The Jiangsu Seagull Cooling Tower Co.,Ltd. (SHSE:603269) share price has fared very poorly over the last month, falling by a substantial 27%. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

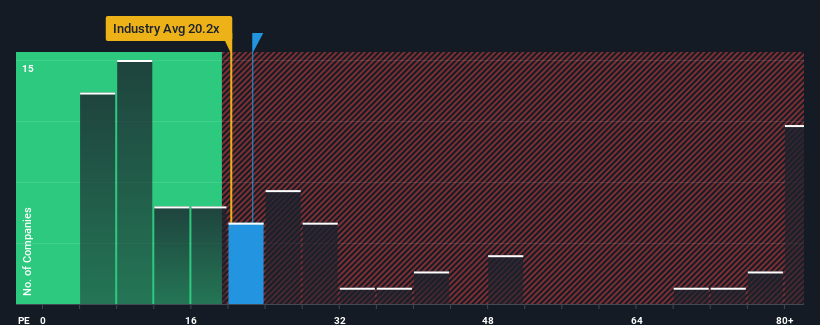

Even after such a large drop in price, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 28x, you may still consider Jiangsu Seagull Cooling TowerLtd as an attractive investment with its 22.6x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Jiangsu Seagull Cooling TowerLtd certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Jiangsu Seagull Cooling TowerLtd's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 25% last year. The strong recent performance means it was also able to grow EPS by 69% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the only analyst covering the company suggest earnings should grow by 102% over the next year. That's shaping up to be materially higher than the 42% growth forecast for the broader market.

With this information, we find it odd that Jiangsu Seagull Cooling TowerLtd is trading at a P/E lower than the market. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Bottom Line On Jiangsu Seagull Cooling TowerLtd's P/E

The softening of Jiangsu Seagull Cooling TowerLtd's shares means its P/E is now sitting at a pretty low level. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Jiangsu Seagull Cooling TowerLtd currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

It is also worth noting that we have found 2 warning signs for Jiangsu Seagull Cooling TowerLtd that you need to take into consideration.

If these risks are making you reconsider your opinion on Jiangsu Seagull Cooling TowerLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.