Source: Guotai Junan Securities Research

Household leverage ratio is an important indicator to measure the debt level of residents in a country, and this indicator also determines the government's attitude towards monetary policy and real estate policy to a large extent.

In the report on Regional Financial Operation released by the people's Bank of China last month, it is pointed out that the level of household leverage has a negative impact on consumption growth.

The report uses the method of econometric analysis to prove that after controlling factors such as per capita disposable income and the scale of social financing, for every 1 percentage point increase in residents' leverage ratio, the growth rate of total social retail consumption will decrease by about 0.3 percentage point.

This is also the first time that the Chinese government has quantitatively confirmed the negative correlation between household leverage and consumption.

In fact, the household leverage ratio is an important indicator of a country's household debt level, which largely determines the government's subsequent attitude towards monetary policy and real estate policy.

A few days ago, Guotai Junan's macro team sounded the alarm on the leverage ratio of residents in some provinces and cities in the article "the debt ratio of residents in some provinces and cities is nearly 80%, restricting monetary and real estate policies-- the 11th of a series of reports on the financial cycle."

Although the overall household leverage ratio is still within a controllable range, some provinces and cities have reached an unavoidable level, and this indicator will in turn restrict the next step of monetary and real estate policy.

01

Who is carrying the weight?

As of the end of 2018, the leverage ratio of China's residential sector was 52.6%.

Since this index is still lower than that of most developed countries, it is considered by many people to be within the scope of safety, but if we split it into provinces and cities, we will find that the results are very different.

The debt ratio of # 8 regions exceeds the national average:

Among them, 76% was in Zhejiang, followed by 68% in Shanghai, 64% in Guangdong, 61% in Gansu, 60% in Fujian, 59% in Beijing, 57% in Chongqing and 55% in Jiangxi.

Among them, Zhejiang, Shanghai, Guangdong and Beijing belong to economically developed areas, which are located in the core economic development zone of Beijing-Tianjin-Hebei, Yangtze River Delta and Pearl River Delta. Chongqing is relatively developed, Fujian is moderately developed, while Gansu and Jiangxi are relatively backward.

# debt ratio is in the range of 50-55%:

52% in Anhui, 52% in Ningxia, 51% in Guangxi, 51% in Hainan and 50% in Guizhou.

# debt ratio is in the range of 40-50%:

Hebei 46%, Yunnan 45%, Sichuan 43%, Jiangsu 42%.

By collating the household debt ratio data of 26 provinces and municipalities directly under the Central Government (some areas are missing) at the end of 2018, we can find that the current national leverage map shows an obvious "U" trend.

▼ at the end of 2018, areas with high leverage among residents

Source: Guotai Junan Securities Research, Wind

Note: the data in the figure show that the resident debt ratio in the corresponding area = the total household credit / the local GDP; debt ratio in the red area is more than 55%, and the debt ratio in the blue area is 40-55%. Henan 2018 data is missing, using 2017 data; Tianjin, Jilin and Heilongjiang data are missing.

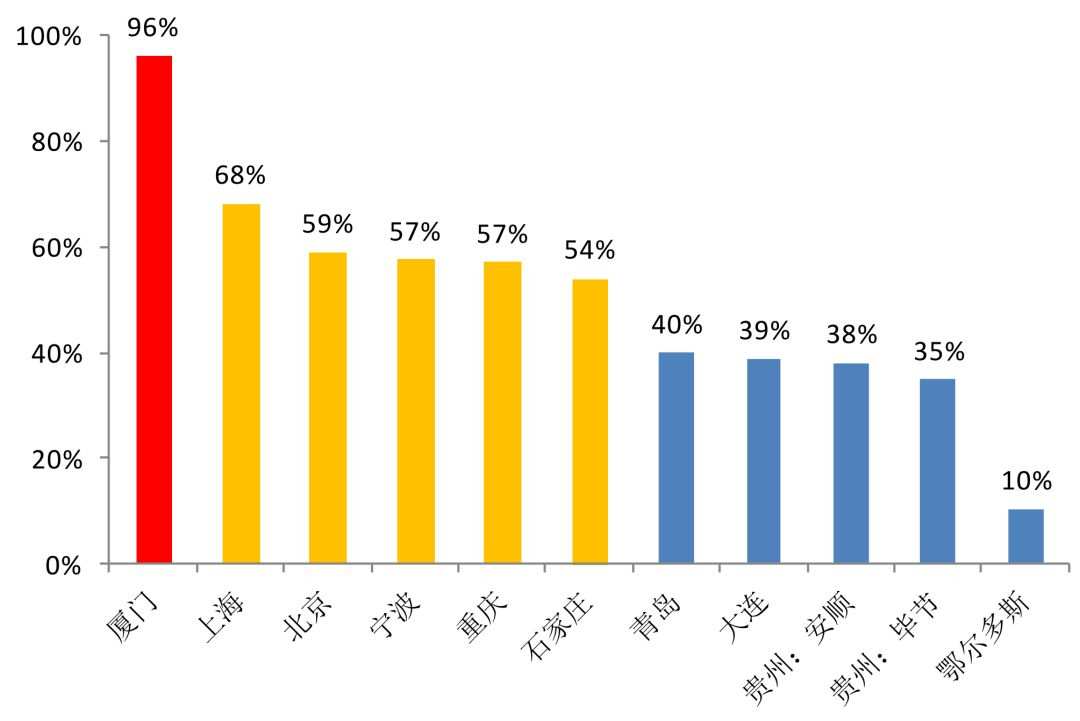

In addition to provincial data, we have also explored key cities.

Limited by the availability of data, we only get data from 11 cities, of which the debt ratio of residents in Xiamen is as high as 96%, and the debt ratio of Shanghai, Beijing, Ningbo, Chongqing and Shijiazhuang is all above 50%. The hidden risk is worth paying attention to.

According to the data of some cities in ▼, the debt ratio of residents in Xiamen is as high as 96%.

Source: Guotai Junan Securities Research, Wind

02

Is 53% of the residents' debt ratio high after all?

Residents' leverage ratio, as one of the important indicators for national decision-makers to determine real estate and monetary policy, is of great significance.

So what is the international level of such a figure of 52.6%?

By comparison, we found that in the same period in 2018, the average household leverage ratio in developed countries was 72.1%, while in developing countries, the figure was only 39.9%.

In other words, China's debt ratio is still lower than that of developed economies, but at a high level among developing countries.

According to ▼ BIS, the household debt ratio of China is higher than that of most developing countries, but still lower than that of developed countries.

Source: Wind, people's Bank of China, Bureau of Statistics, Guotai Junan Securities Research

However, it is worth noting that since the financial crisis in 2008, the deleveraging and debt ratio of developed countries have decreased, while the debt ratio of developing countries has increased moderately. Only China's debt ratio has risen rapidly.

In the past two years, the stock and margin of household sector debt ratio (credit balance / GDP) have risen rapidly, from 39 per cent at the end of 2015 to 55 per cent in mid-2019.

The debt ratio of ▼ residential sector has risen rapidly in the past two years.

Source: Wind, people's Bank of China, Bureau of Statistics, BIS, Guotai Junan Securities Research

The reason behind it is still related to the hot real estate market for many years.

By dividing the sources of household debt, we can see that at the end of the first half of 2019, the consumer debt ratio was 44%, while the operating debt ratio was only 12%, an increase of 16 percentage points over 2015, while the operating debt ratio maintained zero growth.

The increase in the debt ratio of residents in ▼ mainly comes from the consumption category, while the growth of the operating category is limited.

Source: Wind, people's Bank of China, Bureau of Statistics, BIS, Guotai Junan Securities Research

Furthermore, by analyzing the month-on-month changes in the debt ratio, the household debt ratio rose rapidly in the real estate boom in 2009, 2013, 2016 and 2017.

With the verification, the ratio of residents' new credit to commercial housing sales in that year also showed a jump trend in each round of real estate boom.

When the real estate boom was in 2009, the index was as high as 55 per cent, and has been around 40 per cent ever since, rising by about 53.5 per cent in 2016 and 2017.

The years of high growth of ▼ consumer debt correspond to the boom of the real estate market.

Source: Wind, people's Bank of China, Bureau of Statistics, Guotai Junan Securities Research

03

The "rich family" is still there.

So, is China's household debt leverage high enough to cause credit risk?

On this issue, the high savings rate of Chinese residents has long been seen as a firm cornerstone of resistance to risk outbreaks.

By international comparison, the global savings rate in both developed and developing economies has rebounded since 2010, with a global average of 26% at the end of 2018, 22% in developed economies and 32% in developing economies.

Therefore, China's current savings rate of more than 45% is more than ten percentage points higher than the average level of developing countries and twice that of developed countries.

With the support of the rapid development and accumulation of "thick family background" in the early stage, China will not cause a credit crisis in the short term.

Although the macro savings rate of ▼ has continued to decline in recent years, the absolute level is still high.

Source: Wind,IMF, people's Bank of China, Bureau of Statistics, Guotai Junan Securities Research

However, since the financial crisis, the continuous decline in the growth rate of household savings in China must also be paid attention to.

The growth rate has fallen from about 20% in the previous period to less than 10%, and the savings rate has also fallen from 51.8% in 2008 to 45% in 2018-especially in the past two years, and the current savings rate is expected to fall further.

The growth rate of ▼ gross national savings has declined, and the gross national savings rate has continued to decline to 46% in 2017.

Source: Wind,IMF, people's Bank of China, Bureau of Statistics, Guotai Junan Securities Research

On the other hand, we should also see that the high savings rate is also closely related to social security, population structure, capital market development, economic development process, cultural background and so on.

After our country enters the aging society, the population dependency ratio is on the high side, the social security system is not perfect, and we will face a large number of medical security-related pension expenditure demand in the future, which will have a negative impact on the savings rate.

Therefore, it is not advisable to rely entirely on high savings while ignoring the long-term debt risk.

04

The tone of "living in a house without speculation" is hard to change.

So what does the higher leverage ratio of residents mean for ordinary people (0, 67.960, 0. 00%)?

Generally speaking, for an ordinary family who buys a house on a mortgage in a small and medium-sized city, the total principal and interest will account for 28% of the income. 46%.

Further add to the daily living expenses (according to the Engel coefficient of 27.7% in 2018), then 60-75% of the average family's income will be occupied by basic living needs and house-related expenses, and the remaining income will be used to pay for education, health care and other expenses, as well as savings and unexpected expenses.

Objectively speaking, this is not very well-off.

However, the high leverage of residents brings more than just the difficulties of people's lives.

According to US data, all financial crises occurred after the household sector continued to accelerate leverage.

▼ previous crises in the United States occurred after the residential sector continued to leverage rapidly.

Source: Guotai Junan Securities Research, Wind,BIS

Under the environment of medium-and low-speed growth of the domestic economy, the slowdown of residents' income growth and the decline of the savings rate will most likely become the new normal in the future. the balance sheet of the residential sector is no longer indestructible and unbreakable (different income classes and different regions need to be taken into account).

This point, from the four ministries and commissions to strictly investigate "consumer loans", "cash loans", strictly prevent funds from illegally entering the property market, has also been confirmed from the side.

Therefore, on the whole, we believe that the fast-growing household debt must be moderated in order to effectively release risks in subsequent growth, and financial risk prevention and "housing speculation" will still be one of the main themes in the future.

Edit / emily