近年来,港股市场持续受到外资流出的冲击,恒生指数“跌跌不休”,但以“三桶油”、“三大运营商”、银行股为代表的港股高息股、优质央国企价值股受外资影响趋于钝化,反而凭借低波红利的特征走出独立行情。

近年来,港股市场持续受到外资流出的冲击,恒生指数“跌跌不休”,但以“三桶油”、“三大运营商”、银行股为代表的港股高息股、优质央国企价值股受外资影响趋于钝化,反而凭借低波红利的特征走出独立行情。Since the end of January, Hong Kong stocks have generally continued to rise, but there are still large fluctuations from time to time. Looking at it over a long period of time, as of yesterday's close, the Hang Seng Index had a cumulative decline of 3.57% since this year, and continues to be weaker than the performance of major stock market indices in Europe, America, and emerging markets.

However, there is one type of asset that has emerged from a wave of independent markets under a weak market, namely high dividends+moderately valued assets. Statistics show that individual stocks in industries with high dividend rates in Hong Kong stocks have shown strong performance since this year. For example,$CNOOC (00883.HK)$A cumulative increase of 28.77%,$CHINA COAL (01898.HK)$A cumulative increase of 22.82%,$PETROCHINA (00857.HK)$A cumulative increase of 17.64%,$CHINA SHENHUA (01088.HK)$The cumulative increase was 16.64%.

Zhang Saie, vice chairman of South China Finance, said that the current high interest rate environment continues. Coupled with the Federal Reserve's three or four times stressing that inflation is still not fully controlled, interest rate cuts are not necessarily as fast as expected by the market. In terms of stock selection strategies, arranging some positions on high-yield stocks is a good choice.

High-yield assets from Hong Kong stocks are sought after

In recent years, the Hong Kong stock market has continued to be impacted by outflows of foreign capital. The Hang Seng Index “continues to fall”, but Hong Kong high-yield stocks and high-quality central state-owned enterprise value stocks represented by “three barrels of oil,” “the three major operators,” and bank stocks tend to slow down due to the influence of foreign capital. Instead, they have emerged as independent markets due to the characteristics of low-wave dividends.

In recent years, the Hong Kong stock market has continued to be impacted by outflows of foreign capital. The Hang Seng Index “continues to fall”, but Hong Kong high-yield stocks and high-quality central state-owned enterprise value stocks represented by “three barrels of oil,” “the three major operators,” and bank stocks tend to slow down due to the influence of foreign capital. Instead, they have emerged as independent markets due to the characteristics of low-wave dividends.

According to the data, as of the close of trading on March 6, the cumulative increase of CNOOC has reached 28.77% since this year, and the cumulative increase of CNPC shares is 17.64%.$SINOPEC CORP (00386.HK)$The cumulative increase was 6.85%.$CHINA UNICOM (00762.HK)$The cumulative increase was 15.92%,$CHINA TELECOM (00728.HK)$The cumulative increase was 8.82%,$CHINA MOBILE (00941.HK)$The cumulative increase was 5.02%.$CITIC BANK (00998.HK)$A cumulative increase of 13.59%,$ABC (01288.HK)$The cumulative increase was 7.64%,$BANKCOMM (03328.HK)$A cumulative increase of 6.98%,$ICBC (01398.HK)$The cumulative increase was 5.5%.

Many investors told reporters, “Currently investing in Hong Kong stocks is equivalent to finding sugar to eat in glass scraps. We should focus on high-yield stocks, which are currently popular. Otherwise, the capital may be bought in US dollar bonds or fixed deposit in US dollars. The interest rate is also around 4%. In the current environment, the word 'stable' takes the lead.”

As stated, China's risk-free return falls below 3%, and high-quality assets with “low-wave dividends” are relatively scarce. As a result, high-quality central state-owned enterprise value stocks with dividend rates of 8% or higher in the Hong Kong stock market are favored by domestic investors. From the perspective of dividend rates and treasury bond spreads, as of March 6, the Hang Seng High Dividend Index had a dividend rate of 7.85%, and the spread with the 10-year treasury bond yield widened to 5.45 percentage points, which is in a historically high position.

In addition to high-quality central state-owned enterprise targets, another important component of the Hong Kong stock market pool of high-interest shares is local Hong Kong stocks, such as high-quality high-yield stock companies in the fields of local utilities, finance, real estate, and integrated industries in Hong Kong.

Take Hong Kong-funded housing enterprises as an example. From 2015 to 2022 (note: the 2023 data is incomplete, so there are no statistics), the dividends per share showed a steady upward trend. Most companies had a compound dividend growth rate of more than 3% per share from 2015 to 2022; some local Hong Kong stocks promised a high, stable dividend ratio or dividends with sustainable and steady growth. Furthermore, in 2022, the dividend ratio of some representative companies in Hong Kong's local finance, utilities, and integrated industries remained high, and the dividend per share basically returned to the level of 2019.

Zhang Yidong, chief strategist at Societe Generale Securities, said that with the Federal Reserve's interest rate hike in early 2022 and the rise in interest rates on US ten-year treasury bonds, the Hong Kong market's Hibor interest rate rose rapidly, and the spread with Hong Kong's local high-yield stocks continued to narrow, once exceeding the dividend rate of local high-yield stocks. Since October 2023, as expectations of the Federal Reserve's interest rate cuts continue to heat up, Hibor interest rates decline, and the spread between the dividend rate of Hong Kong's local high-yield stocks and the Hibor interest rate widens again, it is expected that local high-yield stocks in Hong Kong will once again be favored by investors.

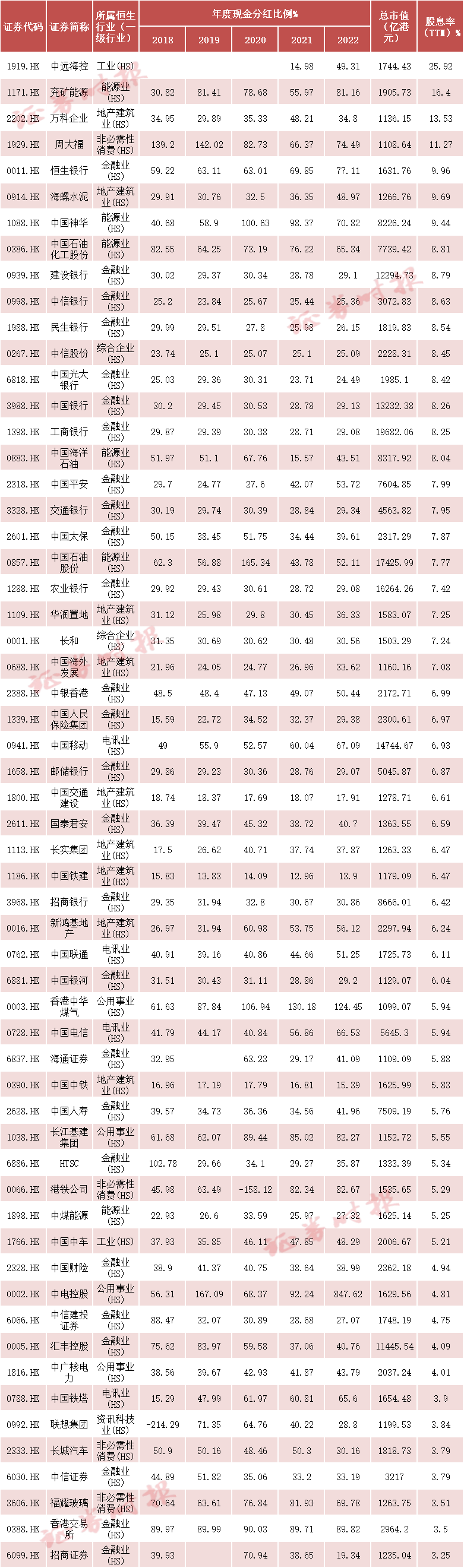

According to the reporter's statistics, there are currently 59 individual stocks in the top 100 Hong Kong stocks by total market capitalization, accounting for 59%, and 17 with dividend rates above 8%. Most of the high-yield stocks are concentrated in finance, energy, real estate, and utilities.

List of the top 100 individual stocks with a dividend rate of 3% or more in total market capitalization

Southbound capital gradually replaced foreign investors to obtain pricing rights for high-interest shares in Hong Kong stocks

In recent years, allocation-type Chinese investors have faced an “asset shortage” to a certain extent. In particular, mainland public fund companies' fixed income departments, insurance, bank financial management and other institutions have strong demand for allocating high-quality and effective assets, and high-quality Hong Kong stocks with high dividends are attractive for long-term allocation.

In 2023, Southbound Capital's net purchase of Hong Kong stocks was approximately RMB 289.5 billion. Among the top ten net inflows of southbound capital according to the previous top ten active individual stocks, low-wave dividend assets occupied 4 seats, namely China Mobile, CNOOC, China Telecom, and China Shenhua. Southbound Capital gradually obtained pricing rights for low-wave dividends in Hong Kong stocks. Compared to the beginning of 2023, Hong Kong Stock Connect's shareholding ratio of Hong Kong stock low-wave dividend assets represented by telecom operators, banks, and energy increased in early 2024.

Taking central state-owned enterprise stocks as an example among high-yield stocks, Wind data shows that in recent years, its share of Hong Kong Stock Connect shares has been rising year by year, from 5.3% at the end of 2018 to 13.5% on February 21, 2024, while the share of international intermediary holdings measured foreign holdings has declined markedly, from 26% at the end of 2018 to 16.6%.

If the scope is extended to the entire Hong Kong Stock Exchange, it can also be seen that the Hong Kong Stock Connect shareholding ratio continues to rise, from 8.8% in 2020 to 14.8% at the end of February 2024, while the foreign shareholding ratio continues to decline, falling from 43.4% in 2020 to 36.7% at the end of February this year.

Zhang Yidong said that in the medium to long term, assets that can provide stable high dividends are invaluable in a relatively complex domestic and foreign environment. High-yield assets are one of the important investment strategies for allocating China's equity assets in the future. Investors are advised to allocate leading central state-owned enterprises in the fields of energy (oil, coal), telecom operators, utilities, finance, highways, etc. based on a long-term, strict “low-wave dividend, convertible bond-like” strategy, as well as high-quality high-yield stock companies in Hong Kong's local utilities, finance, real estate, and integrated industries.