Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Yangmei Chemical Co.,Ltd (SHSE:600691) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Yangmei ChemicalLtd Carry?

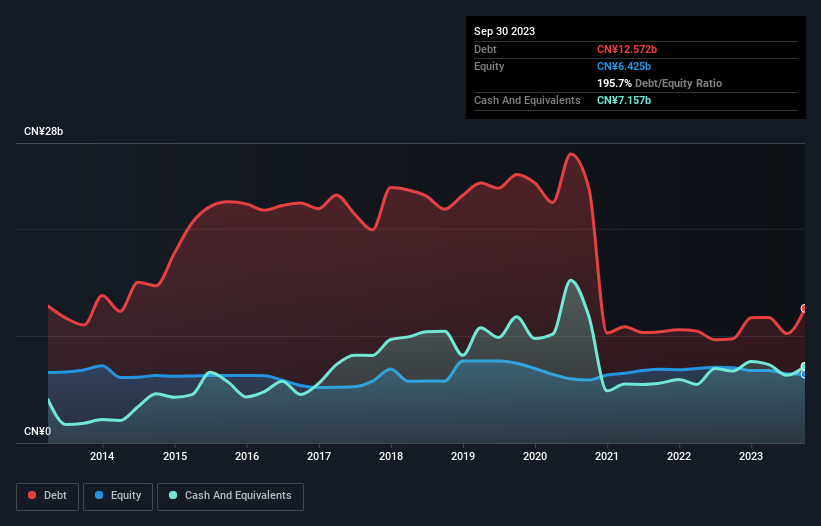

The image below, which you can click on for greater detail, shows that at September 2023 Yangmei ChemicalLtd had debt of CN¥12.6b, up from CN¥9.74b in one year. However, because it has a cash reserve of CN¥7.16b, its net debt is less, at about CN¥5.41b.

A Look At Yangmei ChemicalLtd's Liabilities

According to the last reported balance sheet, Yangmei ChemicalLtd had liabilities of CN¥16.1b due within 12 months, and liabilities of CN¥1.64b due beyond 12 months. Offsetting these obligations, it had cash of CN¥7.16b as well as receivables valued at CN¥2.24b due within 12 months. So its liabilities total CN¥8.38b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company's CN¥5.65b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Yangmei ChemicalLtd can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Yangmei ChemicalLtd made a loss at the EBIT level, and saw its revenue drop to CN¥15b, which is a fall of 22%. That makes us nervous, to say the least.

Caveat Emptor

While Yangmei ChemicalLtd's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost CN¥365m at the EBIT level. When we look at that alongside the significant liabilities, we're not particularly confident about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. It's fair to say the loss of CN¥352m didn't encourage us either; we'd like to see a profit. In the meantime, we consider the stock to be risky. For riskier companies like Yangmei ChemicalLtd I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.