① Banks reduce deposit listing interest rates with the aim of reducing bank debt costs, stabilizing bank interest spreads, and reducing interest rates on long-term deposits more. The adjustment time and extent of different banks will also vary according to their own circumstances and with reference to similar banks. ② It is expected that the concept of “round” or “batch” in deposit interest rate adjustments will gradually fade.

Financial Services Association, January 3 (Reporter Gao Ping) After some urban commercial banks followed up with major banks and stock banks to lower fixed deposit listing interest rates, a number of listed agricultural commercial banks also followed up the adjustments at the beginning of the year. A Financial Services Association reporter discovered that at the beginning of the new year, listed agricultural and commercial banks such as Changshu Bank and Sunong Bank recently lowered their fixed deposit listed interest rates. Some banks cut interest rates for fixed deposits at the same rate as major banks, up to 25 BP, while others only cut interest rates for terms of 2 years or more.

Industry insiders told the Finance Association reporter that local bank deposit interest rates are generally adjusted later than national banks. Banks lower deposit listing interest rates to reduce bank debt costs, stabilize bank interest spreads, and cut interest rates on long-term deposits more. The adjustment time and extent of different banks will also vary according to their own circumstances and with reference to similar banks.

Listed agricultural and commercial banks such as Changshu Bank and Sunong Bank followed up on the reduction period and margin differences

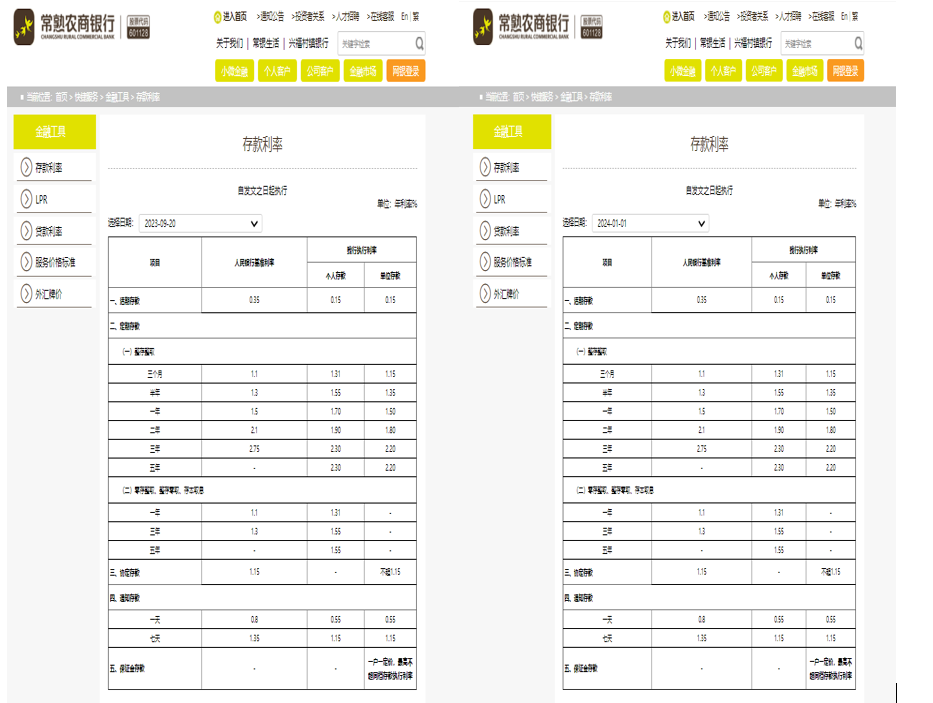

Listed agricultural commercial banks such as Changshu Bank and Sunong Bank all adjusted fixed deposit listing interest rates in the beginning of 2024. Specifically, the deposit interest rate implemented by Changshu Bank on January 1, 2024 shows that the bank's fixed deposit execution interest rates for 3 months, 6 months, 1 year, 2 years, 3 years, and 5 years are 1.31%, 1.55%, 1.7%, 1.9%, 2.3%, and 2.3%, respectively. Prior to that, the interest rates implemented by Changshu Bank from September 20, 2023 were 1.41%, 1.65%, 1.8%, 2.1%, 2.55%, and 2.55%, respectively. The decline was the same as that of the Bank of China. It was reduced by 10 BP for 1 year or less, 20 BP for 2 years, and 25 BP for 3 and 5 years.

Sunon Bank also implemented new interest rates at the beginning of the year. According to Sunong Bank's latest RMB deposit interest rate schedule, the bank's execution interest rates for 3-month, half-year, 1-year, 2-year, 3-year, and 5-year term deposits are 1.35%, 1.55%, 2.05%, 2.4%, and 2.4%, respectively. The effective time is 00:00 on January 1, 2024. Sunong Bank staff told the Financial Federation that prior to that, from September 5, 2023 to December 31, 2023, the bank's interest rates for term deposits were 1.35%, 1.55%, 1.8%, 2.1%, 2.55%, and 2.55%, respectively. It can be seen from this that Sunong Bank only lowered the listing interest rates for 2-year, 3-year, and 5-year fixed deposits on January 1, by 5BP, 15BP, and 15BP, respectively.

In addition to the banks mentioned above, a number of unlisted agricultural commercial banks also adjusted their listing interest rates for RMB deposits at the beginning of the year. For example, in order to meet the trend of interest rate marketization reform, the Yili Agricultural Commercial Bank will adjust the deposit listing interest rate starting January 1, 2024. After the adjustment, the bank's execution interest rates for one-year, two-year, three-year, and five-year term deposits were 1.55%, 1.75%, 2.05%, and 2.1%, respectively. Compared with previous information, they were lowered by 15BP, 25BP, 45BP, and 30BP, respectively. According to the changing trend of market-based interest rates, Huilai Agricultural Commercial Bank will adjust the deposit execution interest rate starting January 3, 2024.

Interest rates on deposits have been lowered again, and bank interest spreads are expected to stabilize

Since the two rounds of deposit interest rate cuts in June and September of last year, this adjustment, which began on December 22 last year, is the third round of widespread and drastic deposit interest rate cuts. Haitong International Banking Analyst Lin Jiali believes that the reduction in deposit interest rates will help stabilize interest spreads. The overall level of interest spreads in the banking industry has been declining for many years. At the end of the 3rd quarter of 2023, it fell to 1.73%, while the overall bad rate of the banking industry in the 3rd quarter was 1.61%. Considering that commercial banks also require employee investment, equipment maintenance, and preparation for future risks, the bank's profitability is extremely limited at this level of interest spreads.

“The monetary policy report for the second quarter of 2023 indicates that bank profits should be viewed reasonably. At the same time, whether it is a decline in LPR or an adjustment in mortgage interest rates, this is due to the decline in deposit interest rates. We believe this reflects the importance that the regulation attaches to the current low interest spreads in the banking sector, and the overall interest spreads in the banking industry are expected to gradually stabilize.” Lin Jiali said.

Zhang Xu, an analyst at Everbright Securities, believes that commercial banks' net interest spreads have continued to narrow in recent times, and the indicator fell to an all-time low of 1.725% in the third quarter of 2023. Moreover, changes such as lower personal mortgage interest rates will put more pressure on net interest spreads for the fourth quarter of 2023 and for some time to come. Currently, banks lower deposit interest rates to help stabilize net interest spreads and enhance the ability and sustainability of finance to support the real economy.

Looking forward to the future, Zhang Xu anticipates that the concept of “round” or “batch” in deposit interest rate adjustments will gradually fade. Banks can adjust their pricing of deposit products more flexibly according to the supply and demand conditions in the deposit market, trends in interest rates in the financial market, and the actual situation of the Bank within the framework of a market-based adjustment mechanism for deposit interest rates without affecting the fair and orderly competition order.