Those holding Wuxi ETEK Microelectronics Co.,Ltd. (SHSE:688601) shares would be relieved that the share price has rebounded 36% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Unfortunately, despite the strong performance over the last month, the full year gain of 3.5% isn't as attractive.

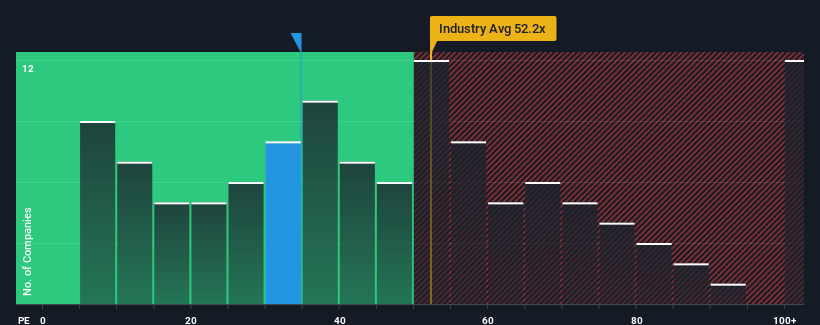

After such a large jump in price, given around half the companies in China have price-to-earnings ratios (or "P/E's") below 28x, you may consider Wuxi ETEK MicroelectronicsLtd as a stock to potentially avoid with its 34.7x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Wuxi ETEK MicroelectronicsLtd certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

How Is Wuxi ETEK MicroelectronicsLtd's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as high as Wuxi ETEK MicroelectronicsLtd's is when the company's growth is on track to outshine the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 37% last year. The strong recent performance means it was also able to grow EPS by 124% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 41% during the coming year according to the two analysts following the company. Meanwhile, the rest of the market is forecast to expand by 41%, which is not materially different.

With this information, we find it interesting that Wuxi ETEK MicroelectronicsLtd is trading at a high P/E compared to the market. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

The Key Takeaway

Wuxi ETEK MicroelectronicsLtd's P/E is getting right up there since its shares have risen strongly. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Wuxi ETEK MicroelectronicsLtd's analyst forecasts revealed that its market-matching earnings outlook isn't impacting its high P/E as much as we would have predicted. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Wuxi ETEK MicroelectronicsLtd, and understanding should be part of your investment process.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.