a lot of cash flow. Only by running commercialization can we achieve autologous hematopoiesis.”

Currently, Rongchang has 8 molecules and more than 20 candidate biopharmaceutical products are being developed. Among them, RC18 has submitted a new drug marketing application to the CDE in August 2023 for rheumatoid arthritis. It is the fastest progress in research. More than 10 of the remaining pipelines are in clinical phase III, and more pipelines are in clinical phase I and phase II.

▌Strong enemies surround us and need to break through urgently

Rongchang Biotech's pressure, in addition to the fact that the products already on the market cannot cover expenses, is that there are already many products on the market that target the same indications and are being intensively promoted clinically.

According to data, the indications for titacipr to treat systemic lupus erythematosus (SLE) were conditionally approved for marketing by the National Drug Administration (NMPA) in March 2021, were included in medical insurance in December of the same year, and were simply renewed at the end of 2023, moving from conditional approval to full approval.

Following the approval of tetracip, in June and December 2021, indications for verdicitumab for the treatment of gastric cancer (GC) and urothelial cancer (UC) were also conditionally approved for marketing in China. Among them, GC indications and UC indications were included in medical insurance in January 2022 and January 2023, respectively, and both were simply renewed at the end of 2023.

Following the successful renewal of the contract in the national negotiations, verdicitumab is not only one of the 7 ADC drugs approved for marketing in China, but also one of the 3 ADC drugs covered by medical insurance. The other two are imported products, emmetastuzumab and vibutuximab.

In fact, judging from treatment demand, both Rongchang Biotech products have good market potential.

According to Frost & Sullivan, the number of patients with systemic lupus erythematosus worldwide in 2020 was 7.795,500, and is expected to reach 8.185,600 in 2025. The corresponding therapeutic drug market will grow from 1.6 billion US dollars to 6.5 billion US dollars. In China, the systemic lupus erythematosus drug market was US$400 million in 2021 and is expected to reach US$3.4 billion in 2030.

The number of UC indications targeted by verdicitumab was 516,000 in 2020, and is expected to increase to 586,000 in 2025. Of these, the number of new cases in China will also increase from 77,000 to 91,000. As the fifth largest malignant tumor in the world, GC is expected to have 1.41 million new cases in the world and 610,000 cases in China by 2030. At that time, the global drug market will reach 36.4 billion US dollars.

However, the broad market naturally attracted more participants to join. Rongchang Biotech's titacip and verdicitumab approved indications all faced an increasingly fierce competitive pattern.

In addition to facing competition from belliumab, which was marketed before it, Taytacip also has to deal with multiple dormant potential rivals. According to incomplete statistics, by the end of 2023, nearly 10 listed companies, including Nuochengjianhua (688428.SH, 9969.HK), Zhixiang Jintai (688443.SH), Hengrui Pharmaceutical (600276.SH), and Kangyuan Pharmaceutical (), had carried out drug research and development on lupus erythematosus. 600557.SH

Among them, Nuochengjianhua's BTK inhibitor obutinib and Zhixiang Jintai's IFNAR1 monoclonal antibody GR1603 are progressing rapidly and have now entered phase II clinical trials. Other companies, including Hengrui Pharmaceutical's SHR-2001 and Kangyuan Pharmaceutical's KYS202002A injections, are mostly in phase I clinical trials.

In contrast, the indication that verdicitumab was approved is that in the domestic market, more than 1 product was marketed earlier than it, and even after it was approved, several products were approved for further market sharing.

Among them, Roche's trastuzumab and BMS's navulizumab (drug O) were approved for marketing in January 2016 and March 2020, respectively, and followed by vidicitumab, imClone (Eli Lilly) remocimab, Cindilizumab from Cinda, tirelizumab from BeiGene, and Merck's pabolizumab (K drug).

For UC, Tirelizumab from BeiGene and treprilizumab from Junshi Biotech were approved by the NMPA in April 2020 and April 2021, respectively.

Of course, in addition to facing many “strong opponents” that have already been marketed, verdicitumab also faces many potential competitors.

According to statistics from China Galaxy Securities, using only the ADC track where the popular target HER2 is located, it can be found that at least a variety of ADC drugs, including Lepu Biotech's MRG002, Hengrui Pharmaceutical's A1811, Zhejiang Pharmaceutical's ARX788, and Columbotai's A166, are undergoing clinical research on GC. Furthermore, MRG002 and A166 are also simultaneously carrying out clinical research on UC.

It can be seen from this that if Rongchang Biotech wants to get rid of the dilemma of being surrounded by strong enemies as soon as possible, it may have to work harder to develop new drugs at a faster pace.