Does Guizhou Zhenhua E-chem (SHSE:688707) Have A Healthy Balance Sheet?

Does Guizhou Zhenhua E-chem (SHSE:688707) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Guizhou Zhenhua E-chem Inc. (SHSE:688707) makes use of debt. But the more important question is: how much risk is that debt creating?

沃伦·巴菲特曾说过一句名言:“波动性远非风险的代名词。”因此,当你评估公司的风险时,看来聪明的货币知道债务(通常涉及破产)是一个非常重要的因素。与许多其他公司一样,贵州振华电子化工股份有限公司(上海证券交易所代码:688707)也使用债务。但更重要的问题是:这笔债务会带来多大的风险?

When Is Debt Dangerous?

债务何时危险?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

债务可以帮助企业,直到企业难以偿还债务,无论是新资本还是自由现金流。最终,如果公司无法履行偿还债务的法律义务,股东可能会一无所获。但是,更频繁(但仍然昂贵)的情况是,公司必须以低廉的价格发行股票,永久稀释股东,以支撑其资产负债表。当然,债务可以成为企业的重要工具,尤其是资本密集型企业。当我们考虑公司使用债务时,我们首先将现金和债务放在一起考虑。

What Is Guizhou Zhenhua E-chem's Net Debt?

贵州振华电子的净负债是多少?

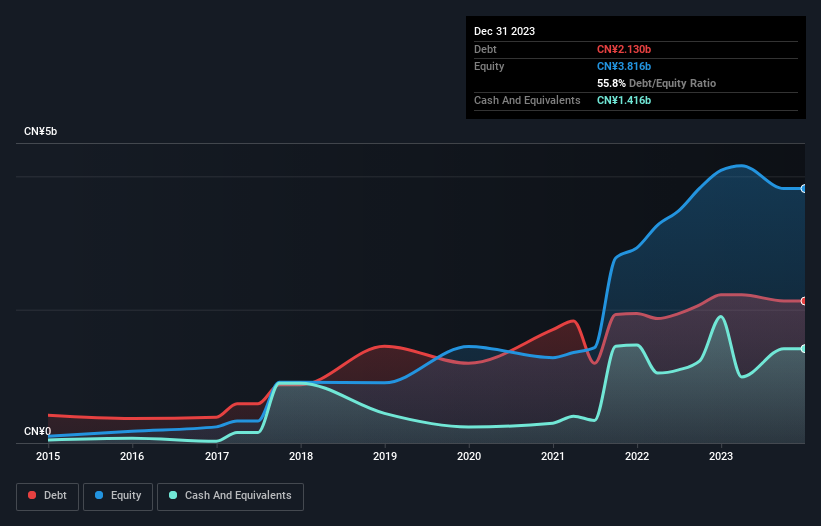

You can click the graphic below for the historical numbers, but it shows that Guizhou Zhenhua E-chem had CN¥2.13b of debt in September 2023, down from CN¥2.22b, one year before. However, because it has a cash reserve of CN¥1.42b, its net debt is less, at about CN¥714.4m.

你可以点击下图查看历史数字,但它显示贵州振华电子在2023年9月有21.3亿元人民币的债务,低于一年前的22.2亿元人民币。但是,由于其现金储备为14.2亿元人民币,其净负债较少,约为7.144亿元人民币。

How Healthy Is Guizhou Zhenhua E-chem's Balance Sheet?

贵州振华电子的资产负债表有多健康?

The latest balance sheet data shows that Guizhou Zhenhua E-chem had liabilities of CN¥3.73b due within a year, and liabilities of CN¥1.21b falling due after that. Offsetting these obligations, it had cash of CN¥1.42b as well as receivables valued at CN¥2.45b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥1.06b.

最新的资产负债表数据显示,贵州振华电子的负债为37.3亿元人民币在一年内到期,12.1亿元人民币的负债在此之后到期。除了这些债务外,它还有14.2亿元人民币的现金以及价值24.5亿元人民币的应收账款将在12个月内到期。因此,其负债超过其现金和(短期)应收账款总额10.6亿元人民币。

Given Guizhou Zhenhua E-chem has a market capitalization of CN¥6.98b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

鉴于贵州振华电子的市值为69.8亿元人民币,很难相信这些负债会构成很大的威胁。话虽如此,很明显,我们应该继续监控其资产负债表,以免情况恶化。

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

为了扩大公司相对于收益的负债规模,我们计算其净负债除以利息、税项、折旧和摊销前的收益(EBITDA),将其利息和税前收益(EBIT)除以利息支出(利息保障)。因此,我们将债务与收益的关系考虑在内,包括和不包括折旧和摊销费用。

While Guizhou Zhenhua E-chem's debt to EBITDA ratio (2.9) suggests that it uses some debt, its interest cover is very weak, at 1.4, suggesting high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Even worse, Guizhou Zhenhua E-chem saw its EBIT tank 92% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Guizhou Zhenhua E-chem's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

尽管贵州振华电子的债务与息税折旧摊销前利润的比率(2.9)表明它使用了部分债务,但其利息保障非常薄弱,为1.4,这表明杠杆率很高。看来该企业会产生巨额折旧和摊销费用,因此其债务负担可能比最初出现的要重,因为息税折旧摊销前利润可以说是衡量收益的丰厚指标。看来很明显,借钱成本最近对股东的回报产生了负面影响。更糟糕的是,在过去的12个月中,贵州振华电子化学的息税前利润下降了92%。如果收益继续保持这一轨迹,那么偿还债务负担将比说服我们在雨中跑一场马拉松更难。资产负债表显然是分析债务时需要关注的领域。但是,未来的收益将决定贵州振华电子未来维持健康资产负债表的能力。因此,如果你想看看专业人士的想法,你可能会发现这份关于分析师利润预测的免费报告很有趣。

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Guizhou Zhenhua E-chem's free cash flow amounted to 36% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

最后,公司只能用冷硬现金偿还债务,不能用会计利润偿还债务。因此,合乎逻辑的步骤是研究息税前利润与实际自由现金流相匹配的比例。在过去三年中,贵州振华电子化学的自由现金流占其息税前利润的36%,低于我们的预期。在偿还债务方面,这并不好。

Our View

我们的观点

On the face of it, Guizhou Zhenhua E-chem's interest cover left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to handle its total liabilities isn't such a worry. Once we consider all the factors above, together, it seems to us that Guizhou Zhenhua E-chem's debt is making it a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with Guizhou Zhenhua E-chem , and understanding them should be part of your investment process.

从表面上看,贵州振华电子的利息保障让我们对该股持初步看法,其息税前利润增长率并不比一年中最繁忙的夜晚那家空荡荡的餐厅更具吸引力。话虽如此,它处理总负债的能力并不令人担忧。综合考虑上述所有因素,在我们看来,贵州振华电子的债务使其有点风险。这不一定是一件坏事,但我们通常会因为降低杠杆率而感到更自在。毫无疑问,我们从资产负债表中学到的关于债务的知识最多。但归根结底,每家公司都可以控制资产负债表之外存在的风险。我们已经确定了贵州振华电子化工的三个警告信号,了解它们应该是您投资过程的一部分。

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

当然,如果你是那种喜欢在没有债务负担的情况下购买股票的投资者,那么请立即查看我们的独家净现金增长股票清单。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。