The Yuxing InfoTech Investment Holdings Limited (HKG:8005) share price has done very well over the last month, posting an excellent gain of 36%. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 6.1% in the last twelve months.

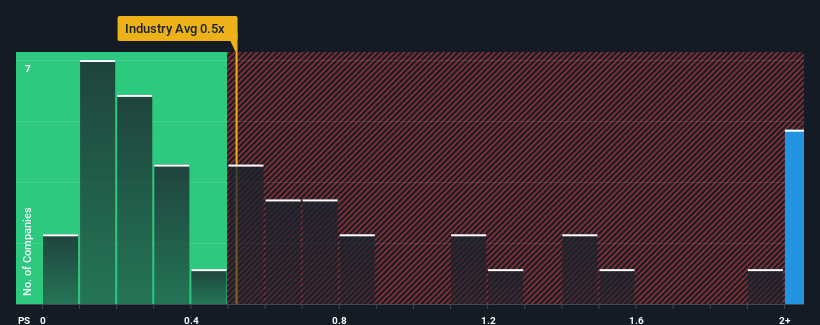

After such a large jump in price, you could be forgiven for thinking Yuxing InfoTech Investment Holdings is a stock not worth researching with a price-to-sales ratios (or "P/S") of 2.4x, considering almost half the companies in Hong Kong's Consumer Durables industry have P/S ratios below 0.5x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

SEHK:8005 Price to Sales Ratio vs Industry February 6th 2024

How Has Yuxing InfoTech Investment Holdings Performed Recently?

It looks like revenue growth has deserted Yuxing InfoTech Investment Holdings recently, which is not something to boast about. It might be that many are expecting an improvement to the uninspiring revenue performance over the coming period, which has kept the P/S from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

It looks like revenue growth has deserted Yuxing InfoTech Investment Holdings recently, which is not something to boast about. It might be that many are expecting an improvement to the uninspiring revenue performance over the coming period, which has kept the P/S from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Yuxing InfoTech Investment Holdings will help you shine a light on its historical performance.

Is There Enough Revenue Growth Forecasted For Yuxing InfoTech Investment Holdings?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Yuxing InfoTech Investment Holdings' to be considered reasonable.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. Whilst it's an improvement, it wasn't enough to get the company out of the hole it was in, with revenue down 44% overall from three years ago. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Comparing that to the industry, which is predicted to deliver 33% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this information, we find it concerning that Yuxing InfoTech Investment Holdings is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

What We Can Learn From Yuxing InfoTech Investment Holdings' P/S?

Yuxing InfoTech Investment Holdings shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our examination of Yuxing InfoTech Investment Holdings revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. With a revenue decline on investors' minds, the likelihood of a souring sentiment is quite high which could send the P/S back in line with what we'd expect. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Yuxing InfoTech Investment Holdings (1 is a bit concerning!) that you need to be mindful of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.