Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that NetScout Systems, Inc. (NASDAQ:NTCT) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

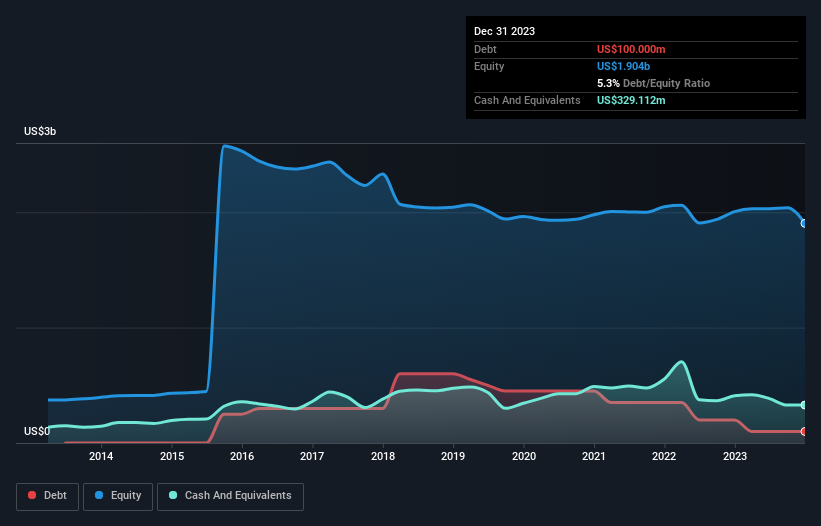

How Much Debt Does NetScout Systems Carry?

As you can see below, NetScout Systems had US$100.0m of debt at December 2023, down from US$200.0m a year prior. However, it does have US$329.1m in cash offsetting this, leading to net cash of US$229.1m.

How Healthy Is NetScout Systems' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that NetScout Systems had liabilities of US$382.3m due within 12 months and liabilities of US$303.6m due beyond that. Offsetting this, it had US$329.1m in cash and US$221.6m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$135.2m.

Since publicly traded NetScout Systems shares are worth a total of US$1.69b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, NetScout Systems also has more cash than debt, so we're pretty confident it can manage its debt safely.

It is just as well that NetScout Systems's load is not too heavy, because its EBIT was down 26% over the last year. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if NetScout Systems can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. NetScout Systems may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, NetScout Systems actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing Up

We could understand if investors are concerned about NetScout Systems's liabilities, but we can be reassured by the fact it has has net cash of US$229.1m. The cherry on top was that in converted 242% of that EBIT to free cash flow, bringing in US$71m. So we don't have any problem with NetScout Systems's use of debt. While NetScout Systems didn't make a statutory profit in the last year, its positive EBIT suggests that profitability might not be far away. Click here to see if its earnings are heading in the right direction, over the medium term.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.