Earnings Report: Guizhou Space Appliance Co., LTD Missed Revenue Estimates By 16%

Earnings Report: Guizhou Space Appliance Co., LTD Missed Revenue Estimates By 16%

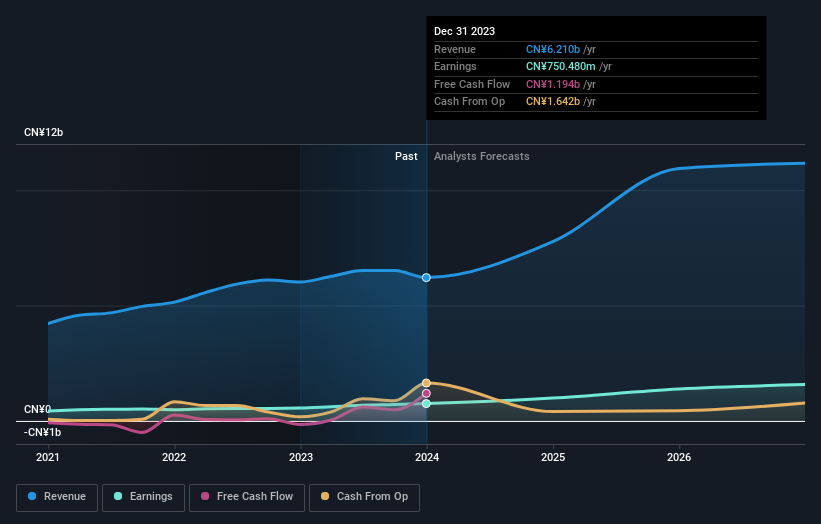

It's shaping up to be a tough period for Guizhou Space Appliance Co., LTD (SZSE:002025), which a week ago released some disappointing yearly results that could have a notable impact on how the market views the stock. It looks like a weak result overall, with both revenues and earnings falling well short of analyst predictions. Revenues of CN¥6.2b missed by 16%, and statutory earnings per share of CN¥1.65 fell short of forecasts by 4.5%. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

对于贵州航天器股份有限公司(SZSE:002025)来说,这将是一个艰难的时期,该公司一周前发布了一些令人失望的年度业绩,这可能会对市场对该股的看法产生显著影响。总体而言,这似乎是一个疲软的业绩,收入和收益都远低于分析师的预期。62亿元人民币的收入下降了16%,法定每股收益为1.65元人民币,比预期低4.5%。分析师通常会在每份收益报告中更新他们的预测,我们可以从他们的估计中判断他们对公司的看法是否发生了变化,或者是否有任何新的问题需要注意。因此,我们收集了最新的财报后法定共识估计,以了解明年可能会发生什么。

Taking into account the latest results, the current consensus from Guizhou Space Appliance's five analysts is for revenues of CN¥7.77b in 2024. This would reflect a substantial 25% increase on its revenue over the past 12 months. Per-share earnings are expected to soar 32% to CN¥2.17. Yet prior to the latest earnings, the analysts had been anticipated revenues of CN¥9.52b and earnings per share (EPS) of CN¥2.33 in 2024. Indeed, we can see that sentiment has declined measurably after results came out, with a real cut to revenue estimates and a small dip in EPS estimates to boot.

考虑到最新业绩,贵州航天器五位分析师目前的共识是,2024年的收入为77.7亿元人民币。这将反映其收入在过去12个月中大幅增长25%。每股收益预计将飙升32%,至2.17元人民币。然而,在最新财报公布之前,分析师曾预计2024年的收入为95.2亿元人民币,每股收益(EPS)为2.33元人民币。事实上,我们可以看到,业绩公布后,市场情绪已显著下降,收入预期实际下调,每股收益预期也将小幅下降。

It'll come as no surprise then, to learn that the analysts have cut their price target 5.9% to CN¥60.84. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on Guizhou Space Appliance, with the most bullish analyst valuing it at CN¥78.00 and the most bearish at CN¥47.74 per share. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

因此,得知分析师已将目标股价下调5.9%至60.84元人民币也就不足为奇了。但是,还有另一种思考价格目标的方法,那就是研究分析师提出的价格目标范围,因为范围广泛的估计可能表明,对业务可能的结果有不同的看法。对贵州航天器有一些不同的看法,最看涨的分析师将其估值为78.00元人民币,最看跌的为每股47.74元人民币。这些目标股价表明,分析师对该业务的看法确实有所不同,但这些估计的差异不足以向我们表明,有些人押注取得巨大成功或彻底失败。

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The analysts are definitely expecting Guizhou Space Appliance's growth to accelerate, with the forecast 25% annualised growth to the end of 2024 ranking favourably alongside historical growth of 17% per annum over the past five years. Other similar companies in the industry (with analyst coverage) are also forecast to grow their revenue at 22% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Guizhou Space Appliance is expected to grow at about the same rate as the wider industry.

了解这些预测的更多背景信息的一种方法是研究它们与过去的业绩相比如何,以及同一行业中其他公司的表现。分析师们肯定预计贵州航天电器的增长将加速,预计到2024年底的年化增长率为25%,而过去五年的历史年增长率为17%。预计该行业其他类似公司(有分析师报道)的收入也将以每年22%的速度增长。考虑到收入增长的预测,很明显,贵州航天器预计将以与整个行业大致相同的增长速度。

The Bottom Line

底线

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Guizhou Space Appliance. Sadly, they also downgraded their revenue forecasts, but the business is still expected to grow at roughly the same rate as the industry itself. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

最大的担忧是,分析师下调了每股收益预期,这表明贵州航天器可能会面临业务不利因素。遗憾的是,他们还下调了收入预期,但预计该业务的增长速度仍将与该行业本身大致相同。此外,分析师还下调了目标股价,这表明最新消息加剧了人们对业务内在价值的悲观情绪。

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Guizhou Space Appliance going out to 2026, and you can see them free on our platform here.

话虽如此,公司收益的长期轨迹比明年重要得多。我们对贵州航天器将于2026年问世进行了预测,您可以在我们的平台上免费查看。

And what about risks? Every company has them, and we've spotted 1 warning sign for Guizhou Space Appliance you should know about.

那风险呢?每家公司都有它们,我们发现了一个你应该知道的贵州航天器警告标志。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。