Big names such as Zhang Kun and Fu Pengbo have come to hold heavy hidden stocks

Commodities broke out of the big dark horse, not copper, nor gold.

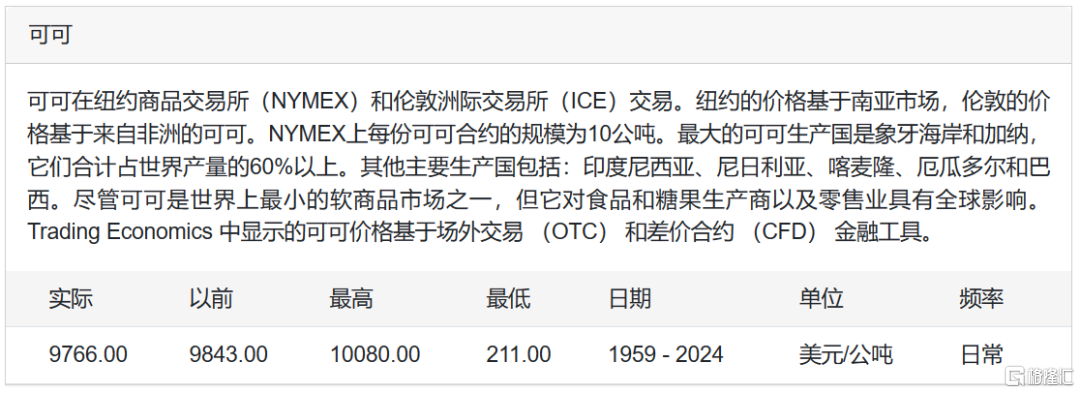

1

Cocoa crisis! Prices soared, surpassing Nvidia

This year's hottest investment products came from commodities, and Nvidia's crazy gains were beyond the reach of Nvidia.

Cocoa futures recently broke through the $1,080/ton level like never before, reaching a record high.

At the beginning of February, the price of cocoa surpassed 5,000 US dollars. In less than two months, the price has directly doubled, surpassing copper, which is regarded as an economic weather vane. This is the first time in history.

Over the past year, Coco's cumulative increase was as high as 300%, which is larger than the cosmic chip factory and Nvidia, the high-profile “AI shovel seller”.

(The content of this article is a list of objective data and information and does not constitute any investment advice)

Behind the sharp rise in cocoa is the world facing its worst supply shortage in decades. West Africa is the world's largest producer of cocoa, accounting for 70% of the world's market share. Due to bad weather and crop diseases, major cocoa growing countries in West Africa rarely experienced large-scale crop failures, causing the world to face the biggest shortage of cocoa supply in more than 60 years.

According to the latest information, major African cocoa plants in Côte d'Ivoire and Ghana have stopped or slowed cocoa processing.

Faced with rising prices, hedge funds were also moved by the news and poured into the cocoa market, thereby exacerbating record price spikes caused by poor harvests in West Africa.

According to the US Commodity Futures Trading Commission data, traders have accumulated $8.7 billion in London and New York cocoa futures contracts and are betting that the price will continue to rise, which is the biggest increase in history in US dollars.

The main raw material of chocolate is cocoa powder. As the price of cocoa futures rises, the price of chocolate raw materials rises. Furthermore, March 31 is Easter, an important holiday in the West. It coincides with the peak of chocolate consumption, and the demand for chocolate is also rising.

The price of chocolate has soared. The average unit price of chocolate eggs in the US has risen 12% compared to last year, and the price of some chocolate eggs in the UK has soared 50%.

Recently, some stores in Brazil even told consumers that chocolate eggs can be purchased through loans and installment payments. This news once made headlines in the region.

Commodities have been hot recently. International gold prices have hit record highs one after another. Cocoa futures have surged unusually. The industry's attention to the commodity market is heating up, and many asset management giants have called for a “commodity bull market.”

According to Goldman Sachs's latest report, commodity prices are expected to rise this year, and the European and American central banks are expected to cut interest rates, which will help support industrial metal prices and consumer demand. The return on commodities is expected to reach 15% in 2024.

Macquarie Group said earlier this month that commodity prices are entering a new round of cyclical rise, driven by tighter supply and an improvement in the global economy.

2

The Japanese stock market surged, and the yen fell to a 34-year low

The Nikkei 225 Index surged 20.63% in the first quarter, the biggest quarterly increase on record.

On February 22, after breaking through the level of Japan's bubble economy in 1989, the Nikkei 225 Index continued to hit record highs this quarter. The main factors supporting the rise in the Japanese stock market include improvements in corporate governance, foreign purchases brought about by the weakening yen, and expectations that the Bank of Japan will stick to a loose monetary policy.

In terms of the international market, after all, the market realized that Japan's end to negative interest rates was a favorable implementation.

The Bank of Japan has just put an end to negative interest rates and announced interest rate hikes for the first time in 17 years. Unexpectedly, the yen's decline rapidly widened further, and the yen fell to its lowest level since 1990.

Although the Bank of Japan has ended its negative interest rate policy, it is expected that the huge interest rate spread between Japan and the US will still exist.

The yield on US two-year treasury bonds is about 4.593%, and the yield on Japanese two-year treasury bonds is about 0.191%. As long as this spread does not change, investors borrow cheap yen and exchange dollars in exchange for assets with higher returns, and this operation exacerbates the depreciation of the yen.

Japan's Ministry of Finance official Masato Kanda said that speculation is an important reason behind the fall in the yen exchange rate. He issued a stern warning that appropriate measures will be taken against excessive actions, and no options will be ruled out.

According to media reports, Japan's Ministry of Finance, the central bank, and the Financial Services Agency held an emergency meeting. After the meeting, Masato Kanda said that the trend of yen is receiving close and urgent attention. The yen fluctuated by 4% in the last two weeks, which is no longer a moderate change. Kanda revealed that if the development of the foreign exchange market has an impact on the Japanese economy, the central bank will respond through monetary policy measures.

Japanese Prime Minister Fumio Kishida said that foreign exchange fluctuations are being closely monitored with a high degree of urgency, and no measures are ruled out to deal with disorderly foreign exchange fluctuations; it is appropriate for the Bank of Japan to shift to a new dimension of monetary policy while maintaining an easy monetary policy; he hopes that the Bank of Japan will consider the government's commitment to ensure the complete end of deflation when guiding the policy.

Nomura's Willcox believes that the Japanese authorities are now more inclined to “talk.” He said, “Central banks often intervene when the market is unexpected. We're all talking about it right now, so I think they'd rather talk than act, but apparently you'll never be able to predict it.”

3

Big names such as Zhang Kun and Fu Pengbo have come to hold heavy hidden stocks

The 2023 fund annual reports were revealed one after another, and well-known fund managers' hidden heavy stocks were revealed.

In the Ruiyuan Growth Value Hybrid Fund managed by Fu Pengbo and Zhu Yi, the largest hidden holdings are Tencent Holdings, which added high-test shares and reduced their holdings in Xinzhoubang and TCL Central.

Zhao Feng greatly increased his holdings in Baosteel, Meituan, Yuantong, and Maotai; joined China Financial Insurance and Yifeng Pharmacy.

Zhang Kun, the first brother of the public fund, released his annual report. Judging from his hidden stocks, in the second half of last year, Zhang Kun added new drugs to companies such as Mingkang, Samsonite, Tiger Pharmaceuticals, L'OCCITANE, Tongrentang Sinopharm, and China Resources Vientiane Life.

Among them, Pharmaceutical Kangde and Tiger Pharmaceuticals are CXO companies, and Tongrentang Sinopharm is engaged in the production, retail and wholesale business of traditional Chinese medicine products. Samsonite Group is the world's largest luggage company. L'OCCITANE (L'OCCITANE) is a global manufacturer of cosmetics and care products. China Resources Vientiane Life is a leading provider of property management and commercial operation services in China.

In the latest annual report, Zhang Kun proposed that as China's economy enters a stage of high-quality growth, the investment framework can remain stable, but in some specific areas more stringent standards need to be adopted:

First, there is corporate governance. In an age of extensive growth, growth can solve many problems. However, in an age of high-quality growth, inefficient growth is no longer meaningful. We expect management to allocate the company's capital more carefully, evaluate the difference in opportunity costs between investing in new businesses and helping shareholders increase old businesses. The importance of dividends and repurchases and cancellations has increased significantly. If management's ability is poor, shareholders' capital may be wasted in disguise.

As an investor, you need to carefully evaluate management's ability and willingness to give back to shareholders. The capital market is an amplifier, and both positive and negative aspects will be amplified. We believe that the effects of amplification will continue to increase over time.

Second, the company's valuation. We believe that in an age of high-quality development, the basic probability that the company will continue to grow rapidly is declining. Unless the company is in a prominent industry trend and has rare competitiveness (yet such star companies are often highly valued), we should not overestimate our ability to judge unconsensual continued high growth. We will carefully consider the company's valuation level in the illiquid primary market and pay the premium very carefully.

The third is the business model of the enterprise. In an age of high-quality growth, the unique “characteristics” of an enterprise that are difficult to quickly imitate are even more important. All the profits and losses of an enterprise come from all decisions in history. Sometimes some of the most important decisions even come from the distant past. Perhaps the management that made the decision did not work for the company long ago, but this decision continues to play an important role.

The former CEO of Nabescu once joked, “Genius invented Oreo, and we are responsible for inheriting the legacy.” Even in the technology industry, which is changing rapidly in the usual sense, companies are becoming long-lived. Among the top 20 technology companies in the world by market capitalization, the youngest is Meta founded in 2004. The giants that look “old” are still lightweight, and the top two companies by global market capitalization were founded in the 70s.

In an era of significant growth, an enterprise's new strategic decision may quickly take the enterprise to a major level; in an era of limited growth, the marginal effect of a new strategic decision inevitably declines. And when a really significant incremental trend comes, such as AI (artificial intelligence), when all companies do their best, the resources they have will be one of the winners and losers.

In this round of AI revolution, we see that tech giants are still leading the way. Their rapidly building the strongest infrastructure and recruiting the world's best talents are important conditions, and niche businesses where they can continue to generate cash flow are prerequisites for all of this. At the same time, it also increases fault tolerance in business operations.

In summary, we believe that these changes should be structural. The “vigorous miracle” and “black chicken becomes phoenix” that often occurred during the era of extensive growth will be more difficult to replicate. The operation of enterprises needs to be more refined, and we also need to use stricter and more detailed standards to evaluate investment targets.