Beijing Infosec Technologies Co.,Ltd. (SHSE:688201) shareholders are no doubt pleased to see that the share price has bounced 26% in the last month, although it is still struggling to make up recently lost ground. But the last month did very little to improve the 68% share price decline over the last year.

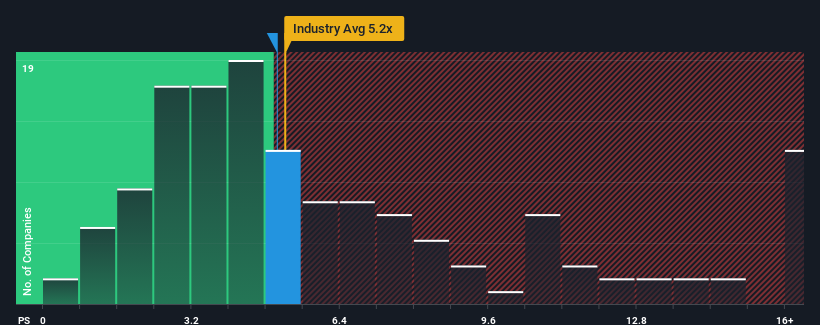

Although its price has surged higher, there still wouldn't be many who think Beijing Infosec TechnologiesLtd's price-to-sales (or "P/S") ratio of 5x is worth a mention when the median P/S in China's Software industry is similar at about 5.2x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

What Does Beijing Infosec TechnologiesLtd's Recent Performance Look Like?

While the industry has experienced revenue growth lately, Beijing Infosec TechnologiesLtd's revenue has gone into reverse gear, which is not great. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Keen to find out how analysts think Beijing Infosec TechnologiesLtd's future stacks up against the industry? In that case, our free report is a great place to start.How Is Beijing Infosec TechnologiesLtd's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Beijing Infosec TechnologiesLtd's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a frustrating 15% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 35% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Looking ahead now, revenue is anticipated to climb by 78% during the coming year according to the two analysts following the company. Meanwhile, the rest of the industry is forecast to only expand by 33%, which is noticeably less attractive.

With this information, we find it interesting that Beijing Infosec TechnologiesLtd is trading at a fairly similar P/S compared to the industry. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

What We Can Learn From Beijing Infosec TechnologiesLtd's P/S?

Its shares have lifted substantially and now Beijing Infosec TechnologiesLtd's P/S is back within range of the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Looking at Beijing Infosec TechnologiesLtd's analyst forecasts revealed that its superior revenue outlook isn't giving the boost to its P/S that we would've expected. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

Before you take the next step, you should know about the 4 warning signs for Beijing Infosec TechnologiesLtd that we have uncovered.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.