Once gone, never come back

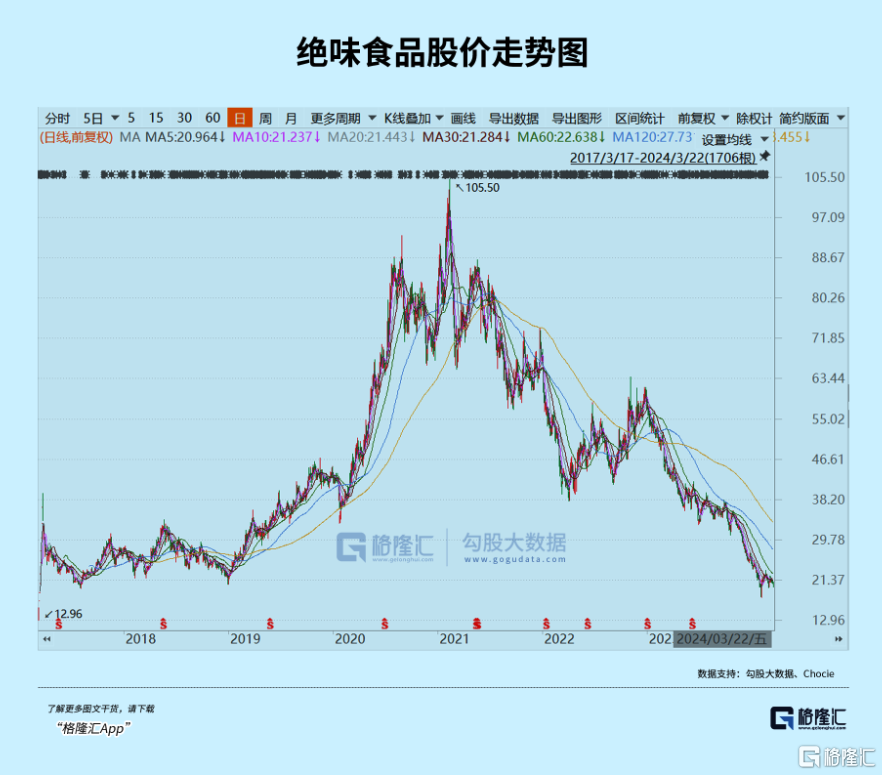

In the A-share market, the market value of the halogenated products giant Zewei Foods soared fivefold in 4 years, reaching a glorious height of 65 billion yuan. However, after the stock price rose above 100 yuan in February 2021, the situation began to reverse. Over the next 3 years, the stock price plummeted by more than 80%, and the market value shrunk by 52 billion yuan.

It's a super roller coaster of delicious stock prices, which is astonishing. At a time when the market was excited before, the valuation once went 90 times (excluding the valuation distortion caused by the sharp drop in 2022 results), and now it has dropped to around 30 times. If you take a rough look at PB, it was 13 times higher at peak in 2021, and now it is 1.73 times, the lowest since its launch in 2017.

By the end of 2023, the total number of shares held by domestic public funds in Jubai Foods was 24.167 million shares, which is at a low level in recent years. Compared to the peak period of 133.7796 million shares held in the fourth quarter of 2020, it is already far different.

Things are out of order. What actually happened behind delicious food falling from the bright light like this?

01 Fundamentals

Before the COVID-19 pandemic, the growth of delicious food was unquestionable. From 2011 to 2019, revenue soared from 1,325 billion yuan to 5.172 billion yuan, with a compound annual growth rate of 18.56%. Net profit to mother soared from 39 million yuan to 801 million yuan, with a compound annual growth rate of 45.9%.

2020 was a huge turning point. Beginning this year, Zhouwei's performance began to slow, and growth seemed to have encountered some bottlenecks. In 2023, revenue is expected to be $72-7.3 billion, up 8.71% — 10.22% year over year. If calculated at the top of 7.3 billion yuan, the compound annual growth rate in the last 4 years has slipped to 9%.

The profit-side performance was even more disastrous. In the first three quarters of 2023, Zhouwei's net profit was 390 million yuan, an increase of 77.57% over the previous year. The growth rate appears to be very high, mainly due to the low base for the same period in 2022. You need to know that net profit to mother fell sharply by 77% in Q3 2022, returning to the level before listing in 2017.

Regarding the 2022 performance of Waterloo, Jubie has given several reasons: some factories and stores suspended production and operations, which had a certain impact on the company's sales revenue and profits; the company increased its support for franchisees, which led to a significant increase in sales expenses; and the cost of raw materials increased significantly, causing a negative impact on gross margin.

It seems understandable that performance has gone awry due to objective factors such as the impact of the epidemic and rising raw material costs. Why by 2023, the epidemic had been completely liberalized, revenue growth still did not improve significantly, and profit performance (first three quarters) only returned to the same period in 2017. Does this suggest that downstream demand has hit a clear ceiling?

Let's look at profitability again. 2023Q3 has a gross margin of only 24.15%, a sharp drop of 11.4% from 35.57% in the 2020Q3, the lowest level since financial data were recorded. In fact, in 2023, the overall price of raw materials for duck by-products has dropped quite a bit compared to 2022, yet gross margin has not stopped declining.

In terms of net interest rate, 2023Q3 was 6.57%, up 3.64% from the end of 2022, but far from 14.77% in 2021. Until 2021, the overall net interest rate level of Zhouwei maintained an upward trend, indicating continued strengthening of profitability. Now a deep hole has been broken out, and the level of profit has been greatly challenged.

In terms of return on net assets (ROE), it was 3.69% in 2022, a sharp drop of 25% from 2016. In addition to the sharp decline in net interest rates in 2022, the continued decline in asset turnover is also an important factor in weakening the ROE trend. In 2016-2022, the asset turnover ratio fell sharply from 1.83% to 0.82%, indicating a certain decline in operating efficiency.

Taken together, the financial performance of the best taste slowed significantly after the pandemic. Growth was no longer as high as in the past, and the good momentum of continuous improvement in profitability came to an abrupt end. Looking at the above dimensions, the decline in stock prices is so deep. Apart from squeezing the valuation bubble, the downward trend in fundamentals is also an important driving force.

02 Growth points

The marinated products market in China is mainly divided into two categories: meal preparation and leisure. The former consumption scenario favors meals, mainly cold dishes, while the latter positions leisure and entertainment as unnecessary, and mainly poultry by-products such as duck neck.

According to Frost & Sullivan, the scale of China's halide products industry is 340 billion yuan. Among them, food brine and casual brine were 210 billion yuan and 130 billion yuan respectively. The overall compound growth rate of the industry was 8% from 2018 to 2022, with food halogen and recreational halogen being 7.2% and 9.3% respectively.

There are many players in the market segment for casual marinated products, including Perfect Taste, Huangshang Huang, Zhou Black Duck, Jiu Jiu Ya, Cao's Duck Neck, Meet Little Yellow Duck, etc., and the market pattern is very scattered. In 2022, the market share of delicious foods was 12.5%, a cumulative increase of 4% over 2018. However, Zhou Heiya shrank slightly by 0.2%, while Huang Shanghuang rose slightly by 0.3%.

Judging from the industry-related data given by the above agencies, the prospects for the halogen products industry are undoubtedly very good. Even in 2022, which was hit hard by the pandemic, the market size of the industry recorded high growth. However, judging from the revenue of the three giants with the highest market share, they are not that optimistic. Among them, Juweiwei's revenue increased slightly by 1.13% year over year, Zhou Heiya's revenue plummeted 18.3% year over year, and Huangshanghuang's revenue plummeted 16.46% year over year. Therefore, investors need to dialectically view the optimistic data given by the agency.

Next, let's take a closer look at the potential growth points of Zhibei in the future, and still analyze them from the two dimensions of volume and price.

Quantitatively speaking, it's nothing more than continuing to open more franchise stores.

It was only in 2015 that Zhouwei officially opened stores, and 61 stores were opened that year. By the end of 2011, the number of stores nationwide reached around 3,700, and expanded to 9,000 by the end of 2016. The A-share market was listed in 2017, and the pace of expansion was accelerated after receiving capital. By 2022, it had expanded to 1,5076 companies. Even in 2022, when the epidemic was severe, the number of newly opened stores reached 1,362.

In the first half of 2023, the total number of stores reached 16,162, and 1,086 new stores were opened in just half a year. Overall, however, because the base for opening stores is getting higher and higher, the growth rate of opening stores will slow down in the future, and single-digit growth is inevitable.

In fact, based on the 31 provinces and 342 cities covered by Exquisite, each city already has nearly 50 stores on average. What scale the total number of stores can be opened in the future will also determine the revenue ceiling.

Tianfeng Securities once gave an aggressive forecast: 38,000. If it can be achieved, there will also be room for more than double the size of the business. However, if you look at the split over many years, the growth rate may not be fast.

In terms of price, Perfect Taste has a more obvious ceiling. On the one hand, duck neck is a casual snack that is not just needed. Future price increases will be more passive due to price increases on the raw materials side. It is already very good that the average annual price increase is in line with the level of inflation. On the other hand, competition in the leisure halide products industry will be very intense, which will suppress the company's price increases. In recent years, up-and-coming casual marinated brands such as Wang Xiaoxian, Marinade Awakening, and Hemp Claw have gradually gained prominence. Receiving venture capital investment in the primary market will put a lot of competitive pressure on Perfect Taste.

At the beginning of 2022, Zhumei Foods raised the price of some products by 5%. In July of the same year, prices were adjusted again for some categories such as duck paws, and the average price increase reached 7% to 10%. However, sales volume grew quite negatively due to the impact of the pandemic or price increases. Previously, the topic “Why young people don't like duck neck anymore” was also trending on Weibo. Some consumers said that it was mainly because the price was getting more and more expensive. This indicates that the price increase is too high and will affect its sales volume.

Judging from the above quantitative and price dimensions, it is an absolute probability event that performance growth will maintain single-digit growth in the future. Also, there must be no major negative brand sentiment or food safety risks.

03 Epilogue

After the outbreak of the epidemic in 2020, a large number of leading A-share consumer companies all experienced a marked slowdown in performance, including Haitian Wei, Zhongju Hi-Tech, Exquisite Foods, Fuling Mustard, Chongqing Beer, etc. From a macro perspective, China's zero consumption growth rate has declined from the rapid phase of 8%-9% before the pandemic to the current level of around 5%. In response to microenterprises, it naturally corresponds to a decline in the performance growth rate of a large number of consumer enterprises.

Moreover, this decline in performance is likely to be irreversible. Because the growth rate of total consumer demand has declined, there is no going back. Unless some consumer companies find a second growth curve, including diversifying their businesses or finding new growth points overseas, the high growth they had before the pandemic is over.

Fundamental growth has declined, and the valuation given by the market will not be as high as it used to be. Expectations for future returns should also be reduced accordingly. Of course, the food and beverage sector will still have many segments with good growth in the future, including ultra-high-end liquor, functional drinks, etc., which are worth exploring and studying.