Guangxi Huaxi Nonferrous Metal Co.,Ltd (SHSE:600301) shareholders would be excited to see that the share price has had a great month, posting a 28% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 17% in the last twelve months.

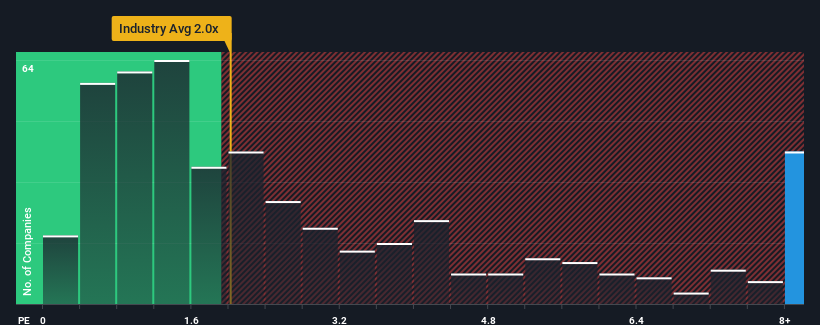

Since its price has surged higher, when almost half of the companies in China's Chemicals industry have price-to-sales ratios (or "P/S") below 2x, you may consider Guangxi Huaxi Nonferrous MetalLtd as a stock not worth researching with its 17.6x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

SHSE:600301 Price to Sales Ratio vs Industry March 15th 2024

What Does Guangxi Huaxi Nonferrous MetalLtd's Recent Performance Look Like?

Guangxi Huaxi Nonferrous MetalLtd hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. Perhaps the market is expecting the poor revenue to reverse, justifying it's current high P/S.. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Guangxi Huaxi Nonferrous MetalLtd's future stacks up against the industry? In that case, our free report is a great place to start.

What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Guangxi Huaxi Nonferrous MetalLtd's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 78%. The last three years don't look nice either as the company has shrunk revenue by 39% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 489% during the coming year according to the one analyst following the company. Meanwhile, the rest of the industry is forecast to only expand by 25%, which is noticeably less attractive.

With this information, we can see why Guangxi Huaxi Nonferrous MetalLtd is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

Guangxi Huaxi Nonferrous MetalLtd's P/S has grown nicely over the last month thanks to a handy boost in the share price. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Guangxi Huaxi Nonferrous MetalLtd's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Guangxi Huaxi Nonferrous MetalLtd you should know about.

If these risks are making you reconsider your opinion on Guangxi Huaxi Nonferrous MetalLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.