Kaili Catalyst & New Materials Co.,Ltd. (SHSE:688269) shareholders that were waiting for something to happen have been dealt a blow with a 28% share price drop in the last month. For any long-term shareholders, the last month ends a year to forget by locking in a 68% share price decline.

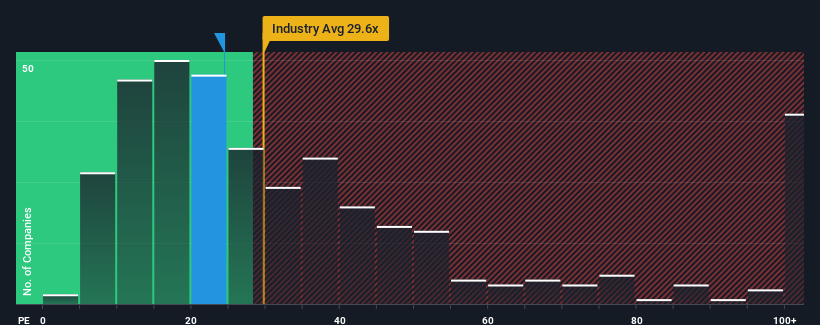

Although its price has dipped substantially, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 30x, you may still consider Kaili Catalyst & New MaterialsLtd as an attractive investment with its 24.4x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Recent times haven't been advantageous for Kaili Catalyst & New MaterialsLtd as its earnings have been falling quicker than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. Or at the very least, you'd be hoping the earnings slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

Check out our latest analysis for Kaili Catalyst & New MaterialsLtd

SHSE:688269 Price to Earnings Ratio vs Industry February 1st 2024 Keen to find out how analysts think Kaili Catalyst & New MaterialsLtd's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Any Growth For Kaili Catalyst & New MaterialsLtd?

The only time you'd be truly comfortable seeing a P/E as low as Kaili Catalyst & New MaterialsLtd's is when the company's growth is on track to lag the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 32%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 16% overall rise in EPS. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been mostly respectable for the company.

Shifting to the future, estimates from the two analysts covering the company suggest earnings should grow by 87% over the next year. That's shaping up to be materially higher than the 42% growth forecast for the broader market.

With this information, we find it odd that Kaili Catalyst & New MaterialsLtd is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Key Takeaway

Kaili Catalyst & New MaterialsLtd's recently weak share price has pulled its P/E below most other companies. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Kaili Catalyst & New MaterialsLtd currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Kaili Catalyst & New MaterialsLtd (of which 1 is a bit unpleasant!) you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.