In 2023, Tesla was “in the limelight” and its stock price doubled in a year. However, at the beginning of 2024, Tesla was devastated by “Waterloo.” Since the beginning of the year, Tesla's stock price has dropped 15%, the worst performance since 2016.

As the Q4 earnings season gradually enters the right track, Tesla will release the fourth quarter results after the market on January 24, EST. According to consistent market expectations, Tesla is expected to record revenue of 25.764 billion US dollars in the fourth quarter, up 5.95% year on year; earnings per share are 0.62 US dollars, down 42.11% year on year.

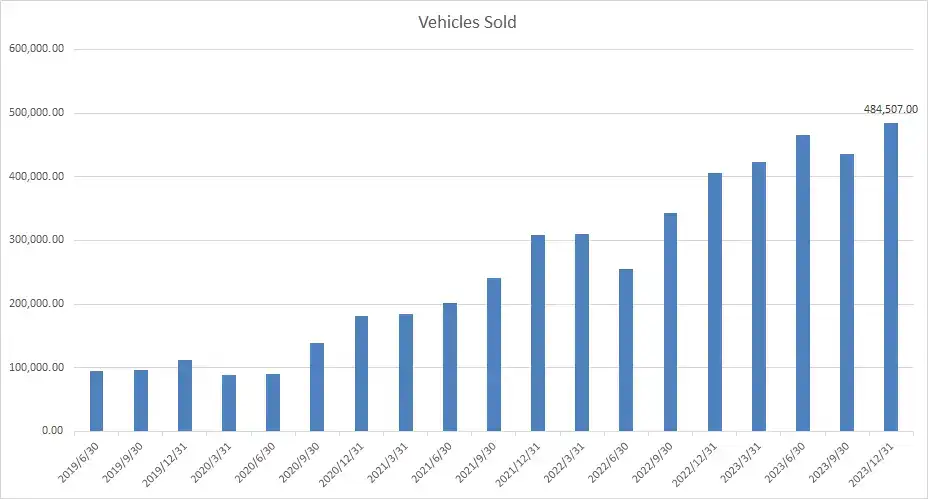

In the fourth quarter, Tesla's production and sales were slightly higher than expected, producing about 495,000 vehicles and delivering more than 484,000 vehicles. In 2023, Tesla's car deliveries increased 38% year over year to 1.81 million units, exceeding its previously set target of 1.8 million vehicles, but falling short of Musk's target of 2 million vehicles. Although deliveries reached a record high, the capital market's response to the news was lackluster.

As of now, in the fourth quarter earnings report, Wall Street analysts are still most concerned about the company's gross margin level.

As the most important observation indicator for each quarter, the overall gross margin for 23Q3 was only 17.9%. Notably, the gross margin for cars before regulatory credit is 16.3%.

Judging from historical data, in the past six quarters, Tesla's gross bicycle profit fell from $17,865 to $8,431, a drop of 53%.

Looking ahead to Q4 results, the market believes that Tesla raised the prices of cars sold in China four times in a row in November last year, mainly due to downward pressure on profits. Another reason was the decline in sales rankings in China, which was affected by competition brought about by price cuts in other new energy vehicles. The price increase behavior may use the fans' mentality of “buy up, not buy down” to promote sales growth.

However, Tesla lowered the prices of inventory cars sold in the US and Canada in the last quarter of 2023, mainly to cope with the impact of high interest rates on consumer sentiment, which means that gross margin may continue to weaken in the fourth quarter.

I/O Fund stock analyst Damien Robbins predicts that in the fourth quarter, automobile gross margin will be about 15.1%, excluding regulatory credit and operating leases; including operating leases, the gross margin for automobiles is expected to be 15.71%, down about 60 basis points from 16.33% in the third quarter.

In addition to gross margin, Tesla's 2024 sales guidelines are also an important focus of the market.

What do the Wall Street giants think?

Wells Fargo: Tesla is “one of the riskiest companies” this earnings season

An automotive analyst at Wells Fargo said Tesla is “one of the riskiest companies” this earnings season, and he expects the company to face various challenges in the coming year.

Wells Fargo analyst Colin Langan predicts that Tesla deliveries will only grow at around 13% over the next year, which is lower than the 50% long-term target set by the company. The year didn't start well for the electric car company, which has cut prices in some regions and suspended production in Germany.

The analyst predicts that in the most recent quarter, the impact of Tesla's price cuts outweighed the impact of increased sales. He predicted Tesla's gross margin of 15.4% for 23Q4, which is lower than analysts' general expectations.

Bernstein: Tesla's profitability in 2024 will also be further reduced

Bernstein, a well-known investment agency on Wall Street, recently mentioned in a report that automobile gross margin is still a key issue in the fourth quarter earnings report.

The analyst said that although Tesla's delivery volume in the fourth quarter was in line with expectations, there is still a downside risk in the automotive business's gross margin. The bank expects 15.7%, compared to the consensus forecast of 17.8%. For 2024, the bank expects Tesla's profit margin and sales volume to fall short of expectations, triggering investors to question the company's growth story.

Furthermore, Bernstein also said that 2024 “looks quite difficult” for Tesla, and investors will gradually question Tesla's growth prospects. The bank expects Tesla's delivery growth rate to be less than 20% in 2024 and 2025. This figure is far below Tesla's previous 50% annual growth target. The bank believes that Tesla will deliver up to 2.17 million vehicles in 2024.

Barclays: 2024 sales guidance may disappoint

Barclays analyst Tesla's price target was lowered from $260 to $250. The bank believes that Tesla's core theme in 2024 is facing sales pressure in an environment where demand is limited.

The analyst told investors in a research report that this year is the first time in the company's history, and sales may depend more on demand than Tesla's production capacity, which may cause investors to re-examine long-term sales expectations. The company expects Tesla to deliver 1.97 million vehicles in 2024, which is lower than market expectations of 2.19 million vehicles, with deliveries increasing by only 9% year over year.

Barclays also believes that the 2024 sales guidance may be disappointing, about 2 million units, but Musk may mention in the earnings conference call that if the macro and interest rate environment is good, sales may reach 2.2 million to 2.4 million units.

UBS: Tesla is expected to sell 2.06 million units in 2024

UBS said that the focus of investors' attention has turned to Tesla's earnings situation, particularly in terms of profit margins. Although some price reduction strategies boosted sales, they also had a negative impact on profit margins. In addition, sales expectations for 2024 have also attracted market attention. UBS expects Tesla to sell 2.06 million units in 2024.

HSBC: The factor that affects Tesla's market value is not car sales

According to HSBC analysts, Tesla's demand for electric vehicles “appears to have stabilized.” Although the company excels in electric vehicle manufacturing, the factors affecting its market value are not car sales, but rather uncertain commercialization progress of the Dojo supercomputer, FSD fully autonomous driving software, and the humanoid robot Optimus.

Morgan Stanley: Tesla will deliver 2.25 million cars in 2024, an increase of about 25%

Morgan Stanley analyst Adam Jonas is still optimistic about Tesla. He expects Tesla to deliver 2.25 million cars in 2024, an increase of about 25%. In September of last year, Jonas released a report saying that Tesla's Dojo supercomputer may increase Tesla's market value by up to 500 billion US dollars and give a target price of up to 380 US dollars.

How did the stock price perform on previous earnings days?

According to Market Chameleon, after backtesting the past 12 quarterly results days, the stock had a high probability of falling on the day of the results release, which was about 67%. The average change in the stock price was ± 7.0%, the maximum decline was -11.6%, and the maximum increase was +11.0%.

Currently, Tesla's implied change is ± 7.2%, indicating that the options market rose or fell 7% in a single day after betting on its performance; in comparison, Tesla's average post-performance stock price change in the first 4 quarters was ± 9.9%, indicating that the current option value of the stock is undervalued.

Judging from the bias in options volatility, market sentiment is slightly bearish on Tesla. An inquiry into yesterday's futures change order revealed that large investors sold call options that expire next Friday and exercise $225, traded 12,400, and bought these options at the same time. They traded 6,704 shares, involving nearly 5 million US dollars.

Cow friends,

The much-anticipated Tesla,

Can you hand over a satisfactory answer to the market?

Friends are welcome to forecast the rise and fall of Tesla's earnings report.

Is it a sharp increase of 5% or more, normal performance (-5%-5%), or a sharp drop of more than 5%?

Click to make an appointment:Tesla 2023Q4 results live

Editor/Somer