The three major US stock indexes all fell more than 1% in the intraday period. The Dow closed down nearly 400 points to a two-week low, and both S&P recorded their biggest daily decline in four weeks. Tesla recorded the biggest decline in four weeks, closing down nearly 5%; the chip stock index fell 1.5% and stopped three times; Nvidia closed down 1% after falling 3% in the intraday period, and Intel fell more than 4% after the market; the China General Stock Index rose four times in a row, outperforming the market on two days. Ideal Auto rose more than 1%, Xiaomi's US stock fell more than 3%, and NIO and Xiaopeng Motors fell more than 2%.

The 10-year US Treasury yield hit a four-month high and the biggest two-day increase in two months. The two-year yield hit a new high of nearly two weeks before falling. The US dollar index fell during the intraday period after hitting a new high for more than four months, and hit a new low after the announcement of US job vacancies. The offshore renminbi rose more than 100 points in the intraday period and rose above 7.26.

Bitcoin once fell below $65,000 in the intraday period. Crude oil closed up nearly 2%, hitting a five-month high over the past few days. Gold hit a record closing record for four days, and silver rose more than 3%. Lunan aluminum rose nearly 2% to a new high during the year, and Lunton copper rose to a two-week high in a row.

Following the unexpected recovery of the US ISM manufacturing index to an expansion range for February announced on Monday, the US job vacancies and factory orders announced on Tuesday were also better than expected: the number of JOLTS job vacancies in February was slightly higher than the number of vacancies in January after the downgrade, stabilizing at a record high, reflecting the resilience of the labor market; factory orders in February exceeded expectations by 1.4% after two consecutive months of decline.

Stable economic data has caused investors to further lower their expectations for the Fed to cut interest rates this year. The media pointed out on Tuesday that the total interest rate cut expected by the market this year has fallen back to around 65 basis points, which is lower than the 75 basis point rate cut expected by Federal Reserve officials this year announced after the Federal Reserve meeting in March. The good news of the economy became bad news for the US financial market. US stocks, US Treasury bond prices, and the US dollar index fell sharply.

US stocks are being dragged down by technology stocks and healthcare stocks. Tesla's delivery volume in the first quarter not only fell year on year for the first time since the beginning of the COVID-19 pandemic, but the 8.5% drop far exceeded analysts' expectations, which had recently been lowered. The stock price once fell nearly 7%, the worst performance among blue chip technology stocks, the biggest one-day decline since Tesla's wholesale sales in China fell 19% year on year in February nearly a month ago. To the surprise of the industry, US regulators did not raise the 2025 federal health insurance Medicare rate, making matters worse for insurance companies facing faster growth in medical costs than expected. The healthcare giant UnitedHealth once fell nearly 8% in the intraday market, leading the decline in Dow's constituent stocks.

The price of various US Treasury bonds fell further on Tuesday, and yields climbed. The yield on 5-year to 30-year US bonds all hit new highs this year. The commentator said that the market expects the Federal Reserve to start cutting interest rates to be delayed, and commodities have recently risen, and crude oil has been at a high level for several months, increasing upward pressure on inflation. Bond-market traders no longer expect three interest rate cuts this year. This reassessment of expectations is driving up US bond yields. The yield on the benchmark 10-year US Treasury rose above 4.40% intraday for the first time in four months. This week's two days combined, it rose more than 10 basis points, the biggest two-day increase since the beginning of February.

In the US stock market, US bond yields generally declined, and two-year US bond yields smoothed out the increase and turned down. Cleveland Federal Reserve Chairman Meister, who has the right to vote at the FOMC meeting of the Federal Reserve's Monetary Policy Committee this year, warned that there is a risk of cutting interest rates too early. It is still expected that the Fed will cut interest rates this year. He believes that cutting interest rates three times is still reasonable, but it is impossible to act in May. The bond market reacted relatively calmly to Meester's speech.

In the foreign exchange market, the US dollar index turned down in the middle of the session after hitting a new high of more than four months in a few days. The decline accelerated after US job vacancies were announced, and non-US currencies generally rebounded. Japan's Finance Minister Shunichi Suzuki reiterated that intervention in the foreign exchange market is not ruled out due to excessive fluctuations in foreign exchange. The yen was still at one point close to the low since 1990, which was set by a drop of 152.00 last week. Later, as the US dollar depreciated, the yen rose slightly. Tatsuo Yamazaki, a former Japanese Ministry of Finance official, believes that the Japanese government may intervene at any time if the yen falls below the current range, given that the Japanese official's remarks have raised the alert level.

Cryptocurrency was not boosted by the dollar's fall, and Bitcoin dived more than $5,000 and fell below $65,000 in the intraday period. Some commentators believe that the drop in currency prices may be related to the sell-off by the US government. According to the media, a wallet belonging to the US government sold 301.75 million bitcoins on Tuesday. These are stolen bitcoins related to the dark web, black market, and the Silk Road that the government confiscated in 2022.

Among commodities, China's manufacturing PMI was strong, driving London's basic metals to a good start in the second quarter. Various metals, led by aluminum, rose by at least 1%. The tense situation in the Middle East, which stimulates safe-haven demand, and the fall in the US dollar have boosted the further rise of gold, continuing its trend of reaching record highs. New York futures rose nearly 2% in the intraday period. Some analysts believe that the recent rise in gold prices may also be related to the recovery of short positions in family offices and self-operated trading rooms.

Geographic tension has led to an increase in supply threats in the oil market, and international crude oil also continued to rise, hitting a new high in five months. According to CCTV reports, in the early hours of Tuesday morning local time, a Ukrainian drone attacked an oil refinery in the Russian Republic of Tatarstan. According to some media, it was one of Russia's largest oil refineries that was attacked. Also, according to CCTV, Ukrainian President Zelansky said that night that 13 people were injured when Udnepropetrovsk region was attacked by Russian missiles. Also on Tuesday, CCTV mentioned that Iran's Supreme Leader Ayatollah Ali Khamenei issued a statement condemning the attack on the Iraqi embassy in Syria, stressing that the Israeli government will be punished and Iran will make Israel regret the crimes it has committed.

The three major US stock indexes all fell more than 1% in the intraday period, the Dow, S&P, and Tesla all recorded the biggest daily decline in four weeks, and the Chinese stock index outperformed the market on two days

The three major US stock indexes collectively opened lower and maintained an intraday decline. The Nasdaq Composite Index fell more than 1% at the beginning of the session. It fell nearly 1.6% in early trading, and the decline narrowed to less than 1% at the end of the session. The decline in the Dow Jones Industrial Average and the S&P 500 index also extended to more than 1% in early trading. The Dow fell more than 510 points and fell nearly 1.3% in intraday trading, while the S&P index fell more than 1.1% in early trading.

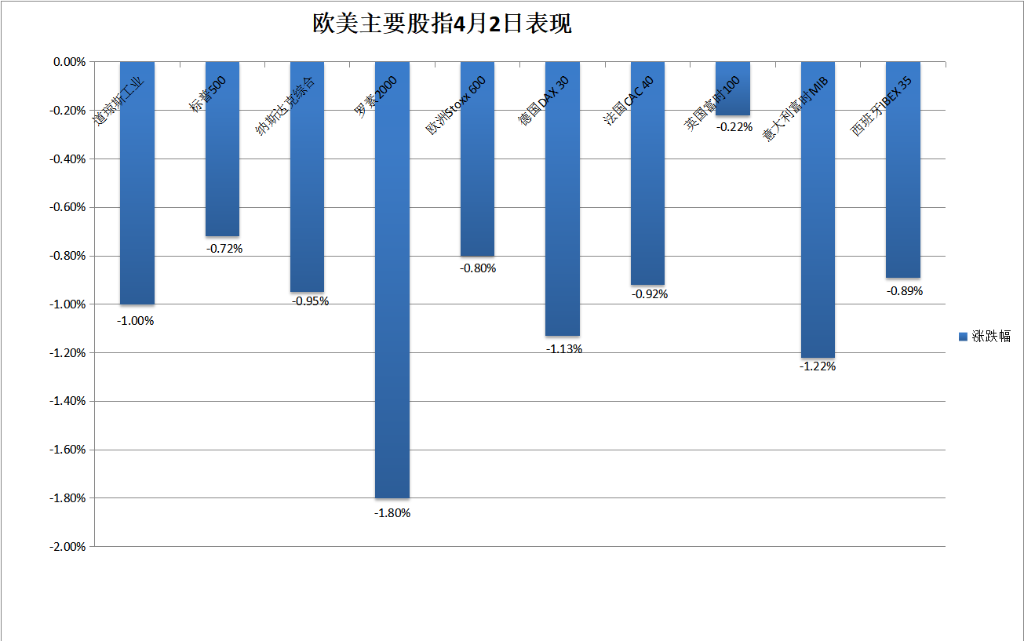

The three major indices collectively closed down, with the S&P and Dow falling for two consecutive days, both recording their biggest closing losses in four weeks since March 5. The Dow closed down 396.61 points, or 1%, to 39170.24 points, breaking its closing low since March 19. S&P closed down 0.72% to 5205.81 points. The NASDAQ index, which rebounded slightly on Monday, closed down 0.95% to 16240.45 points, the biggest drop since March 8, and fell back to its closing low since March 19.

The small-cap stock index Russell 2000, which is mainly value stocks, closed down 1.8%, outperforming the market for two consecutive days and falling to a low level since March 19. The Nasdaq 100 Index, which focuses on technology stocks, closed down 0.94%, and the Nasdaq Technology Market Capitalization Weighted Index (NDXTMC), which measures the performance of technology constituents in the Nasdaq 100 Index, closed down 0.79%, all falling back to their lowest level since March 19 after rebounding on Monday.

Including Microsoft, Apple, Nvidia, Google's parent company Alphabet, Amazon, Facebook's parent company Meta, and Tesla, the tech giant “Seven Sisters” fell at least 1% in early trading, and the decline narrowed or even turned up individually in midday trading. After announcing that the delivery of 386.81 million vehicles in the first quarter fell far short of expectations and was nearly 14% lower than analysts' median expectations, Tesla fell nearly 6.7% in early trading and narrowed in midday trading, closing down 4.9%, the biggest daily decline since March 4. It fell three consecutive trading days to a low level since March 15.

Among the six major FAANMG technology stocks, Microsoft, which had fallen more than 1% in early trading, closed down 0.7%, and began to approach the closing low since March 18, which had fallen for five consecutive days last Thursday; Apple, which had fallen 1% at the beginning of the session, closed down 0.7% and fell to a low level since March 7; Alphabet, which had a record high for four consecutive days on Monday, fell nearly 2% at the beginning of trading, closing down 0.4%; at the beginning of the session, Amazon closed down 0.2%, temporarily falling more than 1% since November 2021, which was refreshed for three consecutive days; The margin closed down and did not continue to break away from what was refreshed last Thursday It closed at a low level since March 11; Meta, which had fallen more than 1% at the beginning of the session and turned up in midday trading, closed up 1.2%, rising for two consecutive days until March 25.

Chip stocks generally declined and outperformed the market. The Philadelphia Semiconductor Index and semiconductor industry ETF SOXX fell more than 2% in the midday session, both falling about 1.5%, falling to closing high levels since March 12, which were refreshed for three days. Among chip stocks, Nvidia's early trading decline, which was roughly flat on Monday, was slightly over 3%, closing down 1%, falling back to its closing low since March 19; at the close, AMD fell 2.5%, Arm fell more than 2%, Intel and Micron Technology fell more than 1%, and TSMC US stocks fell 0.9%. After the market, Intel revealed that the operating loss of the foundry business increased last year from 5.2 billion US dollars in 2022 to 7 billion US dollars. Intel's post-market decline widened rapidly, falling more than 4% after the market.

Most AI concept stocks continued to fall. At the close, BigBear.ai (BBAI) fell more than 5%, SoundHound.ai (SOUN) fell more than 3%, ultra-microcomputer (SMCI), C3.ai (AI) fell more than 2%, Oracle (ORCL) fell 0.9%, Palantir (PLTR) fell 0.6%, and Adobe (ADBE) fell nearly 0.6%, and Astera Labs (ALAB), known as “Little Nvidia,” which sells data center interconnect chips, turned up early trading and closed 1.5%.

Popular Chinese securities either rose or narrowed their intraday decline. The Nasdaq Golden Dragon China Index (HXC) fell nearly 0.6% at the beginning of the session and turned slightly higher in early trading, closing up 0.3%, rising for four consecutive days until March 20. KWEB, an ETF of China, closed up nearly 0.4%, while CQQQ closed down 0.2%. Among the three new car builders, NIO Auto, which fell 4% at the beginning of the market, and Xiaopeng Motor, which fell nearly 6% at the beginning of the market, all closed down more than 2%. Ideal Auto turned down in the short term at the beginning of the market, and closed up more than 1%. Among other individual stocks, by the close, Xiaomi fans fell more than 3%, NetEase fell nearly 2%, Pinduoduo fell nearly 0.8%, Alibaba fell nearly 0.7%, while Ctrip rose more than 4%, Station B rose more than 3%, JD rose nearly 0.2%, and Baidu and Tencent fans rose less than 0.1%.

To the surprise of the industry, US regulators left the federal Medicare rate proposed in 2025 unchanged and not raised, causing insurance companies facing a new obstacle. Healthcare stocks plummeted across the board, UnitedHealth (UNH) closed down 6.4%, leading the Dow, CVS Health Corp (CVS) closed down 7.2%, Centene Corp (CNC) closed down 6.8%, and Elevance Health (ELV) closed down 3.3%.

The bank stock index fell for two days in a row. The overall banking index KBW Bank Index (BKX) closed down 0.9%, continuing to fall from the high level since March 3, 2023; the regional banking index KBW Nasdaq Regional Banking Index (KRX), which rose for two consecutive days on Thursday to a high level since January 30, closed down 1.9%. Last Thursday, the regional bank stock ETF SPDR S&P Regional Bank ETF (KRE) closed down nearly 1.9%.

Bitcoin's sharp decline dragged cryptocurrency and blockchain concept stocks down sharply. At the close, Bitcoin mining companies CleanSpark (CLSK), Marathon Digital (MARA), and Riot Platforms (RIOT) fell nearly 9.4%, 8.8%, and 7.5%, respectively, while MicroStrategy (MSTR), the listed company that holds the most Bitcoin, fell 3.5%, and Coinbase (COIN), the largest US cryptocurrency exchange, fell 2.5%.

Among other highly volatile individual stocks, Trump Media & Technology Group (DJT), a media company owned by Trump, which fell two days in a row, rebounded on the fifth trading day of listing and closed up about 6%, but this is far from over the 21.5% decline after announcing last year's net loss of 58 million US dollars on Monday.

European stocks fell sharply on the first trading day of this week, and the second quarter had a “bad start.” The pan-European stock index, which had been rising for four days, retreated. The European Stoxx 600 Index, which broke the closing record for three consecutive days last Thursday, hit a new low since March 20. Stock indexes of major European countries fell sharply. German stock indexes fell by more than 1%, falling to the highest closing record set for eight consecutive trading days. French stocks and British stocks declined for three consecutive days, falling below closing record highs and one-year highs respectively. Italian and Spanish stock indexes fell for two consecutive trading days after closing at record highs for seven consecutive days.

In various sectors, interest rate-sensitive real estate fell nearly 2.3%, tourism fell by more than 2.2%, retail sales fell nearly 2.2%, medical sales fell by nearly 1.7%. Among the constituent stocks, Novo Nordisk, the highest market capitalization pharmaceutical company listed in Denmark, fell 1.6%; while oil and gas sales, driven by the rise in crude oil, rose nearly 2.5%, hitting a new high of more than five months, thanks in part to Bernstein's first coverage, the Norwegian oil and gas giant Equinor, which was first covered by Bernstein; due to higher metals, the basic resources of the mining sector rose by nearly 1.4%.

The 10-year US Treasury yield hit a four-month high, and the two-year yield hit a new high in nearly two weeks, then declined

Most US bond yields rose for three consecutive trading days. The yield on the US 10-year benchmark treasury bond reached a new low of 4.30% in early Asian trading. At the beginning of the Asian market, the US stock market rose above 4.40%, breaking the high level since November 28, 2023. It rose more than 9 basis points during the day, about 4.35% at the end of the bond market, and about 4 basis points during the day. The cumulative increase of about 15 basis points this week was about 15 basis points, the biggest two-day increase since the beginning of February.

The 2-year US bond yield, which is more sensitive to interest rate prospects, fell 4.69% at the beginning of the European market. The US stock market rose to 4.73% before the market, breaking the high level since March 19 for 2 consecutive days, rising by nearly 3 basis points during the day. At the end of early trading, the increase leveled off and then declined. At the end of the bond market, it was about 4.69%, falling by nearly 2 basis points during the day, and falling after two consecutive days of rising.

The US dollar index hit a new high for more than four months, then turned down in the intraday session, and Bitcoin fell below $65,000 in the intraday period

The ICE US Dollar Index (DXY), which tracks the exchange rate of a basket of six major currencies including the US dollar against the euro, rose to 105.10 before the European stock market, breaking the high level since November 14, 2023 for two consecutive days. The intraday rise was less than 0.1%. European stocks continued to decline after turning before the market. US stocks fell below 104.70 and a new daily low in early trading, falling more than 0.3% during the day.

By the close of the US stock market on Tuesday, the US dollar index was below 104.80, falling nearly 0.3% during the day; the Bloomberg US dollar spot index, which tracks the exchange rate of the US dollar against ten other currencies, fell more than 0.1%, falling to the same high level since February 13, and the US dollar index both fell after rebounding on Monday.

Among non-US currencies, the Japanese yen, which fell for two days in a row, rose to 151.80 against the Asian market, and continued to be close to the high level since mid-1990, which was set at 152.00 last Thursday. European stocks both turned up before and during the day. US stocks fell below 151.50 in early trading to a new daily low. US stocks closed slightly below 151.60 and fell slightly during the day; EUR/USD fell below 1.0730 before the European stock market, breaking the low level since February 14. The European stock market traded close to 1.1.30. 0780 hit a new daily high, rising more than 0.3% during the day. US stocks were at the close Above 1.0760; GBP/USD was close to a new daily high of 1.2580 in early trading, breaking away from the low since February 14 when it fell below 1.2540 on Monday. US stocks were above 1.2570 at the close.

The offshore renminbi (CNH) fell to a new low of 7.2662 against the US dollar in early Asian trading. US stocks turned up in early trading. The increase expanded after the announcement of US vacancies. It rose to a new daily high of 7.2522 in early trading, and rebounded 140 points from the daily low, getting rid of the risk of falling below 7.28 last Monday. At 4:59 Beijing time on April 3, the offshore RMB was 7.2546 yuan against the US dollar, up 49 points from the end of Monday's New York session. It rebounded after falling back on Monday, and rose on the second day of the last five trading days.

Bitcoin (BTC) reached a new daily high of $69,900 in early Asian trading, then continued to decline. After falling below $67,000 in the Asian session, US stocks fell below $66,000 at the beginning of the market, breaking the low since March 24, falling more than $5,000 and falling more than 7% from the daily high. US stocks rose above $66,000 in midday trading, and US stocks were above $66,000 at the close of trading, falling more than 5% in the last 24 hours.

Crude oil closed up nearly 2% and hit a five-month high over the past few days

International crude oil futures remained strong throughout the day on Tuesday. When European stocks hit a new daily high in early trading, US WTI crude oil was close to $85.50, up nearly 2.1% during the day, and Brent crude was close to $89.10, up nearly 1.9% during the day.

In the end, crude oil closed higher for three consecutive trading days. WTI crude oil futures for May closed up $1.44, or 1.72%, to $85.15 per barrel, closing high for two consecutive days since October 27, 2023; Brent crude oil futures for June closed up $1.50, or 1.72%, to $88.92 per barrel, breaking the high level since October 27, 2023 for three consecutive trading days.

US gasoline and natural gas futures rose sharply. NYMEX gasoline futures for May, which fell back on Monday, closed up about 1.8% to 2.7589 US dollars/gallon, breaking the high level since March 19; NYMEX natural gas futures closed up 1.36% to 1.8620 US dollars/million British thermal units in May, rising for 3 consecutive days to March 6.

Lunan aluminum rose nearly 2%, and copper rose to a two-week high for two consecutive days, and gold hit a record closing high for four days

London basic metals futures mostly rose and rose more than 1% on Tuesday, making an overall good start to the second quarter. Lun Aluminum, which led the rise, rose more than 1.8%, to a new high since the end of December last year. With Luntong, Lunzinc, and Lunnickel, they all rose for two consecutive days. Luntong closed extremely close to the 9,000 US dollar mark for the first time in two weeks. Lunzinc continued to break away from its low level since March 1, and Lunn Nickel hit a new high of more than a week. Renxi, which fell last Thursday on the previous trading day, rebounded to a two-week high. Meanwhile, Lun lead, which rebounded more than 2% last Thursday, fell more than 1%, falling to a one-week high.

New York gold futures maintained gains throughout the day, and the Asian spot gold market maintained gains after turning higher in early trading. At the end of the session, futures rose to 2,300 US dollars, up 1.9% during the day. Spot gold US stocks were close to 2,280 US dollars at the end of the session, rising more than 1.2% during the day, all of which hit record highs for three consecutive trading days.

Both futures and spot gold hit record closing records for four consecutive trading days, rising for six consecutive trading days. COMEX June gold futures closed up 1.09% to $2281.8 per ounce. Spot gold was above $2,270 at the close of the US stock market, rising more than 1% during the day.

New York Futures rose for four consecutive trading days. COMEX silver futures closed up 3.39% to 25.923 US dollars/ounce in May, breaking the high level since May 2023 and approaching 26 US dollars for the first time in 11 months.

Editor/jayden