① The copper mine to be acquired is a customer that Jin Chengxin is currently serving. ② Two unusual operations of “$1” and “gambling and borrowing” also appeared in the proposed acquisition plan.

Finance Association, January 22 (Reporter Liang Xiangcai) Jin Chengxin (603979.SH), which specializes in mining services, plans to become a “babysitter” and has taken another step towards the resource side by changing it to a “babysitter.”

One of the special features of this proposed acquisition is that the target copper mine is a customer that Jin Chengxin is currently serving. According to the announcement, the company has been undertaking underground mining service business for the target company Lubambe copper mine since 2017, and the relevant contract period is currently being executed from June 1, 2023 to June 30, 2026.

In addition, Kim Cheng-shin also showed unusual operations of “two dollars for 1 dollar” and “gambling and borrowing” in the proposed acquisition plan.

“Two $1”

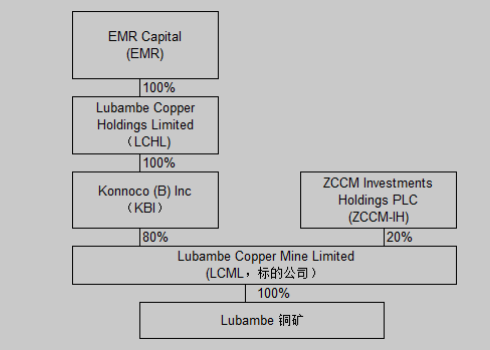

On January 21, Jin Chengxin announced that it plans to establish a new wholly-owned overseas subsidiary to acquire 80% of Lubambe Copper Mine Limited (LCML or target company for short) held by Konnoco (B) Inc. in Zambia for 1 US dollar.

In fact, there is a reason for this $1 “go through the motions” form of investment to collect a copper mine. According to the announcement, the target company to be acquired by Jin Chengxin is insolvent. As of September 30, 2023, LCML's net assets were about -15.1469 million US dollars. Although revenue for the same period was 89.565 million US dollars, net profit was -603.167 million US dollars.

Regarding the copper mine's current “dilemma”, Jin Chengxin also explained in the announcement. Due to various reasons, the mine has never been able to produce, and the seller chose to withdraw from the project due to time restrictions that the fund can invest and hold.

However, Kim Seong-shin still seems quite confident about changing the current situation where the target company is insolvent. According to the feasibility study announcement issued by the company on the same day, through technical reform of the copper mine, it is estimated that the project can achieve an average annual copper concentrate output of 77,500 tons, and the copper content of the copper concentrate is 32,500 tons. Based on a copper price of 8,300 US dollars/ton and a production period of 14 years, the total annual profit of the project was US$15.8815 million, profit after tax of US$126.882 million; the financial internal rate of return after tax was 17.36%, and the payback period after tax was 7.4 years.

In addition, the announcement also mentioned that it also purchased a claim resulting from a $857,116,770 loan to LCML from Lubambe Copper Holdings Limited (LCHL for short) for $1.

A CIFA reporter combed through the announcement and found that LCHL is the controlling parent company of the target company LCML. In other words, if the acquisition is completed, Jin Chengxin will have a claim of approximately US$857 million in its holding subsidiary LCML at a price of $1.

What is obvious is that in the current situation where LCML is insolvent, this claim of hundreds of millions of dollars can be described as a “white bar,” and whether it can be fulfilled depends on the future performance of the target company.

Screenshot of the shareholding structure form of Lubambe Copper Mine Source: Company Announcement

“Gambling and Borrowing” between old and new owners

In addition to the “two $1” mentioned above, in this proposed acquisition, the new and old owners are also involved in “gambling and borrowing” on the basis of anchoring the price of copper.

According to the announcement, LCHL will provide a loan of 40.5 million US dollars to the buyer (that is, a wholly-owned subsidiary of Jin Chengxin) on the premise that some of the agreed prerequisites (including but not limited to all necessary internal approvals and authorizations, and approval from the regulatory authorities) are met. The funds will be provided by the buyer to LCML through a loan to repay LCML's existing third-party priority commercial loans. The loan will be repaid in accordance with the repayment agreement between the buyer and seller. If the repayment obligation agreed in the repayment agreement is not triggered, the buyer is not required to repay the loan to the seller.

Let's look at the repayment agreement. There is a trigger point for the basic repayment obligation. That is, every year starting from 2027, when the average annual LME (copper) spot settlement price is higher than 8818 US dollars/ton, the buyer will repay the seller's loan based on the copper concentrate sales volume and cathode copper production volume (if any) of Lubambe Copper Mine in that year, and according to the ratio and calculation method agreed in the repayment agreement. The total payment amount for all years is no more than 55 million US dollars.

In addition to the above repayment, there is also an additional repayment obligation trigger point, that is, from 2027 to 2029, when the average annual LME spot settlement price is higher than 10,000 US dollars/ton, the buyer will repay the seller's loan according to the copper concentrate sales volume and cathode copper production (if any) of Lubambe Copper Mine in that year, and according to the ratio and calculation method agreed in the repayment agreement. The cumulative payment amount for all years is no more than 10 million US dollars.

In addition, the above repayment obligations, including meeting certain conditions, can be deducted accordingly, but the cumulative deductible amount does not exceed 10 million US dollars.

As for the buyer's loan, the announcement mentioned that the buyer's initial loan of 20 million US dollars will be paid after the seller's loan has been paid, and this loan has priority repayment rights over other LCML shareholders' loans. The funds will be used in conjunction with the seller's loan to repay LCML's existing third-party priority commercial loans, and the remaining funds, if any, will be used for LCML's day-to-day operations.

At the same time, from the date the buyer provided LCML with an initial loan of 20 million US dollars, the buyer will have the right to appoint directors and executives of the target company and make direct decisions on the operation and management of the Lubambe copper mine. If LCML has reasonable capital requirements in its daily operations, it will be provided by the buyer in the form of a loan.

In summary, it is easy to see that Kim Cheng-shin included a “gambling” element in this loan, and whether he repaid the loan and the loan repayment ratio depends on the room for future increases in copper prices. However, in the current situation where LCML is insolvent, Kim Chengxin's priority right to repayment of the target corporate loan is limited to a certain extent by LCML's future performance.

According to reports, Jin Chengxin's main business is the mine development service business, which includes mine engineering construction, mining operation management, mine design and technology research and development. As of the first half of 2023, mining service revenue was 2,996 million yuan, accounting for 91.38%; mining resource development revenue was 168 million yuan, accounting for 5.13%.

According to the research records disclosed by Jin Chengxin, the company's Dikulushi copper mine in the Democratic Republic of the Congo (DRC) has reached production. In 2023, it plans to produce about 8,000 tons of copper concentrate containing copper (equivalent), and plans to sell about 10,000 tons of copper concentrate containing copper (equivalent); the Lonshi copper mine will be put into operation in September 2023. The initial plan is to complete the climb in 2024 and reach production in 2025.