Source: Steel Seal of Thought

Introduction:

This article includes:

1. In investing, what is the real “integration of knowledge and action”?

2. Why can't investors always chase the rise and fall?

3. Is it really possible to “not predict, just respond”?

4. Why do people have similar opinions, but their practices are so different?

5. Why can't you “join if you can't beat”?

1. Everyone can know and act in one

According to the previous article, the first half of a round of investment in industrial trends can be divided into three stages:

Stage 1: Earn money with “poor cognition”

Stage 2: Earn money from “poor execution”

Stage 3: Earn money with a “poor system”

At the stage where the market is fully aware, it will be necessary to start making “poor execution” money. This stage is compared to what many people like to call “the integration of knowledge and action.”

Many people think that they clearly saw investment opportunities, understood the investment logic, and made an investment plan. In the end, they fell out of place, hesitated, gave up as soon as they rose, and then summed up — this is a problem caused by “not integrating knowledge and action.”

Therefore, people in the back office often ask me how to integrate knowledge and action.

However, not buying is also an action, and it also corresponds to this perception — a judgment on risk.

Everyone combines knowledge and action at any time. Procrastination is also a combination of knowledge and action. It is a matter of execution of the brain's priority order to “wait and wait”. Even mentally ill people combine knowledge and action; it's just a problem with the perception system.

You feel like you can't combine knowledge and action. The real reason is that sometimes you have two completely opposite perceptions in your mind. After making money, you always forget another false perception. When you feel that your perception is in place, and when you don't make money, you always think of that perception that hasn't been implemented, and you think it's caused by not being able to combine knowledge and action.

The real question is that your inner world has countless “knowledge” corresponding to different “actions”. How should we find the right “integration of knowledge and action”?

This article includes:

1. In investing, what is the real “integration of knowledge and action”?

2. Why can't investors always chase the rise and fall?

3. Is it really possible to “not predict, just respond”?

4. Why do people have similar opinions, but their practices are so different?

5. Why can't you “join if you can't beat”?

two

Build models to handle situations you've never encountered

The integration of knowledge and action is a set of analytical decision-making mechanisms for the human brain:

Receiving Information → Analyzing Information → Predicting → Decision-Making Actions

When you find someone on the street, your brain starts to activate the “integration of knowledge and action” decision-making mechanism:

Cognition: Coming face to face with someone

Analysis: Distance between two people and relative speed

Forecast: Collision will occur in X seconds

Action: Dodge to a side

Every minute, you have to make countless decisions like this, and the same goes for investments. You research at a company:

Perception: Downstream orders are exploding, competitors are discontinuing production and maintenance

Analysis: Downstream inventories will drop to critical levels after two months

Forecast: Prices will rise

Action: Buy

In this process, the most important thing is the analysis and prediction of information.

There is a popular saying in recent years called “don't predict, just respond”, but if you don't predict, what is your basis for responding?

This is actually the case. What experts call “not predicting, just responding” is not really not predicting, but predicting ahead of time — they have grasped the basic probabilities of some common information in advance, and based on these probabilities, they establish a fixed set of decision plans in the brain in advance, and can respond directly when they encounter new information later.

Receiving Information → (Analyzing Information → Predicting) → Decision-Making Actions

So why can't we respond directly to information and act on it, but must establish a model? Because value investment information comes from the real world, the amount of information is limitless, and every situation is different, and it is impossible to respond directly. The role of the model is to process the situation you have seen in the past, generalize and reproduce past money-making experiences and lessons learned from losing money, and then establish a set of stock price prediction methods in the brain to transform the new information into the operation methods you are familiar with.

This process includes:

1. Predict what will happen next based on known information

2. Decide what to do now

The concept of an artificial intelligence “model” is used here. The reason why the big language model can answer content not in the database is that it is essentially a set of predictive mechanisms that can process information that has never been met before and continuously predict the next word. This ability is called generalization ability.

In investing, “training” model data can not only come from experience, but also learn from mature models (such as Buffett). A large part of the reason why many models have appeared in China in a short period of time is that the previous GPT 2.0 model was open source. Major manufacturers can use GPT-4 to mark their models and accelerate evolution. This has also led to a shortage of OpenAI computing power, and domestic IP has been banned.

In the first few years, investors all had to train one or several sets of investment decision models in their brains. If you make money through these models, then these models will stabilize, which is what we usually say has formed a stable investment method, style, and system.

A person may have several “cognitive-decision” investment models at the same time. The brain's movement of these small models has priorities. You feel that it is impossible to combine knowledge and action. It is precisely because of actions corresponding to some of your cognition that the priorities are lower.

Of all the models, the highest level is the one that is repeatedly punched in the face by the market and repeated over and over again — chasing the rise and fall.

III. The model with the highest priority

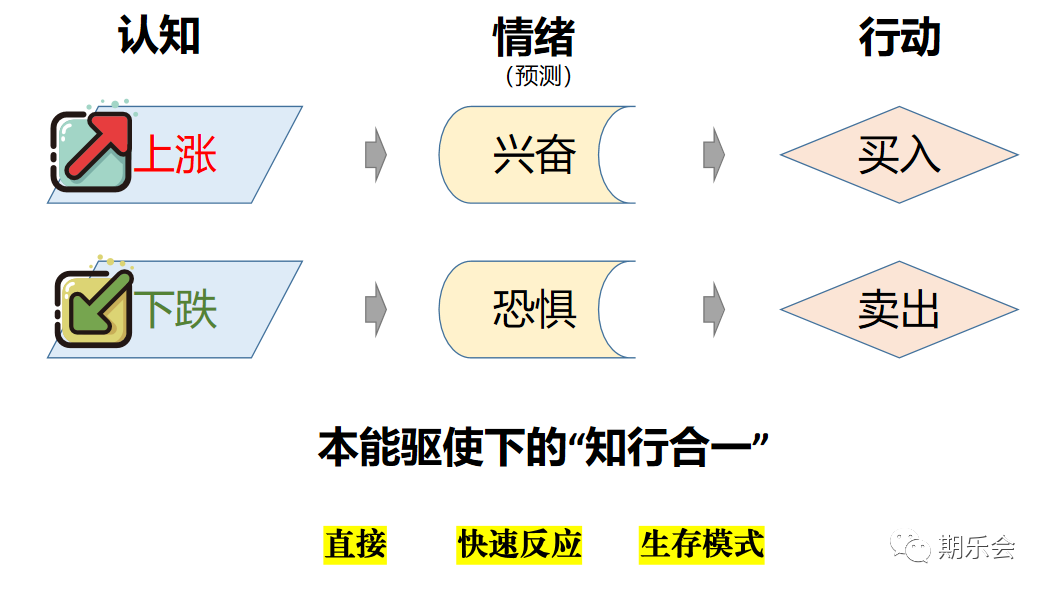

The reason why the act of chasing ups and downs is stubborn is because it is based on the hypothalamus's emotional response rather than the brain's cognitive response. It is an older response model, and therefore has a higher priority. It stems from the two most basic needs of our ancestors — preying on prey and evading natural enemies.

The instinctive response brought about by preying on prey is excitement, and the driving action is attack; the instinctive response to evading natural enemies is fear, and the driving action is to run away. The reason why the two instinctive responses have the highest priority is because opportunities are fleeting, require a quick response, and can't be thought about.

Investors also inherit these two instinctive animal reactions. When stock prices fall rapidly, fear reactions are stimulated and sold on a priority basis; when stock prices rise rapidly, excitement similar to hunting is stimulated and bought on a priority basis.

Speaking of the integration of knowledge and action, this is the most direct integration of knowledge and action.

The act of chasing ups and downs is difficult to get rid of. Even if one person has a high level of investment and a lot of experience, it is only a rise in the response threshold, and they have a good mentality when it comes to fluctuations at a regular level.

Therefore, don't simply say “others are afraid of me being greedy, others are greedy, I'm afraid”. Any human behavior adapts to the environment. If the rise and fall adapts to such a large-scale trend, it is possible to obtain excessive profits when the entire market falls into an environment dominated by emotions.

However, environments suitable for this type of instinctive response are often simple, and the more advanced animals face, the more complex the environment they face. Natural enemies and prey are less clearly distinguished. If misjudgments occur, blind attacks may die, and they may die of exhaustion if they avoid starving themselves.

Similarly, there are very few real trending markets in the stock market. Most of them are volatile markets. If you simply chase the rise and fall, it is likely that you won't even have pants left to lose.

Investors therefore need to use the brain to build more complex “cognitive-action” models.

4. The human brain is a learning model

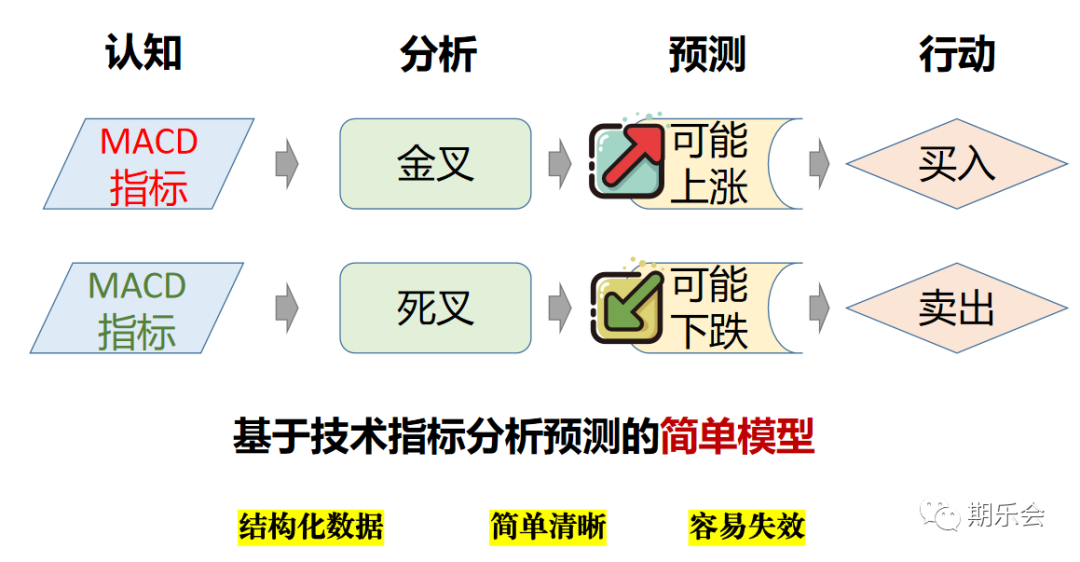

As mentioned earlier, a model includes the four factors of “cognition - analysis - prediction - action”, such as the simplest technical analysis:

Technical analysis is easy to integrate knowledge and action, because it deals with clear numerical information, the listed information is limited, and the correspondence is simple and clear.

However, a model that is too simple and straightforward will fail as soon as there are many people using it. It is necessary to add more technical indicators, more complex relationships and probabilistic judgments, and richer decision-making instructions. Quantitative investment relies on huge computing power to expand optional stocks to the entire market in order to repeatedly reap the leeks of traditional technical analysts.

Although there are more parameters for human brain processing than machines, the computing power ceiling is too low. Before the advent of artificial intelligence, active investment had a better chance of winning or value investment based on fundamental analysis.

The biggest characteristic of fundamental analysis is that most of the key information is qualitative rather than quantitative. This is because the human brain is a learning model. It is not good at calculation; it is better at summarizing rules on its own from past experiences, analyzing, predicting, and making decisions about current situations, and then adjusting this learning model based on feedback.

Returning to the topic of this article, in the face of this round of AI market, since it is an unprecedented new thing, the historical experience of different investment models is very different, and it will give rise to completely different judgments:

If you take the experience of the 2013-2015 mobile internet market, you would think that it is a round of themed industries. There is no need for fundamentals; it can rise if there are themes;

If you learn from the experience of the 2010-2020 wave of new energy industry trends, you will think that the industry trend is still in its early stages. Apart from some computing power targets, there is little value in participating in other targets;

If you extract the historical experience of the 2015-2020 Internet market, you would think that companies with a market value of 100 billion or even trillion dollars, such as ByteDance, Pinduoduo, and Meituan, will emerge from it.

If we take advantage of the 1995-2000 US stock internet revolution, the result would be a complete change in the world and the birth of several great companies...

Different information analysis corresponds to different decisions and operations, and also to different results. Plus changes in the fundamentals themselves, then feed back to the model, make adjustments (relearn the model), then re-output analysis, predictions, and actions, and move on to the next round of feedback...

An investment model is a set of analytical tools in the brain that compresses and decompresses information perception, and predicts and verifies decision-making actions.

What period of history should an experienced investor retrieve depends not on the investment model itself, but on the big model above the investment model — the brain.

5. The impossible triangle of the style model

I've introduced the “impossible triangle of style” in my previous article, that is, any method of investing in stocks must face the trade-off of the three factors of “certainty, prosperity, and valuation”:

“Certainty” is judging the possibility that a company will continue to grow in the future based on dimensions such as “business model, competitive landscape and industry space”;

“Prosperity” is an index for judging the company's current business conditions, including industry supply and demand relationships, increased production capacity or product acceptance, and also major customers or other factors that have caused a sharp increase in current performance, etc.

Certainty and sentiment are both win rate judgments, representing long-term win rate and medium- to short-term win rate, respectively, while “valuation” judges odds, which is a comparison between room for growth and room for decline.

The three elements of “certainty, climate, and valuation” form an impossible triangle of investment. If you give up at least one factor, you form three basic styles:

The so-called investment style is an investment model where your daily usage frequency dominates. It determines — people with a deep pricing style cannot chase the AI sector; people with a rotating industry style don't think too much about the long term and end of AI.

Each of us has our own big model — the brain. The investment model is just a professional vertical model built on top of it. The big model is an innate configuration and adjusted during the growth period, including the most critical parameters — personality and values — leading the same excellent investors to choose different investment models.

Even though a group of outstanding investors agreed on trends in the artificial intelligence industry after discussion, due to the different advantage models in everyone's brain, they read different information and perceptions, and used different historical experiences to obtain different conclusions and perform different actions.

Take these three style models defined by my “impossible investment triangle” as an example:

1. An “industry rotation style” based on prioritizing prosperity, taking into account valuation, and abandoning certainty:

Analysis: Prosperity not only refers to business indicators such as orders, production schedules, and revenue and profit, but also includes indicators such as investment, policies, industry popularity, technology trends, etc., especially in the early stages of investment in industrial trends. Industrial investment intensity is the core sentiment indicator.

Forecast: The AI industry has entered the Age of Discovery. Next, the boom will continue regardless of technological trends, investment intensity, and policy strength.

Action: Find the direction with the strongest industrial prosperity, lay out ahead of time, absorb the dips, and continuously rotate according to valuations.

2. A deep value style based on prioritizing valuation, taking into account certainty, and abandoning prosperity:

Analysis: Due to the blood-drawing effect of the AI sector, many industries experienced negative betas, and many individual stocks were boycotted and lost in value. This is also an opportunity brought about by the AI market.

Forecast: Once the AI market takes a break — there will be a main line adjustment in the fourth quarter of every few years. If the fundamentals of these suppressed sectors remain good, there will be a retaliatory rise.

Action: Keep track of individual stocks you are familiar with. Those that have been undervalued for no reason, slowly depreciate during the decline, and continue to be eliminated to achieve spring planting and fall harvesting.

3. Based on the priority of certainty, the “track layout style” of abandoning valuation, taking into account the degree of prosperity:

Analysis: AI is a major industry trend in the future. This is true, but the targets of early benefits were unclear, or the direction of optical modules that clearly benefited was more cyclical. Therefore, it is still necessary to observe when a real leader with high certainty benefits similar to the Ningde era will emerge.

Forecast: Although the stock may have risen several times when Zhenlong appeared, if you believe this is a major industry trend. Zhenlong, which has risen several times, will rise more steadily in the second half.

Action: Track targets that may benefit from long-term tracking, but do not place positions or only set up observation positions, and buy immediately when their basic quality changes.

Precisely because everyone has a different investment model, it eventually forms an investment market with different styles and you abandon me. There are no right or wrong judgments or decisions. Who can make money depends only on whether they can get approval for more capital.

Although there is a fierce battle for mobility between styles, in the long run, every style can eventually earn money within their style, except for one type of person —

Trust “people who can't beat and join.”

6.

Call the model

Summarize the core ideas of this article:

1. Anyone can combine knowledge and action at any time.

2. The role of the model is to handle situations you have never seen before

3. Chasing ups and downs is a survival pattern, two instinctive animal responses inherited from our ancestors

4. The human brain is a learning model, and the mechanism is “cognition - analysis - prediction - action”

5. Investment style is an investment model with an advantage in your daily use frequency

Humans are bound to be unable to use big model methods to become omniscient and omnipotent investors; they can only use professional investment models that consume less computing power, but in order to cope with complex environments, our brains allow us to build multiple models. The problem caused by this is model calling — when to use what kind of model, which comes back to “cognition.”

It is true that there is a kind of “mismatch between knowledge and action”, which is to rush to achieve results and start acting without real understanding.

The popular saying in the past two years is “join if you can't beat”, but in the end, it's also difficult to make money with this strategy. You don't believe in industry trends or really understand the core logic. It's just because the sector has risen so much that it has inspired a “survival model,” so simply get on the bus first.

Once cognition is inadequate, it is easy for the brain to directly trigger animal instinctive responses. The hypothalamus directly stimulates the “fear model”. If you can't hold it, you cut it off. Then you can't help but chase it three times over. In the end, you won't be able to make any profit.

If you want to integrate knowledge and action, you should give priority to using an “advantage model” that matches one's personality. Either be kind, or rather die — of course, the style that rotates in the A-share sector style can't actually die either.

Editor/jayden