The NASDAQ rose more than 1%, and the Dow bid farewell to this month's low. Among the seven major technology stocks, Apple fell alone, and Nvidia rose nearly 2.5% to a record high on the second day of this week; SMCI, the AI concept “monster stock,” rose 11% to a record high for 8 consecutive days; and Lyft rose 35% after the earnings report. China's stock index rose more than 3%, Bitcoin mining giant Jianan Technology rose more than 20%, NIO and Xiaopeng Motors rose more than 5%, and JD and B stations rose more than 4%.

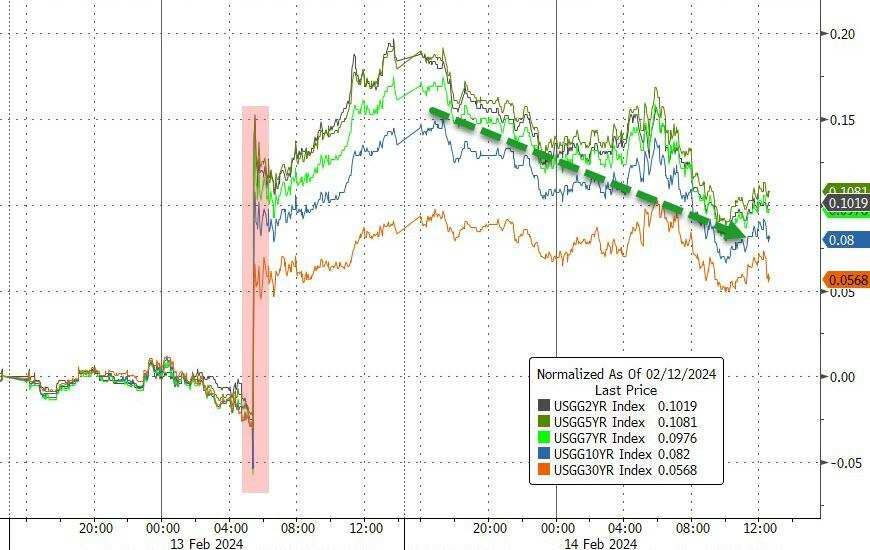

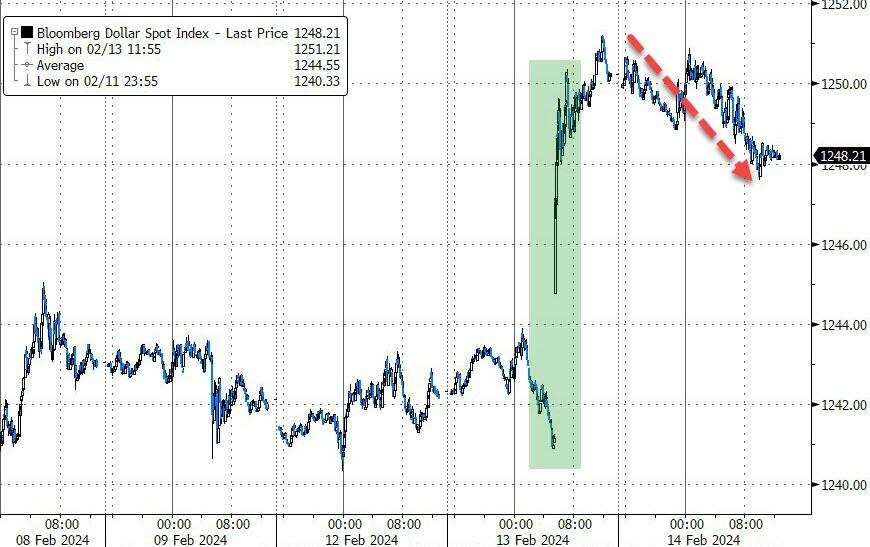

The UK CPI unexpectedly did not accelerate growth, and the two-year British bond yield fell by more than 10 basis points. The two-year US Treasury yield once fell more than 10 basis points from the February high. The US dollar index fell after hitting a three-month high; the yen temporarily withdrew from a three-month low but did not recover 150; the offshore renminbi recovered 7.23 after hitting a new low of nearly three months, rising more than 100 points at one point.

Bitcoin rallied more than $3,000 in the intraday period and hit a new high of more than two years. The market capitalization surpassed $1 trillion for the first time in more than two years. US oil rose more than 1% in the intraday market and then turned down, ending seven consecutive gains and falling to a high of more than two weeks; US natural gas hit a new low for more than three years on the 6th, falling nearly 6% in the intraday period. Gold fell five times in a row, closing at a two-month low. Lunxi stopped at six consecutive days; Luntong fell to a low level of nearly three months; Lunxi and nickel rose to a two-week high for three consecutive years.

The US CPI announced on Tuesday unexpectedly showed signs of a recovery in inflation, which seriously dampened the market's expectations of interest rate cuts. The amount of interest rate cut by the Federal Reserve this year, which is fully reflected in current market pricing, is about three times, in line with the expected number of interest rate cuts announced by the Federal Reserve in December last year. Traders also expect a 70% chance of cutting interest rates for the fourth time during the year, but the overall expected decline is far below the level of a month ago. At the time, swap contract prices showed that investors expected to cut interest rates as much as seven times this year.

After market interest rate cut expectations were adjusted, there was a rebound in the US stock market, which plummeted on the day the CPI was released. According to some commentators, the rebound in US equity bonds on Wednesday stemmed from bottom buyers entering the market after Wednesday's fall. Technology stocks have once again taken on the heavy responsibility of boosting the market, and chip stocks have rebounded strongly. Nvidia is approaching an all-time high in intraday history, hitting a record high for the second time this week. The AI concept “monster stock” ultra-microcomputer (SMCI), which rose against the market on Tuesday, accelerated its rise and continued to reach record highs. Following the good start of Hong Kong stocks in the Dragon Year, China Securities outperformed the market on the second day of this week after Monday.

In terms of the bond market, the UK CPI did not grow slightly faster year on year as analysts expected. Instead, it stabilized the growth rate of 4% in December. Prices of European bonds, led by British treasury bonds, rebounded and yields fell. The yield on two-year British bonds, which are sensitive to interest rates, fell sharply by more than 10 basis points. US bond yields, which soared after the CPI was announced, also fell. The benchmark 10-year US Treasury yield fell below 4.30%, breaking away from a two-month low. The two-year US Treasury yield once fell more than 10 basis points from the high level set over the past few days since the Federal Reserve meeting in December last year.

In the foreign exchange market, the US dollar index, which jumped after the CPI was announced on Tuesday, consolidated and fell after hitting a new high in three months over the past few days. According to some analysts, given the resilience of the US economy, future statements by Federal Reserve officials may boost the US dollar. There may still be some room for the dollar to rise before the end of the first quarter of this year. The yen rebounded below 150.00 against the US dollar on Tuesday, but failed to recover 150. Foreign exchange strategists believe that 152 is the key position that may trigger the Japanese government to interfere in the foreign exchange market next.

Cryptocurrency regained gains at a time when risk-asset US stocks rebounded. Bitcoin rallied more than $3,000 in the intraday market. After reaching the $50,000 mark for the first time in more than two years on Monday, it sprinted towards the $52,000 mark. Bitcoin's market capitalization surpassed $1 trillion on Wednesday for the first time since late 2021, according to CoinMarketCap data.

Among commodities, the fall in US dollar and US bond yields failed to support gold's rebound. Spot gold, which fell below $2,000 after the CPI was announced on Tuesday, continued to hover below this key level, hitting a new low in February. Futures gold also hit a two-month low, continuing to test the $2,000 mark. The commentator said that it is difficult for the price of gold to rebound after falling below $2,000, because some of the drivers that previously broke through $2,000 were expectations that the Federal Reserve would cut interest rates faster. If it is further confirmed that the Federal Reserve is unlikely to cut interest rates soon, it may be a catalyst for a further decline in gold prices.

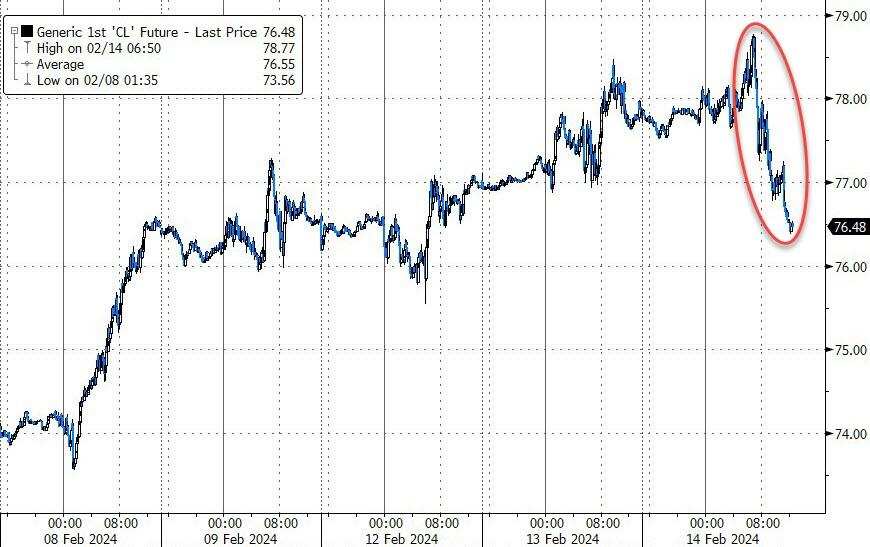

The US Department of Energy announced that US EIA crude oil inventories increased by more than 12 million barrels last week, far exceeding expectations. The international crude oil market stopped rising and falling, and US oil failed to maintain its continuous upward trend for more than a week. After rising more than 1% in the intraday period, it once fell close to 2%, falling to a high level for more than two weeks. Some commentators believe that the increase in crude oil inventories is due to a decline in refining, and the crude oil production and capacity utilization rate of US refineries all hit new lows since December 2022. Furthermore, the chairman of the US House Intelligence Committee issued a statement saying that information on a serious national security threat was provided to Congress without disclosing details. The media claimed that the threat was related to Russia. This is seen as news that attacks some investors in the oil market.

The NASDAQ rose more than 1%, and after Nvidia closed to a record high, Lyft soared, Bitcoin concept stocks surged, China's stock index rose more than 3%

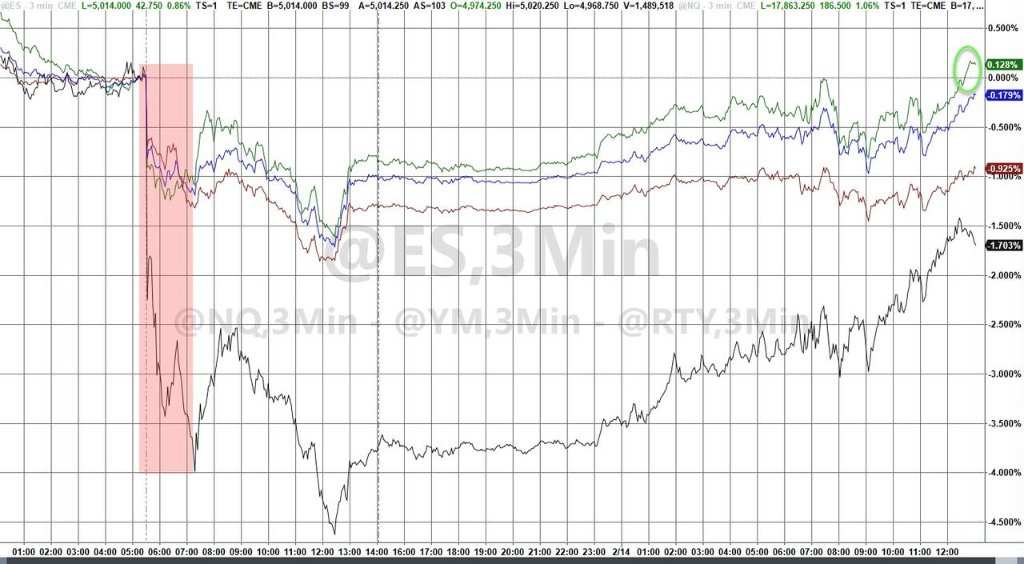

The three major US stock indexes collectively opened higher. The intraday gains declined somewhat, and reached new highs at the end of the session. The Dow Jones Industrial Average rose nearly 150 points in early trading and fell slightly in midday trading. It fell nearly 80 points at a new low, increased after turning higher in midday trading, and rose nearly 170 points on the late day. The S&P 500 index and the Nasdaq Composite Index did not turn down throughout the day. At the end of the session, S&P rose about 1%, and the NASDAQ rose more than 1.3%. In the end, the three major indices closed higher, and none of them offset Tuesday's decline. The S&P and NASDAQ stopped falling for two days, both recording the biggest gains since the publication of the non-agricultural report on February 2, and the Dow, which fell back on Tuesday, recorded the biggest increase since February 1.

S&P closed down nearly 1.4% on Tuesday, the biggest drop on the CPI release date since September 2022, up 0.96% to 5000.62 points. The NASDAQ index, which closed down 1.8% on Tuesday, the biggest drop since January 31, closed up 1.3% to 15859.15 points, breaking away from the new low since February 6 and February 5, respectively. The Dow Index, which recorded its biggest decline since March 9 last year, closed up 151.52 points, or 0.4%, to 38424.27 points, and rebounded after falling nearly 1.4% on Tuesday to a low level since January 31.

The tech-heavy Nasdaq 100 Index closed up 1.18%, rebounding after falling for two consecutive days and closing low since February 6. The Nasdaq Technology Market Capitalization Weighted Index (NDXTMC), which measures the performance of technology components in the NASDAQ 100 index, closed up 1.47% and continued to fall from the historic closing high that was refreshed last Friday. The small-cap stock index Russell 2000, which is mainly value stocks, closed up 2.44%, outperforming the market, and rebounded after falling nearly 4% on Tuesday to the biggest decline since June 2020.

Among the major sectors of the S&P 500, energy and essential consumer goods, which fell nearly 0.2%, closed down on Wednesday. The industry led the rise by nearly 1.7%, Meta's communications services rose more than 1.4%, IT, where chip stocks are located, rose 1.1%, and finance rose nearly 1%. Among the constituent stocks of the Dow, cloud computing giant Saifushi led the rise by nearly 2.9%. Intel ranked second in terms of gains. Caterpillar, Cisco, and Nike rose more than 1%, and J.P. Morgan rose 1%.

Most of the leading technology stocks rebounded, including Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta, and Tesla. Of the seven major technology stocks, only Apple closed down. Among them, Tesla, which raised the price of the US Model 3 long battery life version to 47,490 US dollars, turned down in the short term, and closed up nearly 2.6%, stopping two consecutive declines, leaving the closing low since February 5, when it fell more than 2% on Tuesday.

Among FAANMG's six major technology stocks, Netflix, which fell two days in a row to close at a low price since January 24, closed up 4.5%, breaking the high since December 2021; Facebook's parent company Meta, which fell twice in a row, closed up nearly 2.9%, approaching the historic closing level set on February 2; after founder Bezos reduced its holdings for the second time in a week and revealed a sell-off of 2.1 billion US dollars, Amazon closed up 1.4%, breaking away from the closing position since February 1, which was refreshed for two days; Microsoft closed up nearly 1%; its autonomous driving company Waymo announced its first recall of driverless car software After that, Google's parent company Alphabet closed up 0.5%, and Microsoft both rebounded after falling for two consecutive days to a low level since February 6; while the Apple market initially turned down, it closed down nearly 0.5%, falling continuously from the 3rd to January 17.

Chip stocks generally rebounded after two consecutive days of decline. The Philadelphia Semiconductor Index and semiconductor industry ETF SOXX closed up nearly 2.2% and 2.3%, respectively, outperforming the market. The former was close to the historical closing high set last Friday, while the latter refreshed the historical closing high set last Friday. After establishing the AI-RAN Alliance, a new industry association with SoftBank and standardizing technology that uses mobile communication base stations to distribute artificial intelligence processing globally, Nvidia closed up nearly 2.5%, with a market capitalization of about 1.83 trillion US dollars, surpassing Google's parent company with a market capitalization of about 1.82 trillion US dollars, breaking the closing record high set on Monday; Arm, which fell sharply by nearly 20% on Tuesday, rose more than 10% and closed up nearly 5.4% in early trading. 4%, Intel, Qualcomm rose more than 2%.

AI concept stocks generally followed the upward trend in the general market. At the close, the ultra-micro computer (SMCI), which rose more than 2% on Tuesday, closed up nearly 11.3%, rising for eight consecutive trading days, and hitting a record closing high for 8 days; BigBear.ai (BBAI) rose more than 6%, Palantir (PLTR) rose nearly 5%, C3.ai (AI) rose 1.7%, Adobe (ADBE) rose nearly 0.5%, and SoundHound.AI (SOUN) fell nearly 0.9%.

Popular Chinese securities generally rebounded. The Nasdaq Golden Dragon China Index (HXC), which fell 2.7% on Tuesday, closed up nearly 3.5%, outperforming the market on the second day of this week, breaking the closing high since January 12, set by a rise of more than 2% on Monday. KWEB and CQQQ closed up 3.6% and 1.9%, respectively. The two Bitcoin mining giants followed Bitcoin's sharp rise. Jianan Technology closed up 31.8%, and Yibang International rose 25.3%. Among other individual stocks, by the close, Dada rose nearly 7%, Xiaopeng Auto and NIO Auto rose more than 5%, JD and B stations rose more than 4%, New Oriental and iQiyi rose more than 3%, NetEase rose nearly 3%, Alibaba, Baidu, and Pinduoduo rose more than 2%, Tencent Fanshi rose more than 1%, and Ideal Auto rose 1%.

Among regional banks, New York Community Bank (NYCB), which fell more than 6% on Tuesday, rose nearly 1.1%, Zions Bancorporation (ZION) rose 3.8%, Keycorp (KEY) rose more than 2%, and Alliance Western Bank (WAL) rose 1.7%.

Among the individual stocks that announced financial reports, ride-hailing giant Lyft (LYFT) closed 35.1% after announcing fourth-quarter results that were better than expected and that the adjusted EBITDA profit margin for the 2024 fiscal year would increase by 50 basis points rather than the 500 basis points disclosed when the financial report was released; after announcing the company's first stock repurchase plan and proposed repurchase of up to 7 billion US dollars, Lyft's rival Uber (UBER) closed 14.7%; the medical technology stock IQVIA Holdings (IQV), which had higher revenue and adjusted earnings for the fourth quarter than expected, closed up 13.1 %; the influencer trading platform RobinHood (HOOD), which unexpectedly recorded EPS profits in the fourth quarter, closed up 13%; the pharmaceutical company Charles River Laboratories (CRL), which had higher than expectations in the fourth quarter, closed up 11.3%; while the gaming and entertainment stock MGM (MGM), which had better business than expected in Macau in the fourth quarter but whose US business was affected by the Detroit strike and labor costs, closed down 6.3%; food giant KHC (KHC), whose revenue in the fourth quarter was lower than expected, closed down nearly 6.3%; 5.5%; Airbnb (ABNB) fell more than 5% in early trading and closed down 1.7% after announcing that the loss per share for the fourth quarter was lower than expected, but warned that the increase in the number of nights booked in the first quarter was under pressure.

Among other highly volatile individual stocks, many cryptocurrency concept stocks bounced back. Iris Energy (IREN) closed up nearly 20%, Coinbase (COIN), Marathon Digital (MARA), and Riot Platforms (RIOT) rose more than 14%, and MicroStrategy (MSTR) closed more than 12%.

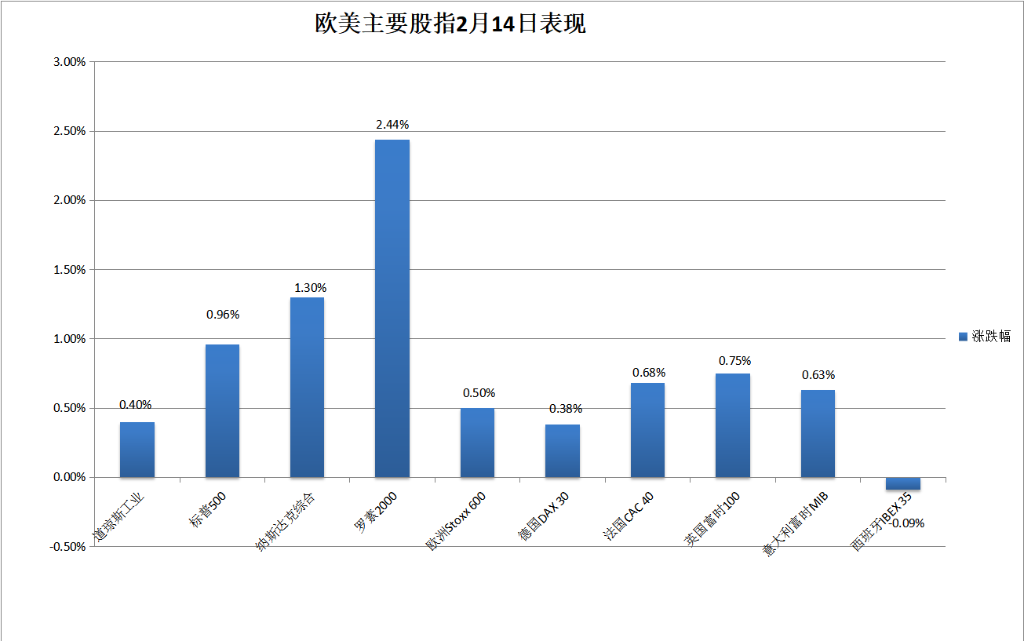

In terms of European stocks, the UK CPI growth did not pick up. Market expectations for the Bank of England's interest rate cut have picked up. Coupled with the positive performance of some companies, the Pan-European stock index rebounded and closed higher on the second day of this week. The European Stoxx 600 Index bid farewell to its closing low since January 25, which was refreshed on Tuesday, and evened out about half of the sharp decline of nearly 1% on Tuesday. Most of the major European countries' stock indexes rose. The German, French and British stocks, which fell back on Tuesday, and the Italian stock index, which stopped rising for three consecutive days, rebounded. British stocks led the rise, while the Spanish stock index closed down slightly and fell for two consecutive days.

Among the various sectors, technology, which fell 2.7% on Tuesday and led the decline, closed up nearly 1%. Among the constituent stocks, Europe's highest market capitalization chip stock, which fell more than 3% on Tuesday, and ASML, which rose more than 0.3% on Tuesday, are still far from the historical closing high set on Monday. The medical sector rose more than 0.8%. Among the constituent stocks, Novo Nordisk, the highest European market capitalization pharmaceutical company listed in Denmark, closed more than 1.7%, reaching a record high for two consecutive days, supporting the Danish stock index to close at a record high after two trading days; Meanwhile, the food and beverage sector fell by nearly 0.5%, affected by expectations Beer giant Heineken fell 6.4% in 2024 profit, which is likely to fall far short of analysts' expectations.

Among other individual stocks, the organic cash flow generated is expected to be sufficient to solve the problem of convertible bonds and debt maturity in the next few years, and the online takeout platform Delivery Hero surged 19.6%, the biggest increase since December 2019, leading the way for Stoke 600 constituent stocks; while Thyssenkrupp, which lowered its annual sales and net profit guidelines, fell 10.5%.

The two-year British bond yield fell by more than 10 basis points, and the two-year US bond yield once fell more than 10 basis points from the February high

European treasury bond prices have rebounded, and British bond yields have taken the lead in the decline. By the end of the bond market, the yield on the UK 10-year benchmark treasury bond was about 4.04%, down about 10 basis points during the day, away from the high level since December 4, 2023, which was close to 4.17% refreshed after the US CPI was announced on Tuesday; the 2-year British bond yield was about 4.53%, falling about 12 basis points during the day, far from the high level since November 27, which was refreshed by 2.42% on Tuesday; the yield on Tuesday was about 2.33%, down about 6 basis points during the day; it rose 2.78% on Tuesday since December 1. The yield on the high 2-year German bond was about 2.72%, down about 3 basis points during the day.

The yield on the US 10-year benchmark treasury bond rose to 4.33% in early Asian trading, rising nearly 2 basis points during the day. After leveling off the rise and falling in the Asian market, the overall decline occurred. US stocks broke 4.25% to a new daily low in midday trading, falling about 7 basis points during the day, about 4.26% at the end of the bond market, falling more than 5 basis points during the day the CPI was announced.

The 2-year US bond yield, which is more sensitive to interest rate prospects, rose to 4.67% in early Asian trading, breaking the high level since the first day of the December 13 Federal Reserve interest rate meeting set on Friday for 2 consecutive days. After breaking 4.60% in midday trading, it fell to a new daily low of 4.55%, falling back nearly 12 basis points from the daily high. At the end of the bond market, it fell nearly 8 basis points during the day. After a major rebound on Tuesday, it fell on the 2nd day of this week and the 2nd day of the last six trading days.

The US dollar index fell after hitting a new high for three months, and Bitcoin's intraday market capitalization rose by more than $3,000, surpassing $1 trillion for the first time in more than two years

The ICE dollar index (DXY), which tracks the exchange rate of a basket of six major currencies including the US dollar against the euro, remained declining for most of the week. It only turned short-term before the European market and early trading. European stocks were close to 105.00 before the market, breaking the high level since November 14, 2023 for two consecutive days. The overall trend during the European and American trading period fluctuated downward. US stocks fell below 104.70 at noon, falling nearly 0.4% during the day.

By the close of the US stock market on Wednesday, the US dollar index was slightly above 104.70, falling more than 0.2% during the day; the Bloomberg US dollar spot index, which tracks the exchange rate of the US dollar against ten other currencies, fell nearly 0.2%, falling from the high level in the same period since November 16 last year, and the US dollar index both fell after two consecutive days of gains.

Among non-US currencies, the yen rebounded below 150.00 for the first time since November last year. The dollar rose above 150.80 against the Japanese yen at the beginning of the Asian session, approaching the high level since November 2023, which was refreshed by 150.90 on Tuesday, then quickly turned down and maintained its decline. European stocks fell to a new low of 150.35 before the market, falling 0.3% during the day; EUR/USD fell below 1.0700 in the European stock market. The US stock market quickly rose to 1.0700. The US stock market closed up and continued to rise after rising. At the moment Above 1.0720, it rose nearly 0.3% during the day; GBP/USD fell below 1.2540 in the European stock market, close to the low since December 23, which fell below 1.2520 last Monday. It fell more than 0.4% during the day. US stocks were above 1.2560 at the close, falling more than 0.2% during the day.

The offshore renminbi (CNH) fell to 7.2337 against the US dollar in early Asian trading, breaking the low level since November 17, 2023 for two consecutive days, and maintained gains after a rapid rise. US stocks rose to a new daily high of 7.2224 in early trading, rising 113 points from the daily low. At 5:59 Beijing time on February 16, the offshore RMB was 7.2243 yuan against the US dollar, up 71 points from the end of Tuesday's New York session, and rose on the second day of this week after falling back on Tuesday.

Bitcoin (BTC), which once fell back to $2,000 in early trading on Tuesday, rebounded strongly. After returning to 50,000 US dollars in early trading, US stocks quickly rose above $510,000. The trading price of a few platforms broke through the $52,000 mark in the short term, breaking the intraday high since December 2021 created before Tuesday's sharp decline, rising more than 7% from the intraday low of $49,000 in early Asian trading. US stocks were above $51,600 in the last 24 hours.

US oil ended seven consecutive gains and falls to a high of more than two weeks, and US natural gas hit a new low for more than three years on the 6th

International crude oil futures turned down in the middle of the day. At the beginning of the session, US WTI crude oil reached a new high of 78.80 US dollars, rising nearly 1.2% during the day. Brent crude oil hit 83.60 US dollars, rising about 1% during the day. After the announcement of US EIA crude oil inventories in early trading, they quickly declined and continued to decline. At a fresh low in midday trading, US oil was close to 76.50 US dollars, falling more than 1.7% during the day.

In the end, crude oil collectively closed down. WTI's March crude oil futures closed down nearly 1.58% to 76.64 US dollars/barrel after rising for 7 days on Tuesday; Brent crude oil futures for April closed down 1.17 US dollars, or 1.41%, to 81.60 US dollars/barrel for 2 consecutive days, breaking the closing low since last Wednesday, February 7.

US gasoline and natural gas futures fell sharply. NYMEX's March gasoline futures closed down about 3.2% to $2.3169 per gallon, falling back after rising for two consecutive days on Tuesday and breaking the high level since October 2 last year; NYMEX March natural gas futures closed down more than 4.73% to 1.609 US dollars/million British thermal units, falling for seven consecutive trading days, breaking the closing low since June 2020, continuing to record the longest continuous decline since October 20 last year. They hit a new low of at least three years since September 2020, falling to 1.59 US dollars per day and falling about 5.5.59 during the day.

Renxi stopped six times in a row, Yanglun copper fell, and Lunnickel rose three times in a row, gold fell five times in a row to hit a new low in February

London basic metals futures continued to rise and fall with mixed results on Wednesday. After rising for six consecutive trading days, Renxi retreated, saying goodbye to the two-day high of six months since August last year, which had rebounded for two consecutive days, and fell back below the Bank of America 8,200 and began to approach the low of nearly three months set last Friday. Lunzinc fell for two consecutive days, approaching the five-month low set last Friday.

Meanwhile, nickel rose for three consecutive days, breaking the high level since the end of January for the second day in a row. The lead, which has been falling for five days in a row, has left its low since November 2022. Lunlu, which fell back on Tuesday, also rebounded and did not continue to fall to the two-week low set last Monday.

New York gold futures generally maintained a downward trend on Wednesday. It was only in the short term that US stocks turned up in the middle of the day. US stocks reached as low as 1996.40 US dollars on the new day of early trading, falling more than 0.5% during the day.

In the end, futures fell for five consecutive trading days. COMEX April gold futures, which closed down nearly 1.3% on Tuesday, the biggest drop since January 3, closed down 0.14% to 2004.3 US dollars/ounce, breaking the closing low since December 13, 2023.

After falling below $2,000 intraday for the first time since December 13 on Tuesday, spot gold fell below $2,000 throughout the day. US stocks fell below $1985 in early trading, breaking their low since December 13 for two consecutive days, falling more than 0.4% during the day. The stock closed above 1990 US dollars, falling more than 0.1% during the day.

edit/ruby