Those holding Chison Medical Technologies Co., Ltd. (SHSE:688358) shares would be relieved that the share price has rebounded 25% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. While recent buyers may be laughing, long-term holders might not be as pleased since the recent gain only brings the stock back to where it started a year ago.

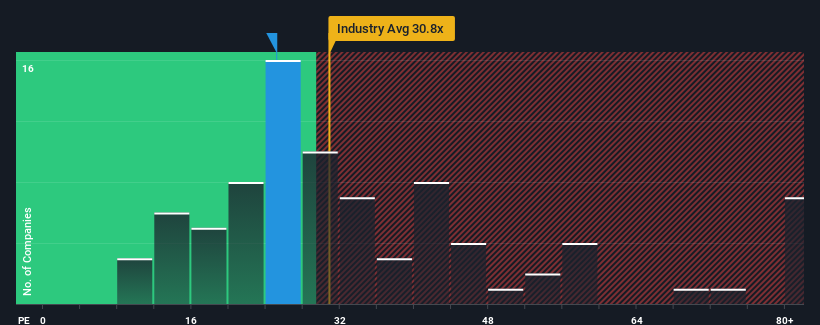

In spite of the firm bounce in price, Chison Medical Technologies may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 25.2x, since almost half of all companies in China have P/E ratios greater than 32x and even P/E's higher than 59x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Chison Medical Technologies has been doing quite well of late. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

SHSE:688358 Price to Earnings Ratio vs Industry March 19th 2024 Want the full picture on analyst estimates for the company? Then our free report on Chison Medical Technologies will help you uncover what's on the horizon.

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Chison Medical Technologies' is when the company's growth is on track to lag the market.

If we review the last year of earnings growth, the company posted a terrific increase of 50%. Pleasingly, EPS has also lifted 55% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the two analysts covering the company suggest earnings should grow by 48% over the next year. That's shaping up to be materially higher than the 40% growth forecast for the broader market.

In light of this, it's peculiar that Chison Medical Technologies' P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

What We Can Learn From Chison Medical Technologies' P/E?

Despite Chison Medical Technologies' shares building up a head of steam, its P/E still lags most other companies. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Chison Medical Technologies' analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Chison Medical Technologies, and understanding should be part of your investment process.

Of course, you might also be able to find a better stock than Chison Medical Technologies. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.