这些雕塑来自一家平价超市奥乐齐。它们不仅形象传神,广告语也十分“接地气”,大白菜在呐喊“我好菜,但便宜啊!”、胡萝卜“我没胡说,我真便宜!”、“夸张!隔壁家的瑞士卷没吃完就过期了!”,文案无不围绕着“优质”“低价”“小包装”关键词。

这些雕塑来自一家平价超市奥乐齐。它们不仅形象传神,广告语也十分“接地气”,大白菜在呐喊“我好菜,但便宜啊!”、胡萝卜“我没胡说,我真便宜!”、“夸张!隔壁家的瑞士卷没吃完就过期了!”,文案无不围绕着“优质”“低价”“小包装”关键词。Source: Wall Street See

From the new showdown between ALDI and Hema, we can see how the retail industry will wage a 'cheap battle' in 2024.

Recently, in Shanghai Metro Jing'an Temple Station, there are several eye-catching oversized sculptures of vegetables, milk, and bread, causing passersby to stop and stare.

These sculptures are from the affordable supermarket ALDI. They are not only vividly sculpted, but the advertising slogans are also very down-to-earth. The cabbage shouts, 'I'm good, but cheap!' the carrot says, 'I'm not kidding, I'm really cheap!' 'Exaggeration! The Swiss roll next door expired before it was finished!' The copy revolves around the keywords 'high quality', 'low price', 'small packaging'.

These sculptures are from the affordable supermarket ALDI. They are not only vividly sculpted, but the advertising slogans are also very down-to-earth. The cabbage shouts, 'I'm good, but cheap!' the carrot says, 'I'm not kidding, I'm really cheap!' 'Exaggeration! The Swiss roll next door expired before it was finished!' The copy revolves around the keywords 'high quality', 'low price', 'small packaging'.

A rather ironic scene is that next to this scene is an ad for Sam's Club, which has led to netizens joking: false business warfare—price cuts, poaching, real business warfare—snide remarks, in-your-face aggressive tactics.

From Hema leading the charge with Move-the-Mountain pricing against Sam's Club, to ALDI stirring up waves again in the year-end business battle, in 2023, 'cost-effectiveness' is undoubtedly the main theme of the retail industry. The trend of low prices has blown from events like Good Deals and Happy Group Purchase to more retail channels: leading snack retailer Liangpinpu Group is busy expanding towards tens of thousands of stores, while 'the first stock of high-end snacks,' Bestore Co.,Ltd., has twice cut prices and 'rebranded itself'; the e-commerce platform targeting the sinking market, PDD Holdings, has market cap surpassing Alibaba; 'zhejiang china commodities city group' Miniso has achieved record-breaking performance this year, with many core data such as gross margin, net margin, achieving historic breakthroughs.

These cost-effective consumer representative companies are demonstrating an expansion speed and growth potential that surpasses the overall industry, highlighting prosperity.

This article will provide a detailed analysis on the following three points:

1. In 2024, 'low price' will remain the core of retail.

2. In the complex and ever-changing Chinese market, where will the retail discount format evolve?

3. The discount track is still in the early stages, the competitive landscape has not yet become clear, which leader in the track, like the overseas hard discount entering China – Olequ or the local retailer transitioning to a discount model – Hema will have the advantage?

Retail Essence: completing commodity circulation with the lowest cost and highest efficiency.

If 2012 is seen as an important turning point from offline to online retail, then 2023 is more like a turning point for the whole retail industry.

After the prosperity peaks and the giants' performance diverges, Alibaba and JD.com both feel anxious. On one side, with PDD Holdings, community group buying, live streaming e-commerce, and other price competition models, new traffic entrances have been opened. On the other side, new formats such as bulk snacks, discount supermarkets, etc., are rapidly emerging, forcing retail companies to optimize their supply chains.

The market is forming a consensus that future retail will return to its essence, which is to complete the circulation of goods with the lowest cost and highest efficiency.

The reason behind this is simple too. Currently, consumer demands have been fully satisfied, leading to an oversupply in the market. Consumers are no longer pursuing one-sided premium branded goods but are more focused on value for money. At the same time, the efficiency of retailers is not high enough, the markups on end products are still relatively high, and there is room for improving efficiency in the intermediate processes. For example, after streamlining the supply chain to the extreme, products at German discount store ALDI can be 20%-30% cheaper than in regular supermarkets, while bulk snack prices are around 10%-20% lower than in regular supermarkets.

In other words, the popularity of discount and other low-price channels is not only a manifestation of consumers' diminishing interest in brands and focus on the products themselves. The shift from low-efficiency channels to high-efficiency channels is an inevitable trend in the retail industry.

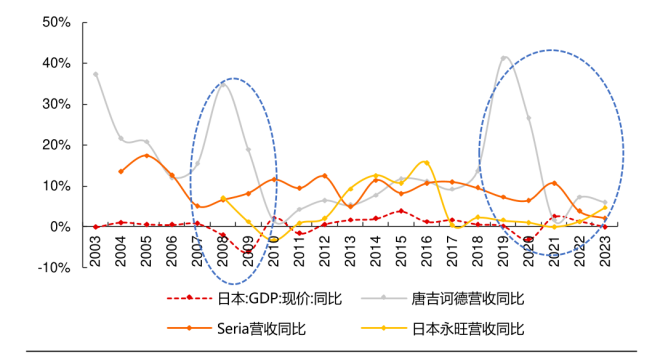

This point can also be inferred from the development path in Japan. According to the book 'The Fourth Age of Consumption' by Japanese consumer society expert Miura Ten, after 2005, Japan's consumption faced a situation similar to China's current one: in an economic downturn phase, consumption shifted from rapid growth in high-end branding to simple consumption. Correspondingly, Japan's retail channels transitioned from department stores to convenience stores and discount stores. The representative discount enterprise Don Quijote offers a product mix of '30% clearance + 70% regular price discount,' cleverly meeting the demands of different consumer groups such as price-sensitive individuals, young people, and housewives.

Don Quijote has maintained strong growth for 30 consecutive years, showing robust anti-cyclical growth capabilities. In the 2023 fiscal year, the company's revenue and net income attributable to the parent were 1.94 trillion yen and 76.4 billion yen, respectively. The compound annual growth rates from 2006 to 2023 were 12.5% and 18.3%, and the net margin increased from 1.7% in 2006 to 3.9% in 2023. Profitability has steadily improved, with the stock price rising more than sevenfold since 2006.

Unlike overseas countries, the penetration rate of hard discount formats in our country is still very low, with penetration rates of both community-based hard discounts and warehouse membership stores below 0.5%, presenting a huge opportunity. According to China Merchants Securities' calculations, based on the 15% penetration rate of community-based hard discounts in Germany and the 4% penetration rate of warehouse membership stores in the United States, assuming that the penetration rate of hard discounts in China reaches the global average level, the combined market space of community hard discounts and warehouse membership stores is expected to reach nearly 700 billion.

China's discount market in 2024: the battle between domestic and overseas, the battle between speed and efficiency

However, when it comes to the word "discount," most consumers may still first think of soft discounts represented by good deals and special promotions. The term "discount" seems inherently related to means such as closeouts and off-season sacrificing quality for low prices, often considered a "poor man's paradise."

But in Shanghai, a unique phenomenon is emerging. The discount supermarket "Aorqi" is becoming a popular destination for finance women and gym-goers after work, offering low-fat meals, sugar-free drinks, high-protein meats, all under 50 RMB. Praised as the 'most suitable supermarket for Shanghai's sophisticated working people' on Xiaohongshu, Aorqi is gaining popularity.

Unlike most budget supermarkets, despite selling goods at extremely low prices, Aorqi does not compromise on experience or quality. As you walk into the bread and deli section, a mix of warmth and fragrance wafts over you. Colleagues praise the 6 RMB German pretzel, saying it tastes better than those priced at upscale bakeries. For a small price, one can live a 'petty bourgeois life,' blending Shanghai's emphasis on 'appearance' and 'substance.'

This original 'hard discount pioneer' from Germany, with a century-old history, confidently offers such low prices due to extreme SKU and operational cost reduction, shortening the supply chain to improve efficiency, and introducing their own brands to lower retail prices. Cost reduction and efficiency improvement are the core logic of community discount stores like Aorqi.

Compared to Walmart's 0.1 million SKUs, Aorqi has only 1800, yet the sales per individual SKU are over 10 times that of Walmart's. Greater scale in procurement brings more significant pricing advantages. According to Wolfe Research's comparison of purchasing costs of a fixed basket of goods at ALDI and Walmart, ALDI's costs are only around 80% of Walmart's.

In order to compress costs to the extreme, Ouleqi pays employees higher wages than its peers and adopts a method where each employee handles multiple tasks, such as stocking and cashiering, to improve efficiency. Compared to Walmart and Target's traditional large stores with a sales per square meter of 4000-6000 US dollars, after squeezing out decoration costs, labor costs, stocking costs, and other factors, Ouleqi's sales per square meter is around 8800 US dollars.

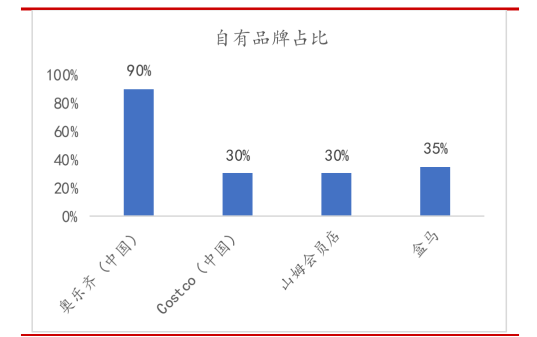

In stark contrast to other discount stores, Ouleqi has taken its own brand to the extreme, with 90% of its own brand products far exceeding the proportions of Costco, Sam's Club, and Hema. Even in the Chinese market, the proportion of its own brand products exceeds 70%. According to industry insiders, optimizing the manufacturing end of its own brand products could bring Ouleqi approximately a 40% price reduction.

As the largest discount retailer in Germany with over 10,000 stores globally, Ouleqi's expansion pace in China appears somewhat slow. In the 4 years since entering the Chinese market, they have opened 50 stores, which is not in line with the triple-digit expansion plan revealed by Ouleqi's China CEO Roman Rasinger in 2022.

However, starting from the second half of last year, there has been a noticeable effort from this German retail giant.

Whether attracting target groups of workers using basic ingredients like radishes and cabbages at the high-traffic Jing'an Temple station during peak commuter times with low prices, or marketing white-label products significantly below the prices of competitors, such as 10 sanitary napkins for 3.9 yuan, shampoo for 9.9 yuan per bottle, and hair conditioner with widespread marketing across the network, iterating and expanding SKU with selections more appealing to locals like "Old Shanghai Eight Treasures Duck," "Shanghai Laofandian Chinese New Year's Eve Dinner," and "International Hotel's Butterfly Puff Pastry without queues," Ouleqi is accelerating its transformation.

The most significant change is that over 80% of Ouleqi's existing suppliers are now local Chinese suppliers.

However, Aoluqi still faces challenges in the huge Chinese market to dominate, with Hema Fresh in Shanghai as the first major competitor. In order to expand its share of the discount market, Hema is also making every effort in its own reform.

The second half of last year became a turning point.

In October, Hema universally reduced prices of more than 5,000 items by 20% and planned to streamline the SKU to around 5,000. The support for the price reduction is a reconfiguration of the supply chain system. If Hema's previous advantage was in "understanding Chinese consumers," then the supply chain is the biggest weakness in the transformation of local retailers into discount formats, with uneven quality levels of product selection, and a variety of SKUs has always been criticized.

Hema is also making efforts to address this weakness. An important measure in the reform is a large-scale adjustment of the KA model that supermarkets used to follow, establishing a purchasing system core with "OEM/own production" similar to mature discount stores like Aoluqi and Sam's Club.

For example, in the past, Hema's production of large single items such as white toast, Hokkaido toast, mochi, and croissants required multiple processes and transportation to complete. Now, through their own Yihai Kerry factory directly delivering the flour to the Sugar Box factory, transportation and packaging costs for flour have been eliminated, while reducing labor costs significantly. Currently, the Sugar Box factory is designed with an annual production capacity of 20,000 tons, with an output value of 0.35 billion yuan.

At the same time, Hema decided to suspend membership renewal fees, although this has caused discontent among old members. If a supermarket positioning itself as high-end but lacks sufficient price advantages, and at the same time lacks competitiveness in product selection without clear differentiation, then the membership system is tantamount to being meaningless. Especially in the increasingly fierce competition in the discount market, compared to unrestricted discount formats like Aoluqi, there is no price advantage.

The reformed Hema is back in the spotlight.

Summary

Overall, the discount format is not only a subversion of the retail price system, but also a reshaping of the supply chain, brands, channels, and product structure. Adjustment in each link will trigger a redistribution of interests and profit models.

In 2024, affordability remains the core of retail. Whether it is domestic retail giants transitioning to the discount format or the "hard discount pioneer" entering China from overseas, in order to establish a firm foothold and gain absolute advantage in the early stage of the industry, they cannot rely solely on past experience models. They must actively seek change, with speed and efficiency becoming the key to market success.

If expansion is slow, scale effects cannot be achieved; if expansion is fast, it will face higher trial-and-error costs and greater capital investment. After the ebb of capital, whether the company itself has enough blood-making ability to continue to invest in strengthening moats is also the key to future competitiveness because not all companies have the backing of Alibaba like Hema.

Editor / ruby