Source: Golden Ten Data

Notably, a delay in the timing of interest rate cuts could ruin all of this. If the soft landing were right, then six interest rate cuts might be too much.

Investors are convinced that the Federal Reserve's next move will be to cut interest rates. But even if the Federal Reserve does follow suit, the timing of interest rate cuts may still leave the market in trouble.

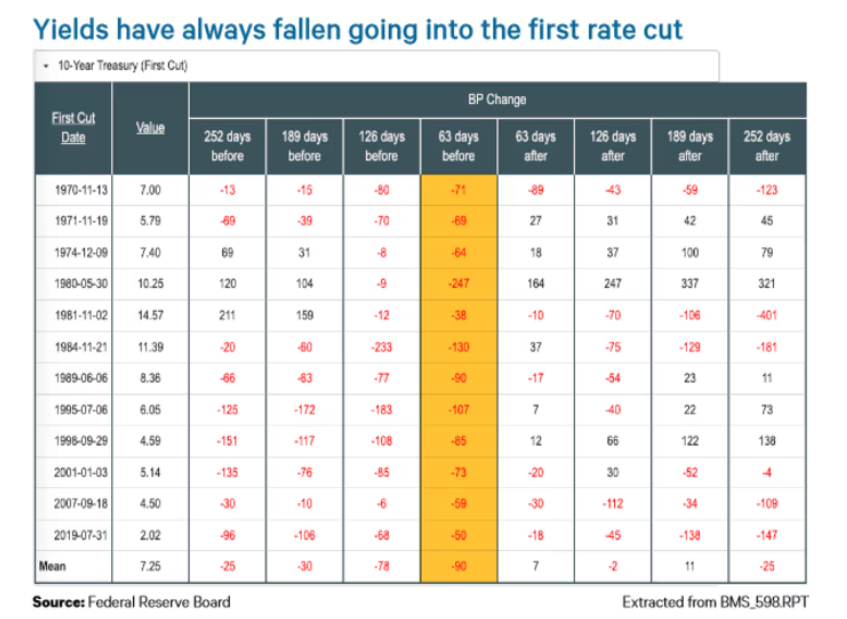

Ned Davis Research uses data from 1970 in the table below to show the performance of 10-year US Treasury yields in the three months before the Federal Reserve first cut interest rates.

As shown in the table, in every easing cycle since 1970, the 10-year US Treasury yield has declined by an average of 90 basis points in the three months before the first interest rate cut.

On December 20 of last year, three months before the market thought the Federal Reserve cut interest rates by 25 basis points in March, the yield on 10-year US Treasury bonds was 3.95%. Joe Kalish (Joe Kalish), chief global macro strategist at Ned Davis Research, wrote in a report this week that based on the lowest decline of 38 basis points in 1981, the yield will be 3.57% by March. “Some weak economic reports could allow us to achieve this goal,” he wrote.

Meanwhile, in another report this week, Kalish pointed out that in the three months before the Federal Reserve cut interest rates for the first time, stock market performance was often relatively stable, and the increase never exceeded 11% during this period. By Wednesday's close, the S&P 500 (SPX) was up only 0.1% since December 20.

However, Kalish said that after cutting interest rates for the first time, the stock market tends to rise in the next six to seven months. The S&P 500 index rose by an average of 12%, an average increase of about 21% throughout the easing cycle, with a median increase of 15.4%. Since 1970, the S&P 500 index has risen in every easing cycle, with the exception of a 27.6% decline after the tech bubble burst from January 3, 2001 to June 25, 2003.

As far as the Federal Reserve is concerned, it has not completely ruled out the possibility of further rate hikes, but it has kept the federal funds rate unchanged at 5.25% to 5.5% since July. According to the minutes of the Federal Reserve's December 12-13 meeting released on Wednesday, “several” officials said that the Federal Reserve may have to keep the benchmark interest rate stable “for a longer period than currently anticipated,” while “some” officials are pushing for some easing measures.

After the minutes of the meeting were released, traders lowered their expectations for interest rate cuts in March. According to CME's FedWatch tool, as of March 20, federal funds futures traders expect the possibility that the Fed will cut interest rates by at least 25 basis points by March 20 is 66.4%, down from nearly 87% a week ago.

Traders expect the probability that the Fed will cut interest rates by 25 basis points at least six times during 2024 is close to 60%, while the so-called bitmap of the Federal Reserve predicts only 3 such rate cuts.

Therefore, although historical data suggests that if the Federal Reserve cuts interest rates in March as planned, US Treasury bonds may rebound, Kalish told MarketWatch in a telephone interview that “the timing of interest rate cuts could ruin all of this.”

He said, “If the first rate cut doesn't start until May or June, [US Treasury yields] may move sideways or even pick up slightly.”

US stocks have also declined somewhat. Kalish said that investors may be reconsidering the pace of aggressive interest rate cuts in market pricing. He pointed out that six interest rate cuts will indicate that the economic situation is more serious, rather than a soft landing like the “Goldilocks,” and the soft landing is the reason for the rise in the stock market in 2023.

“If we achieve a soft landing, then cutting interest rates six times would be too much,” he said.

editor/tolk