Zhejiang Dongri Limited Company (SHSE:600113) shares have had a horrible month, losing 26% after a relatively good period beforehand. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 21% in that time.

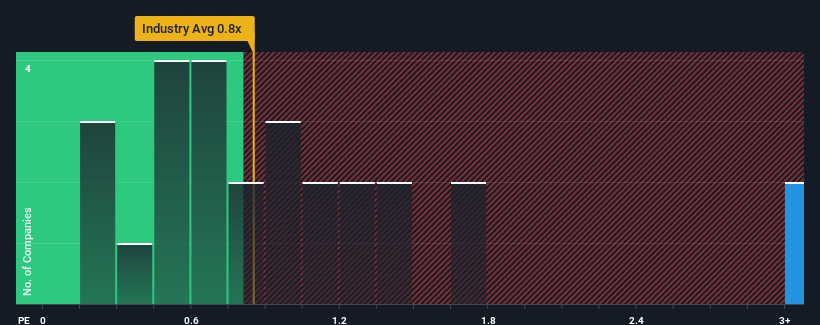

Although its price has dipped substantially, given around half the companies in China's Consumer Retailing industry have price-to-sales ratios (or "P/S") below 0.8x, you may still consider Zhejiang Dongri Limited as a stock to avoid entirely with its 3.7x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

What Does Zhejiang Dongri Limited's Recent Performance Look Like?

As an illustration, revenue has deteriorated at Zhejiang Dongri Limited over the last year, which is not ideal at all. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/S from collapsing. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Zhejiang Dongri Limited will help you shine a light on its historical performance.Is There Enough Revenue Growth Forecasted For Zhejiang Dongri Limited?

In order to justify its P/S ratio, Zhejiang Dongri Limited would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered a frustrating 24% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 45% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

This is in contrast to the rest of the industry, which is expected to grow by 17% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this in mind, we find it worrying that Zhejiang Dongri Limited's P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

What We Can Learn From Zhejiang Dongri Limited's P/S?

A significant share price dive has done very little to deflate Zhejiang Dongri Limited's very lofty P/S. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Zhejiang Dongri Limited revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. When we see slower than industry revenue growth but an elevated P/S, there's considerable risk of the share price declining, sending the P/S lower. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

Before you settle on your opinion, we've discovered 8 warning signs for Zhejiang Dongri Limited that you should be aware of.

If you're unsure about the strength of Zhejiang Dongri Limited's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.