Maoye Commercial Co., Ltd. (SHSE:600828) shares have continued their recent momentum with a 33% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 50% in the last year.

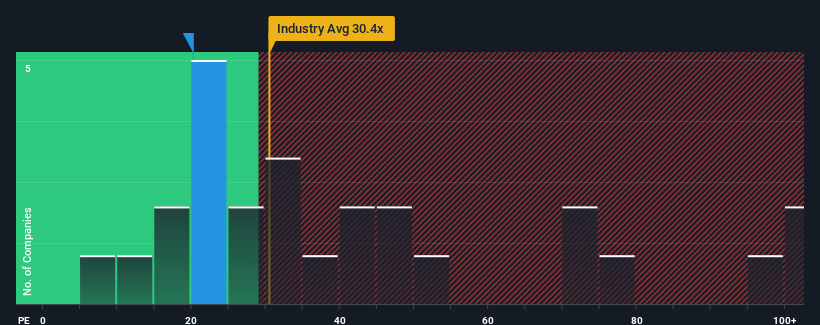

Although its price has surged higher, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 34x, you may still consider Maoye Commercial as an attractive investment with its 20.2x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With earnings growth that's exceedingly strong of late, Maoye Commercial has been doing very well. One possibility is that the P/E is low because investors think this strong earnings growth might actually underperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Maoye Commercial

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Maoye Commercial's is when the company's growth is on track to lag the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 255% last year. However, this wasn't enough as the latest three year period has seen a very unpleasant 37% drop in EPS in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

In contrast to the company, the rest of the market is expected to grow by 43% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we are not surprised that Maoye Commercial is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Key Takeaway

The latest share price surge wasn't enough to lift Maoye Commercial's P/E close to the market median. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Maoye Commercial revealed its shrinking earnings over the medium-term are contributing to its low P/E, given the market is set to grow. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. If recent medium-term earnings trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

Before you settle on your opinion, we've discovered 3 warning signs for Maoye Commercial (2 don't sit too well with us!) that you should be aware of.

Of course, you might also be able to find a better stock than Maoye Commercial. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.