Source: An Insight into Finance

“Rushing high and falling” and “opening high and moving low” are secondary market pairs$MEITUAN-W (03690.HK)$The reaction to the latest earnings report.

On the first trading day after Meituan released its earnings report (March 25), Meituan's stock price soared up and fell from 9% to 5%; on the second trading day (March 26), after Meituan opened more than 2%, the stock price plummeted. At one point, it fell more than 1% intraday and finally closed at HK$93.4 per share. The latest total market value was HK$582.32 billion.

It can be seen from this that the market is concerned about Meituan's financial report. What are the hidden risks?

On the face of it, Meituan's latest financial report for the fourth quarter and year of 2023 is an impressive report card.

Financial reports show that last year, Meituan achieved revenue of 276.74 billion yuan (RMB, same below), up 25.8% year on year, adjusted net profit of 23.25 billion yuan, up 721.6% year on year; achieved revenue of 73.7 billion yuan in the fourth quarter, up 22.6% year on year, and adjusted net profit of 4.38 billion yuan, up 427.6% year on year.

So what is the market really worried about?

Live locally, the war starts again

Meituan started with a group purchase. “Local Life” is undoubtedly an important base for Meituan, and it is also the core business that drives Meituan's core business.

Currently, traffic giants such as Douyin and Kuaishou are attacking the local lifestyle service circuit and are making a lot of money. According to the “2023 Data Report” released by Douyin, the total transaction volume of the Douyin Life Service Platform increased by 256% in 2023, with more than 4.5 million stores, covering a total of 370+ cities; the number of registered service providers increased 1.79 times, the number of merchants cooperated with service providers nearly 2 times, and the total transaction volume of service providers increased nearly 8 times.

At the same time, the number of group buying experts entering the Douyin platform increased 2.89 times, and talent visits helped physical merchants increase revenue by 94.6 billion dollars. Compared with 2022, the platform's short video transaction volume increased by 83%, and the platform's live streaming transaction volume increased 5.7 times.

As can be seen, Douyin is attacking Meituan's strategic hinterland, which will undoubtedly affect Meituan's future growth. This is probably one of the risk points that capital markets are most concerned about.

Faced with Douyin's ferocious offensive, Meituan decided to respond, and a strategy codenamed “Beacon” appeared within Meituan: in 2023, this strategy was seen as a key plan to deal specifically with Douyin's offensive in the local field of life.

As can also be seen from the latest financial reports, Meituan has begun to step down and take on Douyin.

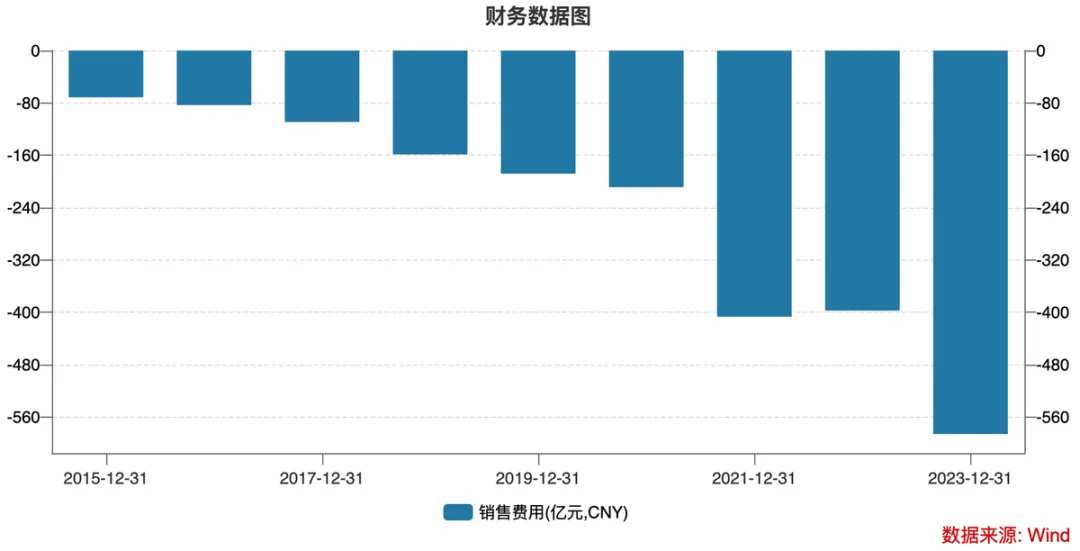

First, Meituan's “money-burning” subsidies are increasing. More specifically:

Sales and marketing expenses for the first quarter of 2023 were 10.4 billion yuan, an increase of 14.6% over the previous year;

Sales and marketing expenses for the third quarter of 2023 were 16.9 billion yuan, up 55.3% year on year and 16.2% month on month;

Sales and marketing expenses for the fourth quarter of 2023 were $16.7 billion, up 55.3% year-on-year, and the sales expenses ratio increased from 17.9% to 22.7%.

In 2023, Meituan's sales and marketing expenses reached 58.6 billion yuan, a year-on-year increase of 47.5%, and its share of revenue also increased from 18.1% in the previous year to 21.2%.

In other words, Meituan spent one-fifth of its revenue on marketing last year.

In response, Meituan said that the increase in sales and marketing expenses as a percentage of revenue is mainly due to the increase in user incentives, promotion and advertising expenses due to the recovery of consumption, changes in the business environment and business strategies. The decline in operating profit is mainly due to higher subsidy rates.

Meituan's active response seems to have temporarily held the base.

In the fourth quarter of 2023, Meituan's core local commercial revenue increased 26.8% year over year to 55.1 billion yuan; operating profit increased 11.1% year over year to 8 billion yuan. However, the operating margin of the core local business segment declined from 16.6% to 14.5% in the fourth quarter.

Second, judging from specific strategies, Meituan is drastically increasing livestreaming/special group purchases, increasing user incentives, etc., and has launched a first-level portal for short videos and live broadcasts on the app's homepage.

In January of this year, Zhang Chuan, president of Meituan Arridian, also stated in an internal open letter that the key to 2024 is low prices every day.

From this perspective, the pace of Meituan's “money-burning” subsidies will not slow down for the time being; this will also limit Meituan's profitability.

Judging from the external environment, it is likely that the attacks on the local lifestyle sector will not stop in the short term by the internet giants with massive traffic in their hands.

In the face of competitors with traffic advantages, Meituan's in-store business is easily impacted.

Major withdrawal of new businesses

Faced with this financial report, another risk point that the market is worried about may be that there is less and less room to imagine Meituan's future growth.

This is mainly because Meituan's strategy for new businesses has begun to shrink drastically.

According to financial reports, Meituan's new businesses include Meituan Premium, Baby Elephant Supermarket, Express Donkey, Online Car-hailing, Bicycles and Motorcycles, Power Banks, and Restaurant Management Systems.

Now that the internet dividends are disappearing, the strategies of all giants are beginning to shift and “survive” by reducing costs and increasing efficiency.

In this context, the new business, which continues to lose money, has undoubtedly become a major burden for Meituan. Among them, the loss situation of Meituan Preferred was particularly severe, and it became the main target of Meituan's contraction.

In 2021, the operating loss of Meituan's new business reached 38.394 billion yuan, of which Meituan Preferred's cumulative loss exceeded 20 billion yuan.

Meituan suddenly realized that community group buying was a protracted battle. As a result, Meituan began to shrink its community group buying business in April 2022, and the contraction trend has continued until now.

Financial reports show that in 2023, the growth rate of Meituan Preferred will slow down due to the fact that the market size of community e-commerce remained basically the same year on year. Despite Meituan Preferential's efficiency improvements in 2023, the amount of losses and loss rates are still significant.

Meituan said that although the efficiency of Meituan Preferred has improved in 2023, the loss amount and loss rate are still significant. The reason is that the growth in the scale of the business fell short of expectations, making it difficult to drastically reduce the cost of each contract.

Furthermore, fierce market competition has made it more difficult to raise product price increases and reduce subsidies. Meituan also stated in financial reports that the community group buying market is more difficult than the company's previous expectations.

Wang Xing, founder and CEO of Meituan, also set the tone at this performance analysis meeting that prioritizes capital allocation in areas with high-quality return on investment.

This means that Meituan's contraction to new businesses will continue and be faster. On the other hand, the contraction in new business has also led to a reduction in losses.

According to the latest financial report, in the fourth quarter of 2023, Meituan's new business lost 4.833 billion yuan, with a loss rate of 26%, the lowest level in history. The main reason for the reduction in losses was Meituan's reduced investment.

Naturally, this has also led to a slowdown in Meituan's new business expansion. In the fourth quarter of 2023, Meituan's new business achieved revenue of 18.565 billion yuan, a year-on-year growth rate of 11.5%, reaching a record low.

This means that there is limited room to imagine Meituan's core business growth. The new business is still burning money and losing money, and no high growth potential can be seen. This is probably one of the internal reasons why the secondary market is concerned about Meituan.

editor/tolk