① China People's Insurance revealed the latest premium income. The life insurance business is still shrinking. In the first 2 months, premium income fell 16.8% year on year. ② Life insurance companies are fragmenting? China Life announced a 2.8% year-on-year increase in premium income in the first 2 months of this year, and the growth rate increased to 17.9% in February alone. ③ According to a previous research report by Haitong International, China Life Insurance continues to implement a “strong sales channel project” to further push forward marketing system reforms.

Financial Services Association, March 12 (Reporter Zou Juntao) Life insurance premium income continued to diverge in February?

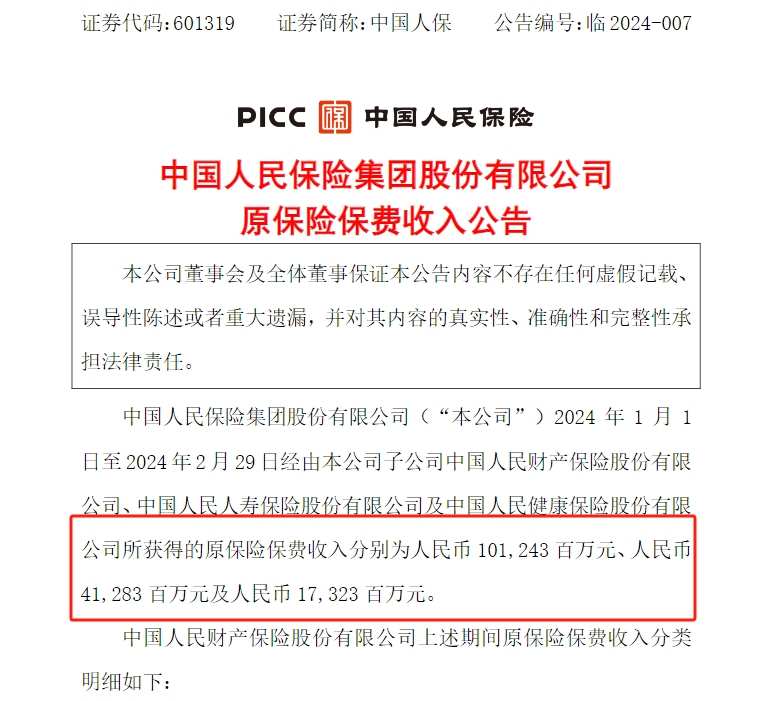

On the evening of March 12, China People's Insurance Company announced the company's latest premium income. In January-February of this year, the original premium income of its People's Insurance Financial Insurance, Human Insurance Life Insurance, and Human Insurance Health Insurance was 101,243 billion yuan, and 17.323 billion yuan respectively. Among them, premium income from the life insurance business continued to decline.

It is worth noting that on the evening of March 11, China Life Insurance issued the original insurance premium income announcement. The company's life insurance business continued to grow at a high rate. The premium income scale in February alone increased 17.9% year-on-year.

Why did life insurance's premium income rise and fall in February again? The reporter learned from industry insiders that there have been no new changes in the industry at present, but the premium income of various insurance companies is highly correlated with the scale of manpower, the status of the main products promoted, and the channel situation.

Life insurance's premium growth rate varied in February. China Life Insurance surged nearly 18% year on year

This evening, China People's Insurance Company disclosed that in January-February of this year, the company's various business subsidiaries recorded original premium income of 101,243 billion yuan; People's Insurance Life Insurance was 41,283 billion yuan, down 16.8% year on year; and People's Insurance Health Insurance was 17.323 billion yuan, up 2.4% year on year.

Judging from the data, among the three major business subsidiaries, life insurance companies are still the most “injured.” In January of this year, People's Insurance Life Insurance recorded original premium income of 32.04 billion yuan, a year-on-year decline of 18.50%, making it the biggest decline in China People's Insurance's business sector. Looking back at the current month, in February of this year, People's Insurance Life Insurance actually recorded an original premium income of only 9.279 billion yuan, a year-on-year decline of 10.36%. This is a slight decrease from the January premium income decline, but it continues to shrink.

It is worth noting that the People's Insurance Financial Insurance and Human Insurance Health Insurance also underwent new changes in February.

According to the split data, People's Insurance actually recorded an original premium income of 38.415 billion yuan in February, a year-on-year growth rate of -1.8% from 2.7% in January of this year; in February, People's Insurance Health Insurance actually recorded an original premium income of 6.125 billion yuan, while the year-on-year growth rate of -4.5% in January was corrected to 18.17%. Overall, in February of this year, human health insurance achieved high growth, but the financial insurance business, which was previously optimistic by the industry, declined.

From an industry perspective, in February of this year, the premium income growth among life insurance companies was still divided.

On the evening of March 11, China Life revealed the company's original insurance premium income. In January-February of this year, China Life recorded a cumulative original premium income of about 252.7 billion yuan, an increase of 2.8% over the previous year. In January of this year, China Life Insurance disclosed that the company recorded cumulative original premium revenue of about 206.6 billion yuan, an increase of 2.2% over the previous year. It is worth noting that the growth rate in February showed signs of increasing.

Looking at the monthly split, China Life Insurance's original premium income in February was about 46.1 billion yuan, an increase of about 7 billion yuan compared with 39.1 billion yuan in the same period last year, and a year-on-year increase of 17.9%.

The implementation of “integration of reporting and banking” has had a profound impact, and the industry is concerned about the new competitive focus of banking insurance channels

It is worth noting that the differentiation in life insurance premium income was already evident in January of this year.

According to statistics from the Finance Association reporter, in January of this year, China People's Insurance, China Life Insurance, China Ping An, China Taibao, and Xinhua Insurance achieved a total premium income of 55.596 billion yuan, a year-on-year decrease of 2.58%. Among the top five listed insurers, only China Life Insurance's life insurance business achieved positive growth.

According to reports, 2023 is a major year of supervision for the life insurance industry, and the regulatory authorities have introduced a number of measures to strengthen industry control, including banking insurance channel reform. According to analysis by industry insiders, the main reason for the general decline in the premium income growth rate of life insurance companies in January of this year was that “good start” activities were limited, and the other was the implementation of “integrated reporting and banking” of banking insurance channels. Among them, the impact of “integration of reporting and banking” is even more profound.

According to the Guotai Junan Securities Report, under the banking insurance “integration of reporting and bank” supervision policy, bank channels showed a phased decline in willingness to sell insurance products; at the same time, some companies have taken the initiative to slow down the development of the logistics business in order to optimize the business structure. Ge Yuxiang, a non-bank finance industry analyst at Dongwu Securities, believes that after the “integration of reporting and banking,” insurance companies re-signed contracts with bank outlets, and banks' enthusiasm for consignment sales was somewhat squeezed.

However, after the implementation of “integrated reporting and banking”, banking insurance channels are still important to insurers. Wang Weiyi's team at Ping An Securities pointed out that in the context of “integration of reporting and banking,” the banking insurance channel industry's fee rate level tends to be consistent, and the focus of competition is shifting from handling fees to partnerships between insurance companies and banks.

The Financial Services Association reporter learned from interviewed industry insiders that from a policy perspective, there are currently no other new changes. The divergence in premium income of life insurance companies may be related to the insurers' own strategies.

On February 20, Haitong International released a research report reviewing China Life Insurance's premium data for January, stating that “a good start in '24 has arrived as scheduled, and I am optimistic about the company's first-mover advantage.” The report points out that China Life Insurance focuses on the “Eight Major Projects” and continues to implement the “Strong Sales Channel Project” to further push forward marketing system reforms, and is expected to maintain steady operation and stabilize its dominant position in the market in the future.

According to reports, at the end of 2022, China Life Insurance launched a new business strategy with layout to lead future development — the “Eight Major Projects”, focusing on innovations and breakthroughs in party building leadership, mechanism optimization, marketing reform, resource integration, management innovation, and ecological drive. China Life Insurance revealed in its 2023 three-quarter report that the company insists on effective teams to drive business development, continues to implement the “Strong Sales Channel Project” around the “Eight Major Projects”, further promotes marketing system reform, strengthens the improvement and training of the sales force, and steadily promotes the transformation of the sales force to specialization and professionalization.