Source: Finance Association

① If you compare various risk events at the macro level to different levels of tsunami warning levels, the “shock wave” that Wall Street is about to face tonight is undoubtedly the most destructive recently... ② Current options market prices show that the implied fluctuation of the S&P 500 index on Tuesday is expected to be as high as 0.9%, higher than the US Federal Reserve interest rate day next Wednesday.

If you compare various risk events at the macro level to different levels of tsunami warning levels, then the “shock wave” that Wall Street is about to face tonight is undoubtedly the most destructive in recent stages...

There are signs that before the release of key CPI data that may affect the Fed's monetary policy trajectory on Tuesday, traders in the US stock options market are becoming more and more anxious — many industry insiders said that the options market is currently worried about tonight's US CPI data causing drastic market fluctuations, even greater than next week's US Federal Reserve interest rate decision.

According to a report by Citigroup, current prices in the options market show that the implied fluctuation of the S&P 500 index is expected to reach 0.9% on Tuesday. This is the largest implied fluctuation estimate since April 2023 before the CPI report was released. This reading is also higher than the implied fluctuation on the day of the Federal Reserve's interest rate meeting next Wednesday.

Citi believes that it makes sense that the market is on thin ice because the Fed's interest rate decision itself will be based in part on the latest CPI data.

In fact, as we mentioned in our preview yesterday, Wall Street will also have a “Super Tuesday” test this week. That is, the US CPI data for February will be released at 20:30 Beijing time tonight. Looking at the time background, the release of this CPI data coincides with the quiet period before the Federal Reserve's March interest rate meeting. The Federal Reserve will lack channels to further interfere with market expectations after the data is released, so the influence of tonight's data is expected to last longer...

Charlie Ripley, senior investment strategist at Allianz Investment Management, said, “The real key to the current market is monthly inflation data.”

So, how will tonight's US CPI data for February actually perform? Where is the market currently most concerned about tonight's data? Let's analyze them one by one from multiple perspectives below...

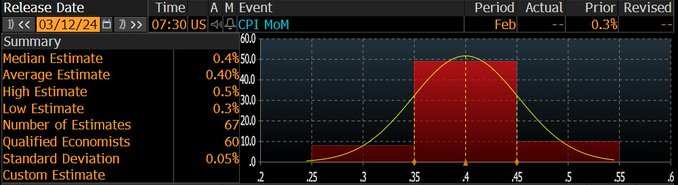

What is the market's estimate for tonight's CPI?

Currently, the last thing many industry insiders want to see in tonight's CPI data is that the CPI data has once again exceeded expectations. Because last month, the expected US CPI fell back to the “2 Era” vision (2.9% compared to the same period), which many people had anticipated, only just fell through. If tonight's CPI data disappoints again, it may reverse the trend of continuing decline in US inflation until now, at least in a phased manner.

Specifically, tonight's overall CPI data is undoubtedly the most likely source of concern — the industry currently generally predicts that the overall US CPI increase in February will rise from 0.3% in January to 0.4%, which will be the biggest increase since September last year. In terms of annual rate, the year-on-year increase in CPI in February is expected to remain at 3.1% for the second consecutive month.

In fact, as shown in the chart below, if we look back at the differences between the actual month-on-month performance of the US CPI and market estimates, it is easy to see that the estimated market value before the CPI data was released was often lower than the actual increase in CPI over the past six months.

The last time the CPI was actually announced was lower than the estimated value month-on-month, and it also dates back to August of last year.

However, considering that the current market estimate for tonight's CPI is as high as 0.4% month-on-month, even if tonight's final announced value is in line with expectations, it's not a very good figure, let alone if the CPI rises higher month-on-month...

Of course, leaving aside the overall CPI performance, the industry still seems to be quite convinced that the decline in core CPI excluding energy and food prices is expected to continue for the time being — the core CPI is expected to rise 0.3% month-on-month in February, slightly lower than the previous value of 0.4%. Core inflation is likely to fall to 3.7% year over year from 3.9% in January, which will be the lowest level since April 2021.

What factors may affect the US CPI performance in February?

In fact, as early as the end of last month, the US PCE price index for January confirmed signs of a rebound in inflation reported in the CPI data for that month, many industry insiders worried that the US CPI increase in February might accelerate again.

The estimates of tonight's CPI data from various agencies using the “New Federal Reserve News Agency” statistics:

What has been mentioned the most is the reason why the CPI data for February may rise again — energy prices. Due to factors such as geopolitics and OPEC production cuts, international oil prices have increased by more than 10% since this year. High oil prices have also boosted the price of refined oil products in the US. According to data from the American Automobile Association, gasoline prices in the US rose by an average of nearly 6% in February.

Although energy prices declined somewhat in early winter, it brought some downward momentum to the overall price trend in the US. However, Wells Fargo estimates that these benefits may be difficult to reap in February. Energy service prices rebounded 4% in February, causing gas station prices to rise.

The National Bank of Canada Wealth Management (NBF) also said that given the rise in gasoline prices in February, the energy segment may have an upward impact on the overall CPI index. Coupled with high housing costs, the overall CPI is expected to reach 0.4% month-on-month, while the year-on-year increase is likely to remain unchanged at 3.1%.

However, in the field of core inflation, it is still expected to be observed whether the benefits can continue to be realized in some areas where the industry is currently more optimistic about cooling. The NBF pointed out that the rise in core prices may slow slightly (0.3% month-on-month increase), partly due to another weak performance in the core commodity sector, which is expected to pull the core CPI increase back to 3.7% year over year — this will be the lowest level in nearly three years.

Société Générale said, “The February CPI report released this week is more likely to show an overall CPI increase of 0.4% month-on-month, mainly due to higher energy prices. Our exact calculation is between 0.3%-0.4% (rounded). If the core data performance is moderate, the market may be willing to ignore the overall increase in prices. Unfortunately, the core CPI rose 0.4% in January, and there is still a reasonable risk that the core CPI for February is as high as 0.3%. Housing rents remain the biggest challenge to falling CPI inflation. We expect landlord equivalent rent (OER) to rise 0.4% in February, following a 0.6% increase in January.”

ANZ stated, “We expect core CPI to rise 0.3% month-on-month in February, and rising energy prices will drive overall CPI up 0.5% month-on-month. Supercore and rent inflation unexpectedly rose in January. Some reversal is expected in February, but seasonal fluctuations in supercore prices continue, which indicates that the reversal may not be significant. Although demand for labor has slowed over the past year, mainly due to an increase in labor supply, there is still a significant net excess demand. Although Fed officials are encouraged by the easing of the inflation rate over the past year, the inflation rate is still too high, and the progress of the different components of inflation is uneven. FOMC officials need to have more confidence that the inflation rate will return to 2% before considering cutting interest rates.”

By contrast, the Canadian Imperial Bank of Commerce's estimates are relatively optimistic.

The bank said, “Is the US about to usher in a second wave of soaring inflation? We don't think so. We expect the consumer price index for February to be 0.3% month-on-month for both the overall and core indices. This assumption is based on the fact that wage and price resets across the economy in January — probably exacerbated by a strong economy and remaining seasonal factors — a process that has already been completed. This means that this month's non-housing services data will turn cold. Housing may remain hot, but commodity prices will remain in a deflationary range. This is not the composition of inflation that Chairman Powell wants, but as the economy booms, the overall level of core inflation will be within a reasonable range, and the Federal Reserve will have time to achieve a more sustainable composition of inflation.”

How is the global market “preparing” for tonight?

As mentioned in our preview yesterday, even though a month has passed, many Wall Street traders still have fresh memories of what happened on the day of the last CPI data release on February 13.

According to data released by the US Department of Labor at the time, the biggest month-on-month increase in core consumer prices in the US in January was the biggest month-on-month, which caused the S&P 500 index to fall 1.4% on the same day — the index's worst CPI release day performance since September 2022. The sharp drop in February also pushed US bond yields to their highest point during the year.

According to a set of industry statistics, although the S&P 500 index fell on only 4 CPI report release days in the past 12 months, the volatility of these trading days has been rising recently — over the past six months, the S&P 500 index has moved at least 0.8% in either direction on the day the CPI was released, which is far higher than less than 0.5% for the statistical period ending in September last year.

This reaction shows that the market is once again becoming more sensitive to inflation reports. Last year, as inflation subsided, the stock market reacted relatively modestly to CPI signals.

Thomas Martin, senior portfolio manager at Globalt Investments, said, “Economic data is beginning to ask more questions rather than answers — that is, how long it will take for the Federal Reserve to gain more confidence in improving inflation. The stock market has had a strong year so far, but are they going too far too fast? It's possible.”

Yong-yu Ma, chief investment officer of Bank of Montreal Wealth Management, said, “The stock market finally got rid of higher-than-expected inflation data (negative) last month, which is impressive. However, if unfavorable data appears for many months, this will test whether the stock market can continue to ignore this, and further question whether the gains so far this year need to be consolidated as soon as possible.”

Bob Schwartz, a senior economist at the Oxford Institute of Economics, also said that the performance of the upcoming CPI and PPI indicators is critical. If the strong rise in CPI in January proves to be no accident, the Federal Reserve's assessment of the policy shift may face new adjustments.

Federal Reserve Chairman Powell testified in Congress last week that the Federal Reserve will not rush to cut interest rates until policy makers are convinced they have contained inflation. Currently, the US economy and labor market are still strong, which means there is room for the Federal Reserve to wait for more clear evidence that inflation is returning to policymakers' 2% target before taking easing action.

edit/ruby