Over the past few years, the revenue and profit of collecting resources have fluctuated, but it has still reaped good performance, and business operations have been developing steadily.

Since the beginning of this year, international gold prices have soared from 1,800 US dollars to a record high of 2150 US dollars as the Fed's interest rate hike cycle nears its end, and the price of gold futures in Shanghai has reached a new high in 13 years.

At a time when the price of gold is expected to rise again, some gold-related companies, such as Jihai Resources (02489.HK), have submitted prospectus to the Hong Kong Stock Exchange and passed the hearing, making great strides into the capital market.

This means that as the third largest gold mining company in Shandong, Jihai Resources also became the first private gold mining company in Shandong Province to go public in Hong Kong, holding relatively scarce gold mining rights. According to information, the Hong Kong subsidiary of Zhaojin Group is the cornerstone investor of its IPO, which also shows an affirmation of the fundamentals and development prospects of marine harvesting resources.

So, looking back at the financial data, what is the quality of marine collection resources?

Business operations are steady, and gross margin is in the first tier of the industry

1. Stable revenue and profit performance

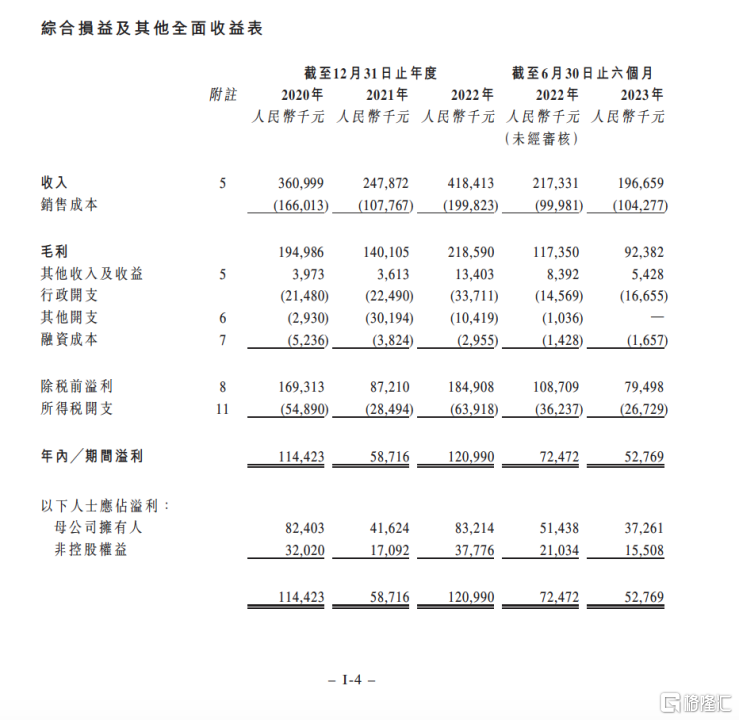

According to the prospectus, in 2020, 2021, 2022 and the first half of 2023, Jihai Resources achieved revenue of about 361 million yuan, 248 million yuan, 418 million yuan, and 197 million yuan respectively, and realized net profit of about 82 million yuan, 42 million yuan, 83 million yuan, and 37 million yuan, respectively.

Revenue and profit in 2021 were affected by production and market prices, etc., and there were slight fluctuations, but after a few years, the revenue scale was still very impressive, and the performance was steady.

In 2021, two major gold producing provinces, Shandong Province and Henan Province, were phased out, and gold production in various countries generally declined. Coupled with the cooling of gold investment sentiment, the spot price of gold in China showed a downward trend, falling from 392.4 yuan/gram on December 31, 2020 to 373.9 yuan/gram on December 31, 2021. In the end, various external factors caused fluctuations in the performance of marine harvesting resources.

Therefore, it can also be seen that since then, global gold prices have risen, production and operation have steadily resumed, negative external factors have been eliminated, and the revenue of marine harvesting resources rebounded markedly in 2022, with a sharp increase of 68.55% over the previous year.

Furthermore, due to the sharp rise in gold prices in the second half of 2023, combined with the “gold, nine silver, ten” peak consumption season, perhaps the revenue of harvesting resources for the whole year of 2023 is still quite optimistic.

2. Gross margin is in the first tier of the industry

According to the prospectus, in 2020, 2021, 2022 and the first half of 2023, the gross margin of gold sales of Jihai Resources was 54%, 56.5%, 52.2%, and 47%, respectively, and remained fluctuating around 50% in recent years.

Compared with other leaders, in the first half of 2023, Zijin Mining's gross margin of mine gold production was 47.09%, compared to 51.02% in the first half of 2022; in the same period, the gross margin of Sichuan gold was 44.58%, and the first half of 2022 was 49.28%. It can be seen from this that although the gross margin level of marine collection resources has fluctuated, it remains at the leading level in the industry.

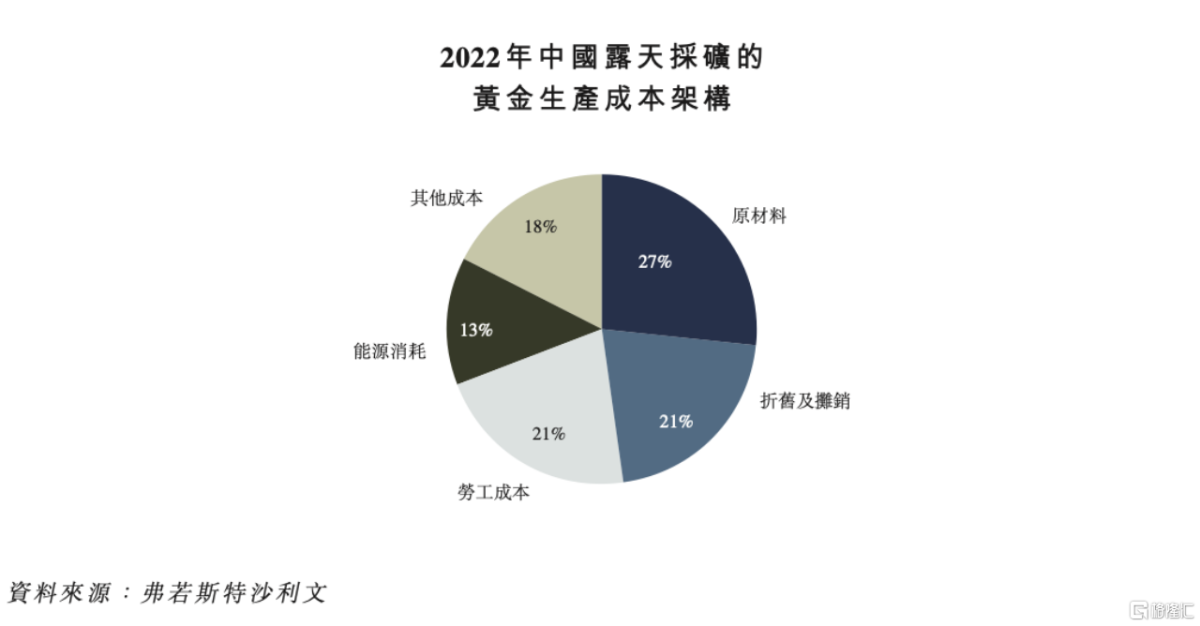

This is inseparable from the excellent cost control capabilities of marine harvesting resources. The cost of raw materials has always been the biggest component of gold production costs, and the company's business model is to undertake all mining work on its own. In this way, gold production costs are naturally controlled without outsourcing by a third party.

According to the prospectus, the company's average production cost in 2022 is about 186.3 yuan/gram, which is lower than the industry average of 298.0 yuan/gram mentioned in the Frost & Sullivan report. This is why its gross margin is in the first tier of the industry.

3. Production capacity is “full” and waiting for further expansion

In fiscal year 2022, the ore processed by the Jihai Resources Plant has reached 1991,000 tons/year, and the capacity utilization rate has reached 100.6%. In other words, under current production capacity, harvesting resources have made full use of existing production facilities to give full play to the scale effect, thereby further controlling costs and driving an increase in profit margin levels. This also means that with the completion of activities to expand the collection of marine resources, it is possible to expect breakthrough growth in their performance.

Therefore, judging from the above three sets of core data, it is easy to judge that under a healthy business model and sufficient production efficiency, when faced with the impact of external factors, harvesting resources can effectively reduce the negative impact. Based on the company's current scale and size, the overall performance performance is still good.

The upward channel of gold prices has not changed, and the growth of marine harvesting resources has been verified

Gold prices have been high in recent years. In particular, in the second half of this year, the price of gold reached a new record high, and both supply and sales in the gold market are booming, once again opening the door for investors to invest in gold, jewelry, and gold mining stocks.

In the author's view, now is the window of opportunity for gold mining stocks to be included in investment targets, and after the listing, Gahai Resources may enter investors' eyes.

First, in the medium to long term, the Fed's interest rate policy and market demand for gold will continue to support the rise in gold prices, and the income of gold miners is expected to soar and maintain growth.

The dominant trend in gold prices mainly depends on financial attributes and safe-haven attributes under the monetary function. US inflation continues to cool down, and the direction in which the Fed is moving from raising interest rates to cutting interest rates is clear. By 2024, when interest rate cuts begin, gold is in the range from the end of interest rate hikes to the beginning of interest rate cuts, long-term interest rates are expected to fall, which is good for gold. Furthermore, rising demand for additional gold purchases by central banks around the world will also provide an upward function for gold prices.

As the rise in gold prices brings about a revaluation of mineral resources and an appreciation of prospecting rights, it will increase the elasticity of gold miners' income growth. As for Gathering Resources, as one of the top five gold mining companies in China, it has a considerable amount of gold mining resources, industry-leading gross margin and capacity utilization, and along with revenue realization, it has released more excess profits to the capital market.

Second, after the production capacity of marine collection resources is expanded in the future, the annual output and revenue are still expected to surpass expectations in the market.

As a cyclical industry, the growth of gold miners also depends on mining capacity. After listing, capital raising will further enrich the capital volume, and offshore resources will be able to further build and expand infrastructure or optimize mining, breaking through production capacity bottlenecks. As a result, gold production is increased, and the company is actually generating revenue from operations to accelerate growth. The construction and expansion of infrastructure will also further spread risks and reduce the impact of discontinuation of production and maintenance on the overall operation of enterprises.

In addition to the revenue side mentioned above, the cost side of marine harvesting resources may also have a lot of room for improvement in the future.

Over the past few years, the total production maintenance cost (AISC) of gold mines has been getting higher and higher. In the third quarter of this year, it has already exceeded 1,300 US dollars/ounce. However, as inflation declines in the future and falling oil and gas prices will drive prices of key cost drivers such as diesel, energy, and cyanide to fall, the cost side is expected to stabilize or even decline.

So despite the rise in AISC, overseas gold producers remain optimistic. Newmont expects its AISC guidance standard for 2023 to be $1150-1,250 per ounce, and Barrick expects its AISC guideline to be $1,170-1,250 per ounce, a decrease compared to last year and is expected to continue to decline.

For harvesting resources, gross margin may improve, compounded by revenue growth, thereby boosting profits, and profit margins will begin to rise. Therefore, in the long run, marine harvesting resources will continue to show greater potential and value.

Epilogue

Over the past few years, the revenue and profit of collecting resources have fluctuated, but it has still reaped good performance, and business operations have been developing steadily.

This also reflects from the side that the listing of Sea Collection Resources is not like some companies. Losses and business problems are left aside for small and medium-sized investors, but they hope to use the capital market to obtain more opportunities, open up space for imagination, and create value.

After listing, the revenue side of Jihai Resources improved to meet more market demand through resource expansion. A sharp rise in volume and price may lead to better stock price flexibility. At this time, you might as well give Jihai Resources higher expectations.