Source: Wall Street News

S&P fell to a record high. The NASDAQ fell by more than 1%, all of which stopped rising for two weeks, and the Dow fell for two weeks in a row. The chip stock index closed down 4%, and Nvidia closed down 5.5%, the biggest drop in nine months. TSMC's US stock and AMD fell nearly 2%, both falling to historic closing highs. TSMC still rose more than 9% this week, and fell 11% after Mewell Technology's earnings report. Apple closed up 1% to end seven consecutive declines, falling 5% in a week, and Tesla falling 11% throughout the week. China overtook the market, and China's stock index rebounded, but it fell for the first time in the Dragon Year. Station B's earnings report rose 5% the next day, JD rose more than 3%, and the weekly earnings report rose 7.6%. The Pan-European stock index rose for seven weeks, French stocks hit record highs. ASML fell nearly 3%, and Novo Nordisk fell more than 1%, all falling to historic highs.

After the US employment report, the two-year US bond yield fell by more than 10 basis points to a one-month low; the US dollar index hit a new low of more than a month and a half, and the biggest weekly decline in more than two months; and the yen rose by more than 1% in the two-day intraday period, hitting a one-month high. The offshore renminbi rose more than 100 points in the intraday period and broke through 7.19, hitting a new high of more than two weeks.

For the first time in Bitcoin's history, it rose above 70,000 US dollars in intraday and fell back to nearly 4,000 US dollars in half an hour. Crude oil fell more than 1% and declined throughout the week. US oil fell to a low of more than a week for two consecutive years. Gold futures hit a record high for six days, rising nearly 5% this week, the biggest weekly gain in nearly five months. Luntong fell to a high level during the year and still rebounded this week. Lunnickel hit a seven-month high, and Helun Zinc rose more than 4% in a single week.

The non-farm payrolls report shows that the US labor market has cooled down and is still resilient: 275,000 new non-farm payrolls were added in February, 75,000 more than analysts expected, and the total increase in December and January was reduced by 167,000; the unemployment rate did not stabilize in January; instead, the unemployment rate rose to 3.9%, a two-year high; wage growth slowed from January, the year-on-year growth rate remained flat at 4.3%. The year-on-year growth rate was 0.1%, lower than the expected 0.2%.

The commentator said that although employment growth in February exceeded expectations, employment growth declined sharply in the previous two months. Wage growth slowed in February, and the unemployment rate unexpectedly rose. Taken together, it suggests that the Federal Reserve still needs to act prudently, and they may be relieved to start cutting interest rates in the middle of the year. The major employment report released on Friday made traders more betting that the Federal Reserve will cut interest rates in June this year, and interest rate cuts are expected to increase during the year.

This week, the market's expectations for the Fed to cut interest rates this year are heating up. By Friday, the number of interest rate cuts is expected to rise from three a week ago to four

After the employment report was released, swap contract pricing showed that investors almost 100% absorbed the expectations of cutting interest rates by 25 basis points in June, and expected to cut interest rates by about 98 basis points in total this year; US Treasury bond prices first fell in the short term, then jumped rapidly, and the decline in yields accelerated. The yield on two-year US bonds, which are sensitive to interest rates, fell to a one-month low, and dived more than 10 basis points from rising. The yield on US bonds declined or continued to rise throughout the week.

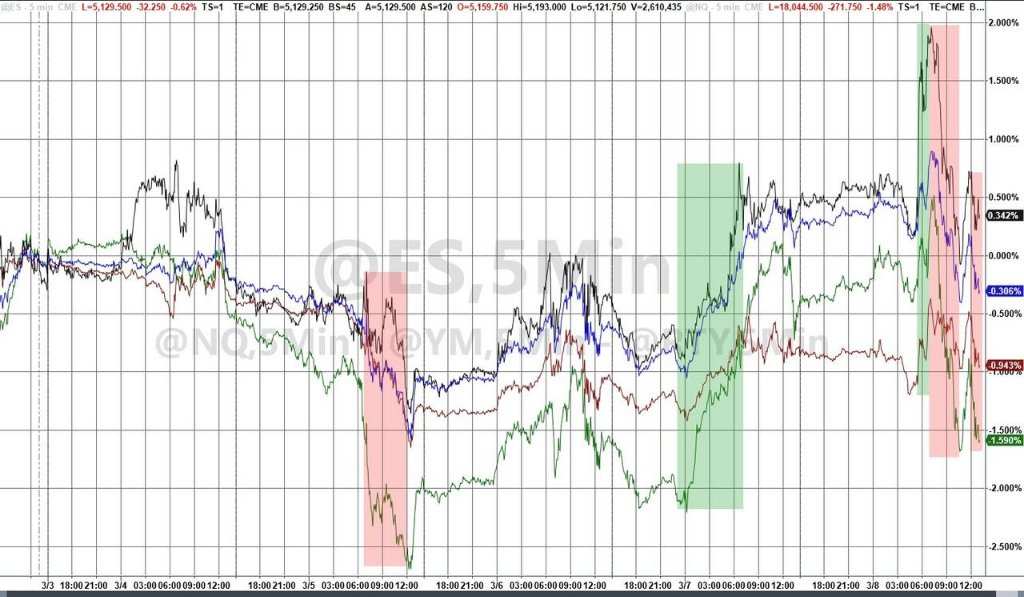

After the employment report, major US stock indexes rose sharply in early trading, and there was an unexpected intraday reversal. S&P fell to a record high. The NASDAQ index fell more than 1% on the second day of this week. Seeing that Tuesday's decline was smoothed out within two days of Powell's testimony, it still dashed hopes that it would continue to rise on the closing day of this week. Chip stocks, which have supported the market for several days, became the culprit behind the fall in US stocks on Friday. Maywell Technology, which led to a sharp double-digit decline, Nvidia evened out the intraday gain of more than 5%, and fell more than 10% from the historical intraday high created by earlier trading. The trend of continuing to hit a record high for more than a week came to an abrupt end. Due to the sharp drop on Friday, chip stocks took back most of their gains in the first four days of this week. Even the record high TSMC US stocks continued to rise sharply this week.

In the foreign exchange market, after the US employment report was released, the US dollar index accelerated its decline and fell to a low level since mid-January. This week, when Powell testified to Congress and repeatedly confirmed that interest rates are expected to be cut this year, the worst weekly performance in more than two months. At a time when the US dollar is weakening, non-US currencies are generally rising. On Thursday, the yen surged to a new high in a month due to revenue data and news such as hawking by central bank officials, etc., with an average intraday increase of more than 1% on both days. Bitcoin experienced a huge intraday shock, first rising by nearly $3,000, breaking the 70,000 US dollar mark for the first time in history. After a flash dive, it fell nearly 4,000 US dollars from its historical high in just over half an hour, then hit 68,000 US dollars, and increased cumulatively in the last 24 hours.

Among commodities, after the release of the US employment report, which strengthened expectations of interest rate cuts, the increase in gold expanded rapidly. New York futures closed at a record high every day for a week, and this week recorded the best weekly performance since the week the conflict between Palestine and Israel escalated in October last year. Apart from market expectations that the Federal Reserve will cut interest rates, the continuing tense geographical situation in the Middle East and Ukraine, and China and many other central banks have repeatedly increased their gold holdings, all driving up the price of gold. Despite the weakening of the US dollar, international crude oil turned down intraday and did not successfully resume gains. Crude oil failed to maintain its upward momentum this week after Saudi Arabia and other OPEC+ countries announced last weekend that they would extend voluntary production cuts until June. The commentator said that the demand side did not provide much support for oil prices, the peak demand season for US cars has yet to arrive, and the Chinese situation needs economic stimulus.

S&P fell to a record high for two weeks, Nvidia recorded the biggest decline in nine months, and Apple ended seven consecutive declines and almost outperformed the market

The opening performance of the three major US stock indexes was mixed, and soon after, they rose sharply. The high-opening S&P 500 Index and the Nasdaq Composite Index rose more than 0.6% and nearly 1.1% respectively in early trading, hitting record highs in the intraday period. The Dow Jones Industrial Average, which opened slightly lower than 15 points, broke out of its decline at the beginning of the session. It rose nearly 180 points and rose nearly 0.5% in early trading. At the end of early trading, the S&P and NASDAQ declined, and the Dow also fell in midday trading, and the NASDAQ decline widened to more than 1%.

In the end, the three major indices fell after two consecutive days of collective gains. The NASDAQ closed down 1.16% to 16085.11 points, but failed to break the all-time high level set last Friday, and fell more than 1% this week after Tuesday. S&P closed down 0.65% to 5123.69 points, falling from a record closing high of around 1% on Thursday. The Dow closed down 68.66 points, or 0.18%. The decline was less than about 1% on Tuesday, to 38722.69 points.

The small-cap stock index Russell 2000, which is dominated by value stocks, closed down about 0.1%. The tech-heavy Nasdaq 100 index closed down 1.53%, failing to continue to approach the highest closing record set last Friday, falling more than 1% on the second day of this week after Tuesday. The Nasdaq Technology Market Capitalization Weighted Index (NDXTMC), which measures the performance of technology components in the NASDAQ 100 index, closed down 2.31%. After rising 2.5% last week, it fell 0.72% this week.

Major stock indexes failed to continue their upward trend this week. S&P fell 0.26%, the NASDAQ fell 1.17%, and the NASDAQ 100 fell 1.55%, all of which stopped rising for two weeks and falling for the third week in ten weeks since the beginning of 2024. Apart from this week, the first week of the new year and the first week of February 16 have also declined since the beginning of the year. The Dow fell by 0.93%, falling for two weeks after five weeks of continuous growth, and falling for the fourth week of this year. Meanwhile, the Russell 2000 had a cumulative increase of 0.55%, rising for two consecutive weeks.

Among the major sectors of the S&P 500, a total of six closed down on Friday. IT, where chip stocks such as Nvidia are located, fell more than 1.8%, other sectors fell less than 0.9%, and healthcare and industry fell less than 0.3%. Google's communications services have come to an end. Real estate that is sensitive to interest rates and is beneficial to interest rate cuts has risen by more than 1.1%, while energy and finance have risen by nearly 0.4% and 0.2%, respectively.

Only three sectors declined this week. Tesla's non-essential consumer goods fell by about 2.6%, Apple's IT fell by nearly 1.1%, and communication services fell by more than 0.6%. Among the eight sectors that have been rising, utilities have risen by more than 3%, energy, materials, and real estate have all risen by more than 1%, and medical care has risen slightly.

Including Microsoft, Apple, Nvidia, Google's parent company Alphabet, Amazon, Facebook's parent company Meta, and Tesla, the seven major technology stocks rose sharply in early trading, and most turned down during the session. Tesla opened high and went low, rising more than 2% at the beginning of the session, falling more than 1.8%. After rebounding on Thursday and closing down on the fourth day of this week, breaking the closing low since May 2023 set on Wednesday, it fell 13.5% this week, smoothing the decline of last week's rebound and falling for the second week in the last six weeks.

Among the six major FAANMG technology stocks, Apple, which fell for seven consecutive trading days and closed at a new low since October 27, 2023, closed 1% higher in midday trading; Alphabet, which turned up higher at the beginning of the session, rose more than 2% in early trading, closed up nearly 0.8% in early trading, rising for 2 days to a week; while Meta, which had been rising for 2 consecutive days to close, rose more than 1% in early morning trading and closed down 1.2% at the end of early trading; Microsoft, which had been rising in early trading, closed down 0.7% in early trading and failed to continue to refresh from January 31, when it fell for 3 consecutive days on Wednesday Low; Amazon, which had risen more than 1% in early trading, closed down 0.8 %; Netflix, which had risen more than 1% in early trading, closed down 0.6%.

Most of these tech stocks fell this week. Apple fell nearly 5%, Microsoft and Netflix fell more than 2%, Alphabet and Amazon fell more than 1%, while Meta surged up about 0.7%.

Chip stocks generally turned down during the intraday period. The Philadelphia Semiconductor Index and semiconductor industry ETF SOXX rose 1% and nearly 1% respectively in early trading, and turned down towards the end of early trading. They both closed down about 4%, falling to closing record highs set for two consecutive days. This week they have climbed nearly 0.6% and 0.7% respectively, far less than last week's 6.8% increase.

Among chip stocks, Nvidia rose 5.1% in early trading and hit a record high at the end of early trading. It fell nearly 6.7% during the low trading day, falling 11.2% from the high set in early trading, closing 5.5%, the biggest closing decline since May 31, 2023. It fell to a record closing high for six consecutive trading days, rising 6.4% this week; it was announced that TSMC US stocks, which had an 11.3% year-on-year increase in February's revenue, rose about 6.2% in early trading and fell nearly 6.2% in early trading for three consecutive days. 2.9%, closing down 1.9%, up 9.3% this week; AMD rose 7.5% to a record high in early trading. At the close, Broadcom fell 2.7%, closing down 1.9%, and both fell 2.3% this week, and TSMC US stocks both fell back after breaking record closing levels for two consecutive days; the first-quarter results guidance fell short of expectations, and Morgan Stanley slashed the target price by 15.5% to $71. Maywell Technology (MRVL) moved low and closed down 11.4%; at the close, Broadcom fell about 7%, Intel fell 4.7%, and Qualcomm fell nearly 3%.

Most AI concept stocks followed the general market and turned down. BigBear.ai (BBAI), which had lower than expected sales and higher losses in the fourth quarter, closed down more than 31.6%; the ultra-micro computer (SMCI), which had risen nearly 6% in early trading, closed down 1.7%; C3.ai (AI), which had risen 7.8% in early trading, turned down 0.2% in midday trading; Palantir (PLTR), which had risen more than 3% in early trading, closed down 1.6%, Adobe (ADBE) closed down nearly 0.8%, while SoundHound.ai (SOUN) held gains throughout the day and closed up more than 4%.

Popular Chinese securities generally rebounded and outperformed the market. The Nasdaq Golden Dragon China Index (HXC) rose 1.3% at the beginning of the session, turned down at the end of early trading and closed up 0.7%. It is expected to close slightly after falling back on Thursday, falling 3.7% this week, falling for the first time since entering the Year of the Dragon. KWEB and CQQQ closed up around 0.2% and 0.4%, respectively. Among individual stocks, Station B, which fell nearly 2% after announcing earnings on Thursday, rose 5%, JD rose more than 3%, and surged 7.6% this week when fourth-quarter revenue was better than expected. Xiaopeng Motor rose nearly 2%, Alibaba rose more than 1%, Baidu and NIO Auto rose about 0.5%, NetEase rose slightly, while Pinduoduo fell nearly 6%, Ideal Auto fell nearly 0.4%, and Tencent Pink fell more than 0.3%.

After US President Joe Biden revealed that he would be instructed to evaluate the federal government's classification of marijuana, saying that no one should be imprisoned for using or possessing marijuana, cannabis concept stocks generally rose. Tilray Brands (TLRY) rose nearly 8% in early trading, Aurora Cannabis (ACB) rose more than 6%, and Canopy Growth (CGC) rose nearly 5%, and closed up 3.7%, respectively.

Among individual stocks with high volatility, pharmaceutical company Amylyx Pharmaceuticals (AMLX) closed down 82.3% after announcing that its amyotrophic lateral sclerosis (ALS) drug failed to reach the target in later trials and that the drug may be withdrawn from the market; after the US Food and Drug Administration's FDA delayed approval of Eli Lilly's Alzheimer's drug, LLY (LLY) fell more than 3% in midday trading, closing down 2.4%, dragging down the medical sector; while the fourth quarter revenue and first-quarter and full-year guidance led to higher than expectations for the first quarter and full year, the IoT company Samsara (IOT) closed up nearly 14%; Apparel retailer Gap (GAP) closed 8.2% after announcing fourth-quarter revenue was higher than expected and its brand Old Navy returned to positive growth for the first time in more than a year; while fourth-quarter profits and first-quarter guidance were higher than expected, the electronic signature company DocuSign (DOCU) closed 4.5%.

In terms of European stocks, the pan-European stock index, which has been rising for two days, has temporarily stopped. The European Stoxx 600 Index closed slightly higher, barely breaking a record closing level for three consecutive days. Most of the major European countries' stock indexes closed down. The German, Italian, and Spanish stock indexes closed at the historic closing levels set on Thursday. After two consecutive gains, three consecutive gains, and six consecutive gains, respectively. British stocks stopped at three consecutive days, but French stock indexes closed at record highs for two consecutive days, rising for three consecutive days.

Among the various sectors, interest-rate sensitive real estate rose by more than 2%, and financial services closed up 1.1%, thanks to Morgan Stanley's rating being upgraded to overrated UBS, which closed 4.1%; while the technology sector fell 1.6%. Among the constituent stocks, ASML, the highest market capitalization chip stock in Europe listed in the Netherlands, closed down 2.7%, leaving the record high created on Thursday. Among other individual stocks, Spanish pharmaceutical company Grifols soared 19.7% after KPMG approved its 2023 results; while German fresh e-commerce HelloFresh, which fell far short of expectations in 2024, fell sharply by 42.1%; after surging more than 8% on Thursday due to improved trial results of new oral weight loss drugs, Novo Nordisk, the highest European market capitalization pharmaceutical company listed in Denmark, closed down 1.6%, falling to the high closing record set on Thursday.

The Stoxx 600 index rose more than 1% this week, rising for the seventh week after a slight increase last week. Most of the stock indexes of various countries have been rising. German stocks have been rising for five weeks, Italian stocks have been rising for six weeks, French stocks and Western stocks, which have been falling back last week, have rebounded. Western stocks, which have continued to rise over the past week, have risen more than 2%, while British stocks have been falling for three weeks. Due to the rise on Friday, the real estate sector surged 2.5% this week, and the financial services sector, which rose more than 2% on Thursday, also surged more than 2%. Despite the fall on Friday, technology still rose nearly 1% this week, while the automotive sector, which had the highest increase last week, fell by about 1%, and tourism fell by more than 1%.

US bond yields once fell by more than 10 basis points in the two years after the employment report to a one-month low

The price of European treasury bonds rose sharply, and yields followed the decline in US bonds in the intraday period. By the end of the bond market, the yield on the UK 10-year benchmark treasury bond was about 3.97%, down about 2 basis points during the day; the yield on 2-year British bonds was about 4.22%, down about 5 basis points during the day; the yield on the benchmark 10-year German treasury bond was about 2.26%, down about 4 basis points during the day; and the yield on 2-year German bonds was about 2.75%, down about 7 basis points during the day.

After the US non-farm payrolls report was released, the yield on the US 10-year benchmark treasury bond quickly rose above 4.12%, then quickly fell to a new high of 4.04%, breaking down to a low level since February 2, falling back by nearly 9 basis points from the daily high, and then rebounded. US stocks had an intraday increase of 4.10%, rising by nearly 2 basis points during the day, then falling back. By the end of the bond market, it was about 4.07%, falling about 1 basis point during the day. The 10-year yield fell by a total of about 11 basis points this week, for three consecutive weeks.

The 10-year US Treasury yield was at a risk of 4.0% on Friday and closed below the 50-day EMA, at the same time low for nearly six weeks

After the US employment report was released, the 2-year US bond yield, which is more sensitive to interest rate prospects, first rose above 4.55% to a new high, then fell rapidly, breaking 4.41%, breaking the low level since February 7, falling by nearly 10 basis points during the day, falling by nearly 15 basis points from the intraday high. US stocks had an increase of 4.50% in midday trading, leveling off most of the declines. By the end of the bond market, it dropped about 3 basis points during the week. The decline was about 6 basis points during the week. After four weeks of continuous rise, it fell by about 16 basis points. Last week at the base point.

US bond yields for various maturities declined collectively this week, with medium-term bond yields leading the decline

The US dollar index hit a new low of more than half a month, Bitcoin rose above 70,000 US dollars for the first time in the intraday period and fell back nearly 4,000 US dollars in half an hour

The ICE dollar index (DXY), which tracks the exchange rate of the dollar against a basket of six major currencies, including the euro, turned up before the European stock market. It rose slightly during the day, rising slightly during the day and maintained a downward trend. The decline widened rapidly after the release of the US non-farm payrolls report, falling below 102.40, breaking the low level since January 15. It fell more than 0.4% during the day, and then fluctuated and rebounded. The US stock market erased most of the losses.

By the close of the US stock market on Friday, the US dollar index was below 102.80, falling nearly 0.1% during the day, falling nearly 1.1% this week; the Bloomberg US Dollar Spot Index, which tracks the exchange rate of the US dollar against ten other currencies, fell by more than 0.1% and continued to break the low level since January 15. This week, the US dollar index all fell for six days, and fell for two weeks after seven weeks of continuous growth. This week was the only week since entering 2024.

Among non-US currencies, the yen rose for three consecutive days. The dollar rose more than 1% in the intraday period after Thursday. The dollar fell below 146.50 against the US yen after the US employment report, breaking the low level since February 2, falling 1.05% during the day; after the US employment report, the US stock market rose above 1.0980 against the US dollar, breaking the high level since January 12, up 0.3% during the day, and the British pound rose above 1.2890 against the US dollar, breaking the high level since the end of July 2023. The euro fell slightly during the day, and the pound maintained its upward trend.

The offshore renminbi (CNH) fell below 7.20 against the US dollar in early Asian trading. European stocks completely broke out of the decline in early trading and picked up after the US employment report. US stocks rose to 7.1848 before the market. After hitting a new high since February 23 on Thursday, they also refreshed their intraday high since February 21, rising 155 points during the day, and continued to decline thereafter. US stocks once again fell below 7.20 in midday trading and fell to a new low of 7.2037. At 5:59 Beijing time on March 9, the offshore renminbi reported 7.2,000 yuan against the US dollar, up 3 points from the end of Thursday in New York. It rose on the fourth day of this week, rising 113 points this week, rebounding after falling back last week. It rose for the third week in the last four weeks, and fell only last week since entering the Year of the Dragon.

Bitcoin (BTC) experienced a huge shock in early trading of the US stock market. It first rose above 70,000 US dollars, breaking the record high of 69,000 US dollars this Tuesday, rising nearly 3,000 US dollars from the level before the US employment report was released, then quickly turned downward. At the end of early trading, US stocks fell below 67,000 US dollars. Some platforms fell below 67,000 US dollars, and fell more than 5% from the highest record set about half an hour ago. Then it quickly returned to 67,000 US dollars and reached 68,000 US dollars in midday trading. Above 10,000 US dollars, in the last 24 hours It has risen by more than 1%, and has risen by more than 9% in the last seven days. The increase is far less than last week's increase of more than 20%.

Crude oil fell more than 1%, falling back throughout the week, and US oil fell to a low of more than a week

International crude oil futures turned down in the middle of the day. When European stocks hit a new daily high before the market, US WTI crude oil hit the $80 mark, rising more than 1.3% during the day, rising above $83.80. Brent crude oil rose nearly 1.1% during the day and continued to decline thereafter. European stocks maintained a downward trend after falling in early trading. After the US employment report was released, most of the decline was recovered, but the pre-market decline in US stocks widened. When US stocks hit a new daily low in early trading, US oil fell below 77.60 US dollars, falling more than 1.7% during the day. The oil price was estimated at 81.70 US dollars, down 1.5% during the day.

In the end, crude oil both fell by more than 1%. WTI crude oil futures for April closed down nearly 1.17% to 78.01 US dollars/barrel, falling for two days, breaking the low since February 26 set on Tuesday; Brent crude oil futures for May, which closed on Thursday, fell more than 1.06% to $82.08 per barrel, and US oil closed higher this week only on Wednesday.

US oil fell 2.4% this week, and oil fell 1.76%. After a rebound last week, it fell for the third week in the last eight weeks. In the 22 weeks since the outbreak of the conflict between Palestine and Israel, crude oil has declined for a total of 12 weeks.

US gasoline and natural gas futures fell sharply. NYMEX's April gasoline futures closed down about 1%, at $2.5272 per gallon, and failed to break out of the low since February 23, which was refreshed on Tuesday. After a rebound last week, falling 3.33% this week and falling for the third week in the last four weeks; NYMEX April natural gas futures fell nearly 0.72% to 1.805 US dollars/million British thermal units, falling for three consecutive days, breaking down 1.63% this week, falling back after four weeks of continuous decline.

Luntong rebounded this week, Lunnickel, Zinc rose more than 4% in a week, and gold futures hit a record high for six days, the biggest weekly gain in nearly five months

Most of London's basic metal futures fell on Friday. Luntong, Lun Aluminum, and Lun Lead, which had risen two times in a row, fell. As soon as it reached 8,600 US dollars on Thursday, it fell to its high level since the end of December last year. Both Lun Aluminum and Lun Lead bid farewell to their one-month high positions. Lunzine, which had been rising for four days and four days to hit a new high in a month, also fell back.

Meanwhile, Renxi rose for 3 days, breaking the high level since August last year on the 2nd, and Lunnickel rose 2 times in a row, continuing to refresh the high level since November last year.

Most of the basic metals rose this week. Lunzine, which led the rise, rose by about 4.6%, and Lunxi nickel, which rose nearly 2%, for four weeks, and Lunxi also rose more than 4% for two weeks. Luntong and Lunn lead, which stopped rising for two weeks last week, rebounded, rising by about 0.9% and more than 3%, respectively, while Lunn Aluminum, which had been rising for two weeks, dropped slightly by 0.2%.

After the US employment report was released, New York gold futures jumped. At one point, the test was 2190 US dollars. Spot gold rose above 2,180 US dollars. For the first time in futures history, the US stock market experienced another wave of gains. For the first time in futures history, it rose more than 1.7% during the day. Spot gold rose above $2,195, rising more than 1.6% during the day, and futures both hit record highs for three consecutive days. US stocks rebounded some of their gains in midday trading.

At the close of maturities, COMEX April gold futures closed up 0.94% to 2195.3 US dollars/ounce, rising for seven consecutive trading days, reaching a record high for six consecutive days. At the close of the US stock market, spot gold was above $2,170, up about 0.8% during the day.

Gold rose 4.75% during the current cycle, the biggest weekly increase since the week of October 13, 2023, and continued to rise for three weeks. In the 22 weeks since the outbreak of the Israeli-Palestinian conflict, futures declined for only six weeks. The biggest decline was in the week of December 8, which fell nearly 3.6%. In that week and the week of February 16, spot gold fell below the $2,000 mark in the intraday period.

Editor/jayden