Source: CFA Reporter: Yan Jun

① A Goldman Sachs research report raising the target price of “three barrels of oil” sparked ridicule from netizens; ② Goldman Sachs gave reasons for the recommendation: strong dividend rate and potential share buybacks; ③ despite the suspension of high A-share dividends on the first day of April, the institution remains optimistic for a long time.

A research report by Goldman Sachs recommending buying CNPC and CNOOC to raise the target price of “three barrels of oil” attracted attention in the market.

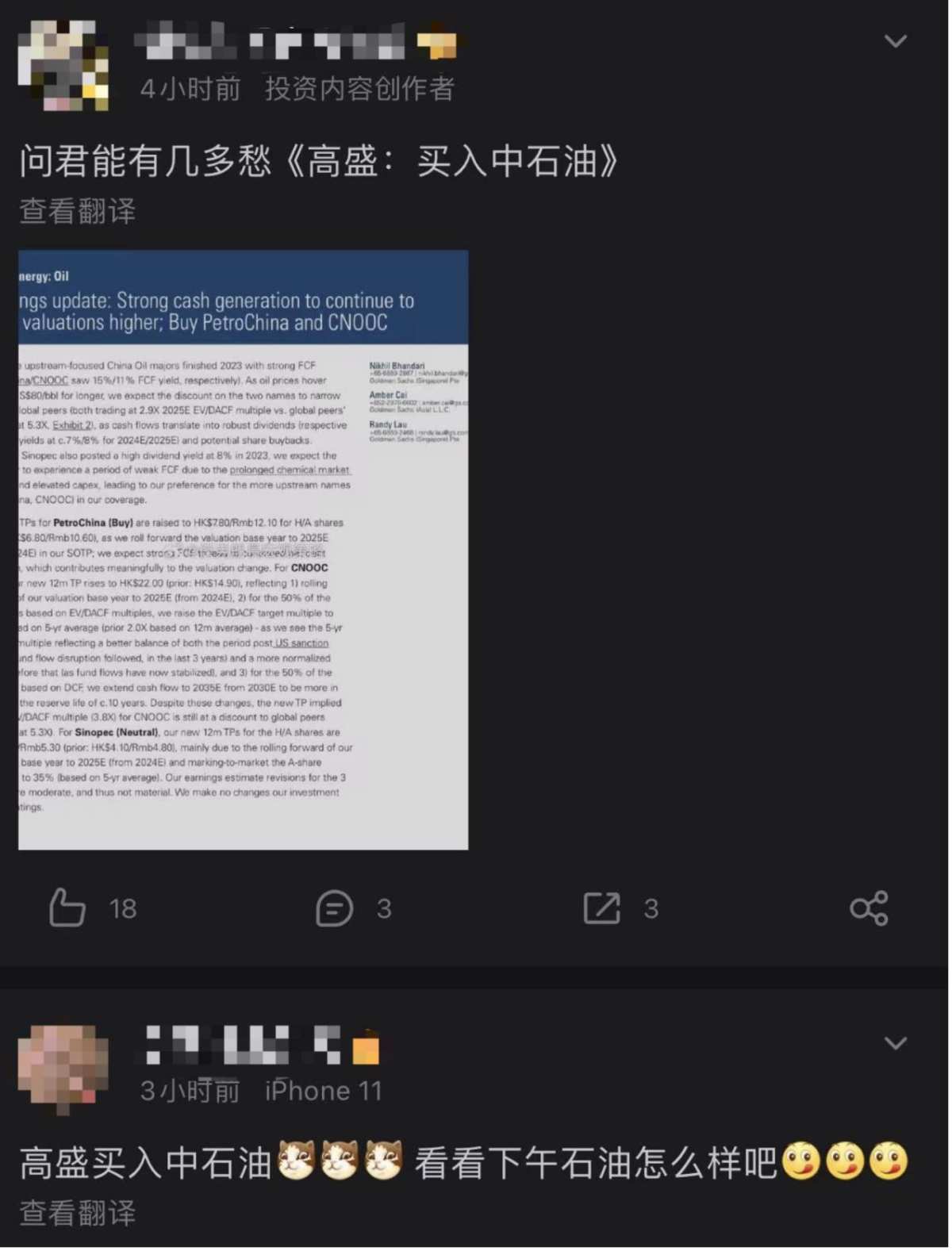

According to Goldman Sachs's latest research report, the CNOOC rating is “buy,” and the target price for the next year was raised to HK$7.8 for Hong Kong stocks and $12.1 for A-shares; to give CNOOC a “buy” rating, the target price for Hong Kong stocks was raised from HK$14.9 to HK$22; Goldman Sachs raised the target prices for CNOOC's Hong Kong stocks and A-shares from HK$4.1 to HK$4.2 and $4.8 to 5.3, respectively.

Regarding the reasons for giving CNPC and CNOOC purchase ratings and raising the target price of “three barrels of oil,” Goldman Sachs believes that strong cash flow will continue to drive up the company's valuation.

However, as soon as the research report came out, it immediately attracted the attention of the market. Some netizens ridiculed “if you ask how worried you can be, Goldman Sachs bought CNPC.” Other netizens said, is it another time to “buy back from XX, the villa is near the sea”?

Goldman Sachs: Strong dividend rate and potential share buybacks to raise target price of “three barrels of oil”

Goldman Sachs said that as oil prices maintain a longer-term trend of 80 US dollars per barrel, the free cash flow yields of CNPC and CNOOC are 15% and 11%, respectively. It is expected that the discount for these two stocks will narrow compared to the world. As cash flow turns into strong dividends and potential stock repurchase plans, Goldman Sachs is optimistic about the stock price performance of CNPC and CNOOC.

In the latest research report, Goldman Sachs raised the target price of “three barrels of oil”:

For the “buy” rating given to CNPC, the target price was raised to HK$7.8 for Hong Kong stocks and $12.1 for A-shares within the next year. In the March 26 research report, Goldman Sachs set the target prices for CNPC Hong Kong stocks and A-shares at HK$6.8 and HK$10.6.

For CNOOC's “buy” rating, the new 12-month target price was raised from HK$14.9 to HK$22.00.

Although Goldman Sachs gave Sinopec a “neutral” rating, it still raised its target price for the next year. CNOOC's target prices for Hong Kong stocks and A-shares were raised from HK$4.1 to HK$4.2 and RMB 4.8 to 5.3 yuan, respectively.

Goldman Sachs said that the above valuation base year was rolled forward from 2024 to 2025, and the “three barrels of oil” profit revisions were moderate and would not change the investment rating. In addition, Goldman Sachs also said that if oil prices remain at $80 per barrel, CNPC will be an ideal choice for long-term investors, and this price level is expected to continue until 2025.

Why can “three barrels of oil” win the favor of Goldman Sachs and raise the target price over and over again?

It is easy to see from the annual report data that steady performance growth and continued high dividends have brought “three barrels of oil” long-term stable benefits through fluctuations in oil prices to a certain extent.

First, let's focus on petroleum. The annual report mentioned that in 2023, the Group achieved an average crude oil price of 76.6 US dollars, down 16.8% from 92.12 US dollars in the same period last year; revenue for the full year of 2023 was 3.01 trillion yuan, a decrease of 7% year on year, but this decrease was less than the drop in oil prices; net profit to mother was 161,146 billion yuan, an increase of 8.3% year on year, a record high. It achieved free cash flow of 176.122 billion yuan, an increase of 17.1% year over year, and also reached a record high.

Looking at CNOOC, in 2023, it achieved operating revenue of 416.609 billion yuan, down 1.3% year on year; net profit to mother was 123.843 billion yuan, down 12.6% year on year.

Sinopec's revenue in 2023 was 3212.22 billion yuan, down 3.2% year on year; realized net profit of 60.463 billion yuan, down 9.9% year on year.

Although the revenue of the “three barrels of oil” all declined by varying proportions due to international oil prices, the dividends were not easy.

CNPC plans to distribute a cash dividend of 0.23 yuan per share for the end of 2023, with a total dividend of about 42,095 billion yuan;

For CNOOC's three annual dividends, it is proposed to pay a final dividend of HK$0.66 per share (tax included) to all shareholders, along with an interim dividend of HK$0.59 (tax included) per share already paid. The total final dividend and interim dividend for 2023 are HK$1.25 per share (tax included);

Sinopec's cash dividend for the full year of 2023 was RMB 0.345 per share (tax included), plus the repurchase amount during the year, and the 2023 dividend ratio reached 75% after the combined calculation.

How does the agency view the “Goldman Sachs buy-back” joke?

High dividends missed the feast of thousands of stocks rising and falling today. “Three barrels of oil” had mixed ups and downs.

At the close of trading on April 1, CNPC and Sinopec A shares fell by 1.42% and 0.47% respectively, while CNOOC Hong Kong stocks surged 2.95%.

However, despite the fall in CNPC's stock price, today's main capital inflow was 109 million yuan, a net inflow for 6 consecutive days, with a cumulative net inflow of 477 million yuan. The cumulative increase in the past 5 trading days was 4.96%, and the cumulative increase in the past 30 trading days was 12.6%.

According to the industry, netizens ridiculed nothing more than concerns about the “three barrels of oil” stock price. In the first quarter that just ended, CNPC and Sinopec increased by 39.94, 16.82%, and 35.59%, respectively. According to domestic brokerage analysts, the high dividend strategy is still worth looking forward to in the future.

Some brokerage firms pointed out that since this year, in the energy sector of central state-owned enterprises represented by three barrels of oil, stock prices and corporate valuations have increased markedly in the context of ensuring energy security and the transformation of new energy sources. However, in comparison with domestic non-state-owned enterprises in the same industry and overseas enterprises in the same industry, the current valuation is still relatively low. As the profitability gap between central state-owned enterprises represented by three barrels of oil gradually narrows, the valuations of leading central state-owned enterprises such as CNPC still have significant prospects of improving, and valuations may continue to be repaired.

For example, in the April gold stock recommendations, CNOOC was recommended by 4 brokerage firms, including Dongxing Securities and Ping An Securities. After the Ningde era, it was the second-most recommended individual stock by brokerage firms. The brokerage firm said it is optimistic that in the future, under a stable oil price center, the company will have high production storage space, strong cost control capabilities, and high performance stability. The company's integrated exploration and development strategy continues to reduce costs and increase efficiency, has steady cash flow, and maintains a balance between high dividends and high capital expenditure over a long period of time.

edit/lambor