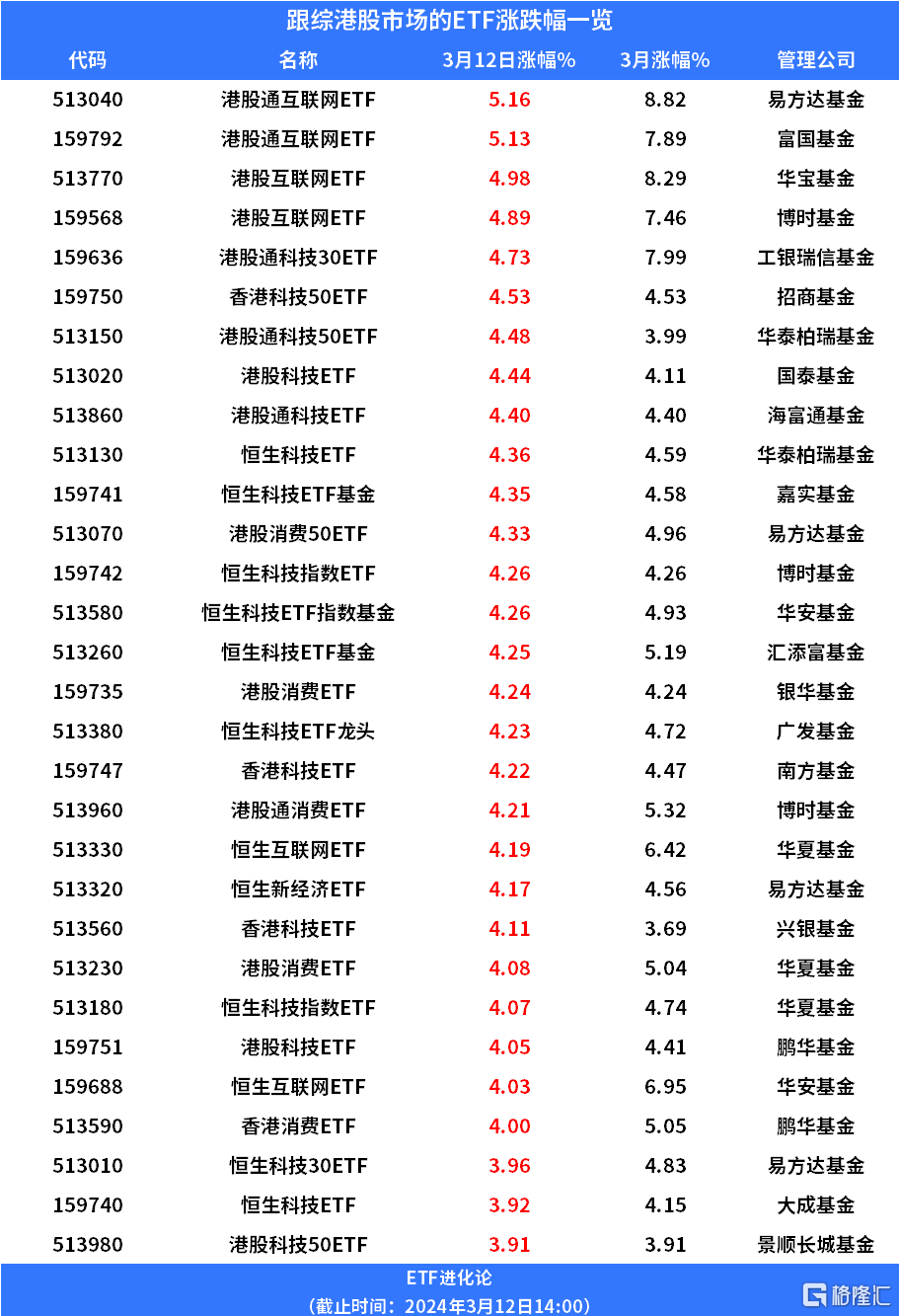

Hong Kong stocks strengthened; Xiaomi Group, Jinshanyun, and Bilibili rose more than 10%; E-Fangda Fund Hong Kong Stock Connect Internet ETF, Huabao Fund Hong Kong Stock Internet ETF, Bosch Fund Hong Kong Stock Internet ETF, ICBC Credit Suisse Fund Hong Kong Stock Connect Technology 30 ETF, and China Merchants Fund Hong Kong Technology 50 ETF rose more than 4.5%.

The Hang Seng Technology Index, Hong Kong Stock Connect Internet Index, and Hong Kong Stock Connect Technology Index all cumulatively increased by more than 20% from their lowest point in early February, entering a technical bull market.

Hong Kong stocks rose. According to the news, Xiaomi Motor announced that the first car, the SU7, will be officially launched on March 28. It will be delivered as soon as it is released, and the volume will increase when it is delivered. 59 stores in 29 cities across the country opened reservations simultaneously.

In terms of capital, as of the close of trading on March 11, southbound capital had achieved net inflows for 18 consecutive trading days, with a total net purchase of 51,124 billion yuan, an increase of 68.38% over the same period last year. Since this year, 34 trading days have seen net inflows of southbound capital, with a total net purchase of 64,155 billion yuan, an increase of nearly 1.22 times over the previous year.

Penghua Fund said that as the performance expectations of Hong Kong stock companies pick up and market liquidity improves, Hong Kong stocks may start a double-click market where performance and valuation are repaired.

According to Tianfeng Securities, expectations for cooling US inflation are getting stronger, and they are optimistic about investment opportunities in the Hong Kong stock market, focusing on the growth value and revaluation opportunities of internet platforms, new consumption, and new power targets, as well as the defensive value of high-quality and high dividend stocks.

Guotai Junan believes that looking ahead, the bottom of Hong Kong stocks is consolidating and fluctuating upward in the medium term, and the dividend style is dominant. As domestic policies to increase economic momentum continue to be introduced, economic growth is expected to stabilize; although the major trend in overseas liquidity is easing, the short-term trend is disrupted by a rebound in US inflation data, overseas liquidity expectations have been repeated, and the growth style of Hong Kong stocks has been further affected. In addition, there are many overseas risk events, including general elections in many parts of the world, geopolitical frictions raging, and expectations that the US recession may heat up and disrupt the Hong Kong stock market. The high-dividend style with low risk characteristics such as undervaluation and stable cash flow is still preferred. It is recommended to focus on dividend assets with low risk characteristics of Hong Kong stocks, such as telecommunications operators, energy, and utilities. Furthermore, the mid-year growth stock market will emerge, and the new energy sector will take the lead, but the market will focus on technological manufacturing.

Huatai Securities pointed out that Hong Kong stocks have recently stabilized and fluctuated within the range, and with marginal changes in short-term overseas interest rate cuts expectations are relatively limited, the pace of Hong Kong stock recovery or the pace corresponding to the introduction of subsequent policies. Allocation-based foreign capital has yet to shift downward. Southbound capital still focuses on the intersection of predictive annual reports+high dividends: from the perspective of annual reports, the bottom of net profit to mother of the Hong Kong Stock Connect 2023FY is already quite solid. According to the Hong Kong Stock Connect 2023FY disclosed sample (disclosure rate is 23%), net profit from the upstream and midstream cycle industry increased and declined year-on-year, but the “reversal of difficult circumstances” such as consumer/utilities showed an improvement in net profit to mother.; From a dividend perspective, the transportation/coal/petroleum/communications dividend ratio is high and relatively stable, combined with annual reports Looking at it intersectionally, the high dividends from transportation and communications and the improvement in net profit to mother are highly predictable.