Hangzhou Juheshun New Material Co.,LTD (SHSE:605166) shares have had a really impressive month, gaining 25% after a shaky period beforehand. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 16% in the last twelve months.

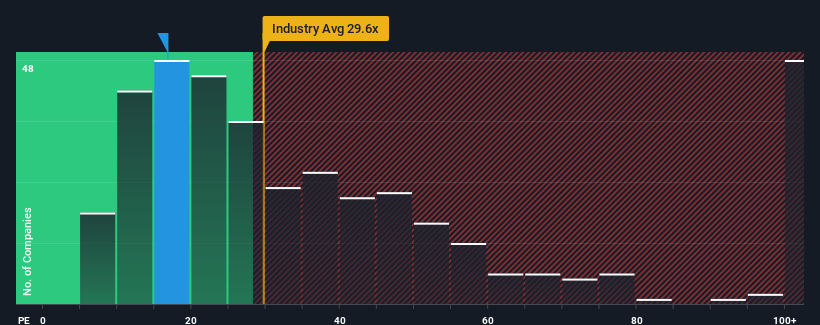

Although its price has surged higher, Hangzhou Juheshun New MaterialLTD may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 16.8x, since almost half of all companies in China have P/E ratios greater than 32x and even P/E's higher than 58x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With earnings that are retreating more than the market's of late, Hangzhou Juheshun New MaterialLTD has been very sluggish. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Does Growth Match The Low P/E?

In order to justify its P/E ratio, Hangzhou Juheshun New MaterialLTD would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a frustrating 23% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 86% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 72% during the coming year according to the dual analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 40%, which is noticeably less attractive.

With this information, we find it odd that Hangzhou Juheshun New MaterialLTD is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Key Takeaway

The latest share price surge wasn't enough to lift Hangzhou Juheshun New MaterialLTD's P/E close to the market median. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Hangzhou Juheshun New MaterialLTD currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Having said that, be aware Hangzhou Juheshun New MaterialLTD is showing 2 warning signs in our investment analysis, and 1 of those is concerning.

If you're unsure about the strength of Hangzhou Juheshun New MaterialLTD's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.