The three major US stock indexes continued to rise for five weeks, and the NASDAQ reversed the weekly decline with a rebound on Friday. The Dow reached a record high in the past two years, and FTSE's earnings for the component stock market rose nearly 16% weekly. Tesla continued to fall after delivering trucks; Pfizer, which abandoned the development of diet drugs, fell by more than 5%; and Dell once fell close to 10% after its earnings report. The China Securities Index declined. Pinduoduo fell for the first time since its earnings report, but it surged 22% this week. It rebounded for the first time since Station B's earnings report. It was still down 19% this week, and Xiaopeng Motor fell by more than 5%.

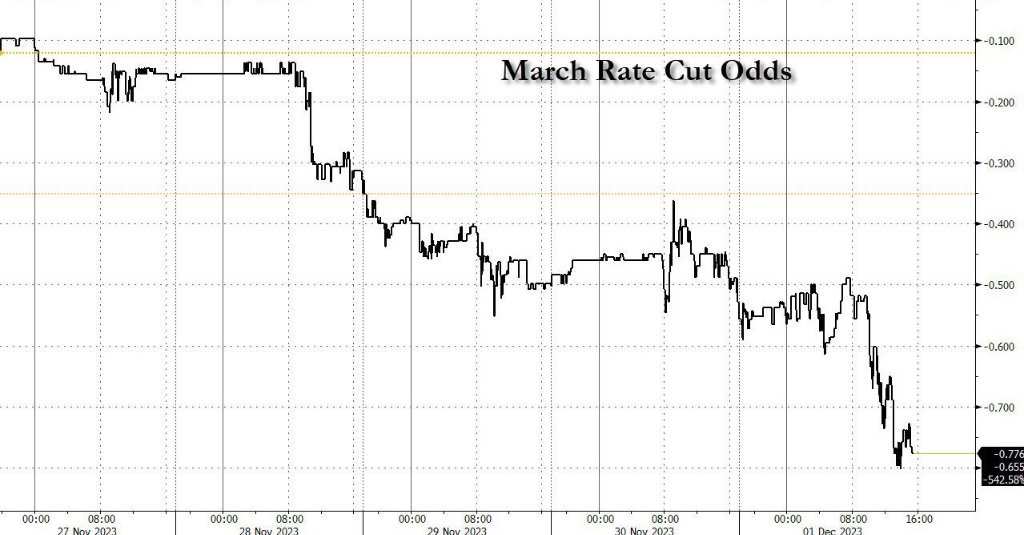

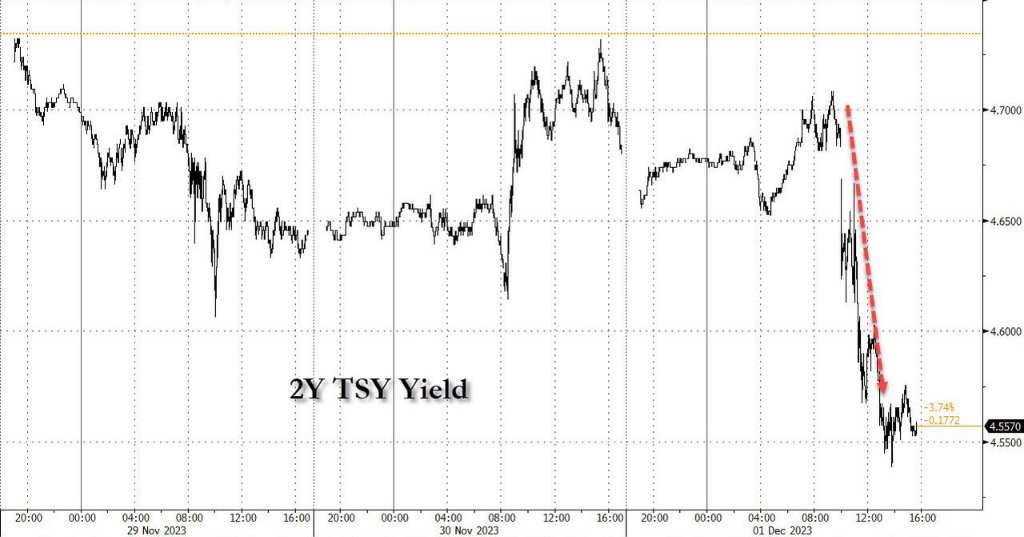

After Powell's speech, two-year US Treasury yields jumped more than 10 basis points, hitting a five-month low. The US dollar index made a U-turn and declined, falling from a one-week high, falling for three weeks for the first time in five months. At one point, the offshore renminbi rebounded by more than 300 points, recovering 7.13 in the intraday period and close to a four-month high. ECB officials encouraged two-year German bond yields to fall by nearly 40 basis points in a week.

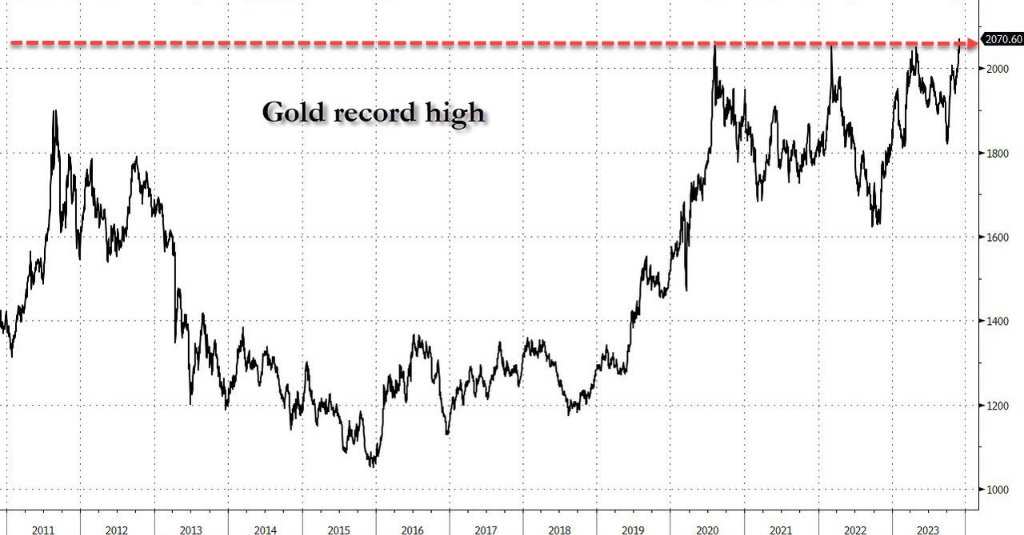

After the OPEC+ meeting, crude oil fell to a two-week low for two consecutive weeks and fell for six weeks in a row. Gold rebounded, futures rose for three weeks, and spot gold was approaching historic highs. Lundtong rose to a four-month high twice in a row, and Lunkel rebounded more than 5% in a week. Updating

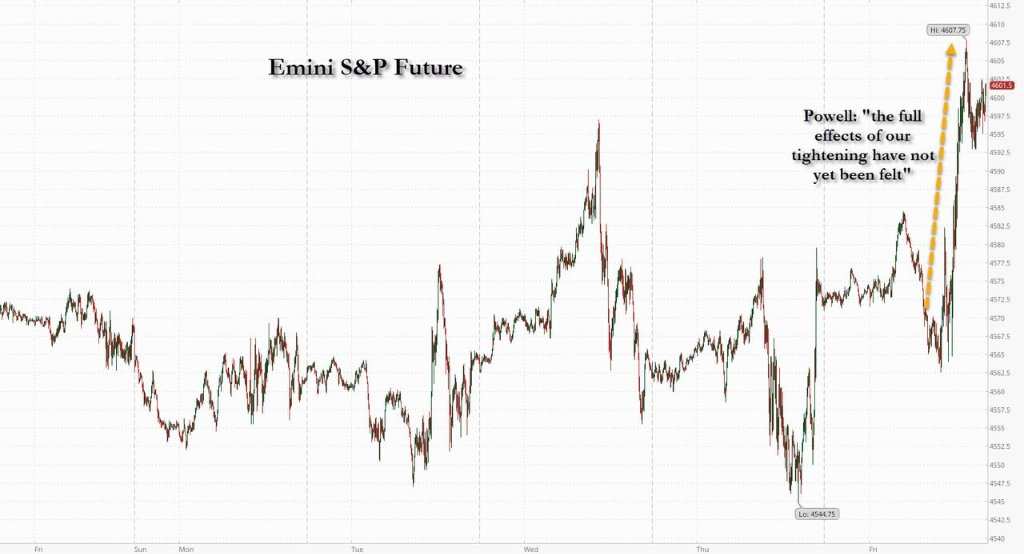

Federal Reserve Chairman Powell continued the previous day's rhetoric of suppressing expectations of interest rate cuts by Fed officials, saying that it is still too early to judge when easing will occur, and that the Fed is still preparing for further tightening when necessary. However, US bonds did not repeat Thursday's trend. Instead, intraday prices rebounded and yields dived.

Commentators said that Powell's current speech reiterated that prudence was taking shape and suggested that a soft landing was taking shape. Coupled with the continued weakness of the US ISM manufacturing index announced on Friday, they all strengthened the market's expectations that the Fed would cut interest rates as early as the first quarter of next year, driving up stocks and bonds. Other commentators mentioned that Powell pointed out that the impact of monetary policy on the economy is lagging behind, and that past austerity has not yet shown its full impact. This has heightened expectations that the Fed has already raised interest rates.

Prior to Powell's speech, the exchange rate of US stocks and bonds had relatively little fluctuation. After Powell's speech, US bond yields quickly leveled off gains in the intraday period and declined. Interest rate sensitive two-year US Treasury yields fell by more than 10 basis points, falling below 4.60% for the first time in five months. The yield on benchmark ten-year US bonds also evened out Thursday's increase, falling by more than 10 basis points to a three-month low. The US dollar index made a U-turn and declined after Powell's speech. It fell from the one-week high that was refreshed before Powell's speech. It was the first time in five months that it has been falling for three weeks in a row.

Before Powell's speech, the three major US stock indexes opened lower collectively, and the Dow quickly turned upward, and the NASDAQ, which was dragged down by chip stocks and other technology stocks, continued to decline. After Powell's speech, the US stock market rose, the Dow's gains expanded, and S&P and the NASDAQ turned upward. The NASDAQ leveled the losses of the previous few days this week with a rebound on Friday, maintaining a weekly upward trend, and other stock indexes continued to rise for more than a month.

Among the key individual stocks, after releasing positive financial results on Thursday, Saifushi continued to take the lead in supporting the rise in the Dow; Tesla failed to reverse the decline after it began delivering the electric pickup truck Cybertruck. China Securities has generally declined. Pinduoduo's stock price fell on the first day since the financial report was released. Due to the sharp rise on the day of the earnings report, the trend of this week's surge did not change, while the stock price of Station B continued to fall continuously after the earnings report was announced, and will plummet by double digits throughout the week.

The prices of US and European bonds rebounded collectively this week, and yields declined. Goldman Sachs advanced the estimated time for the ECB to cut interest rates for the first time from the third quarter of next year to the second quarter. On Friday, ECB officials gave their heads off. Villeroy, the ECB Governing Council and Bank of France Governor, said that the ECB may consider cutting interest rates next year. If any impact is not taken into account, interest rate hikes have already gone too far, and the data supports the central bank's view that inflation will fall back to target. Villeroy's speech contributed to a sharp decline in yields on European bonds, especially short-term Eurozone treasury bonds. This week, when it was announced that Eurozone CPI for October had slowed beyond expectations, yields fell by a double-digit basis point.

Supported by the declining dollar, non-US currencies rebounded in the intraday period, and various commodities rose. Gold, whose gains were suspended on Thursday, rebounded at an accelerated pace. For the first time in history, the main New York futures contract was close to 2010 US dollars. Spot gold is one step away from its historical high. Part of the benefit was that China's Caixin manufacturing PMI did not fall but rose to an expansion range in November. London basic metals generally rose, and Lundong reached a high level of nearly four months.

International crude oil, on the other hand, fell further after the OPEC+ oil production policy meeting and fell to a two-week low, continuing the trend of gradual weekly decline for more than a month. The decline in oil prices shows that the decision of the OPEC+ meeting on Thursday disappointed the market. There was no formal announcement of a joint production reduction commitment after this meeting, implying that OPEC+ has internal differences, and investors doubt that OPEC+ will eventually be unable to implement the new production cuts.

The three major US stock indexes continued to rise for five weeks, falling for the first time after FTSE's earnings report, Zhou Pinduoduo's earnings report, and will continue to rise sharply this week

The performance of the three major US stock indexes after they collectively opened low was varied. The Nasdaq Composite Index fell more than 0.6% at the beginning of the session, and the S&P 500 index fell close to 0.3% at the beginning of the session, then narrowed some of its losses. The Dow Jones Industrial Average quickly turned up slightly after falling less than 40 points at the opening. After Powell's speech in the US stock market in early trading, the S&P and NASDAQ rose one after another, and the Dow's gains expanded. At midday trading, the Dow rose more than 310 points and rose nearly 0.9%, the S&P rose nearly 0.7%, and the NASDAQ rose 0.6%.

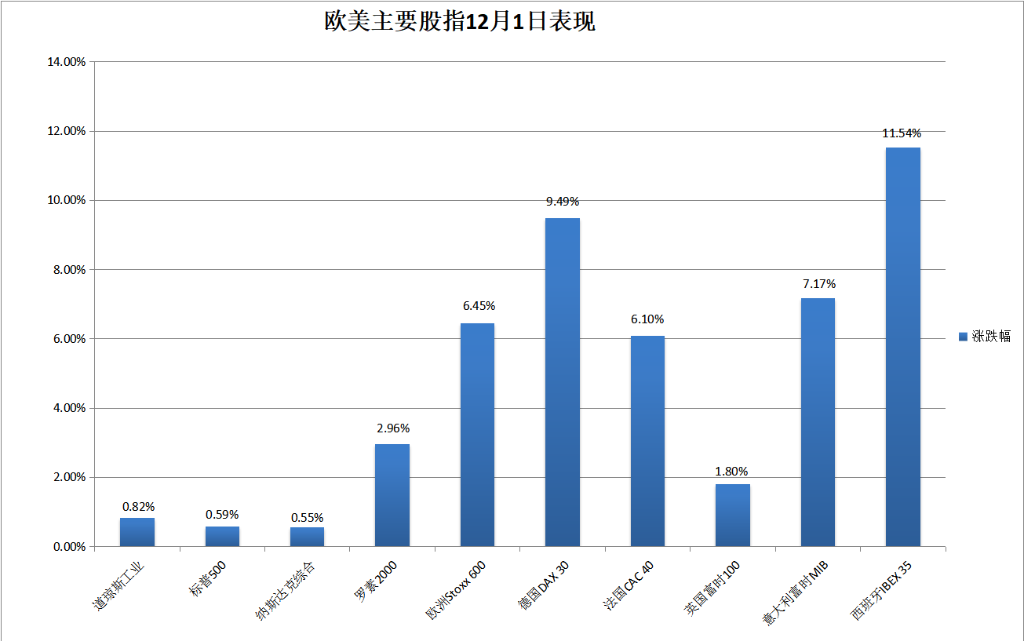

In the end, the three major indices collectively closed higher. The Dow closed up 294.61 points, or 0.82%, to 36245.5 points. It closed above 36,000 points for the first time since January last year. It has been rising for four consecutive days and hitting a new closing high since January last year for two consecutive days. S&P closed up 0.59% to 4594.63 points, a new closing high since March 30 last year, rising for two consecutive days. The NASDAQ closed up 0.55% to 14305.03 points. After two consecutive days of decline, it rebounded to its highest level since July 31.

The small-cap stock index Russell, which is mainly value stocks, closed up 2.96% in 2000, rising to a high level since September 14 for three consecutive days. The Nasdaq 100 index, which focuses on technology stocks, closed up 0.31%, breaking away from its low since November 17, when it fell for two consecutive days on Thursday. The Nasdaq Technology Market Value Weighted Index (NDXTMC), which measures the performance of technology industry constituent stocks in the Nasdaq 100 Index, closed down less than 0.1%. It fell for three days in a row and hit a new low since November 15 on the two days. It fell 0.61% this week, falling after four weeks of continuous gains.

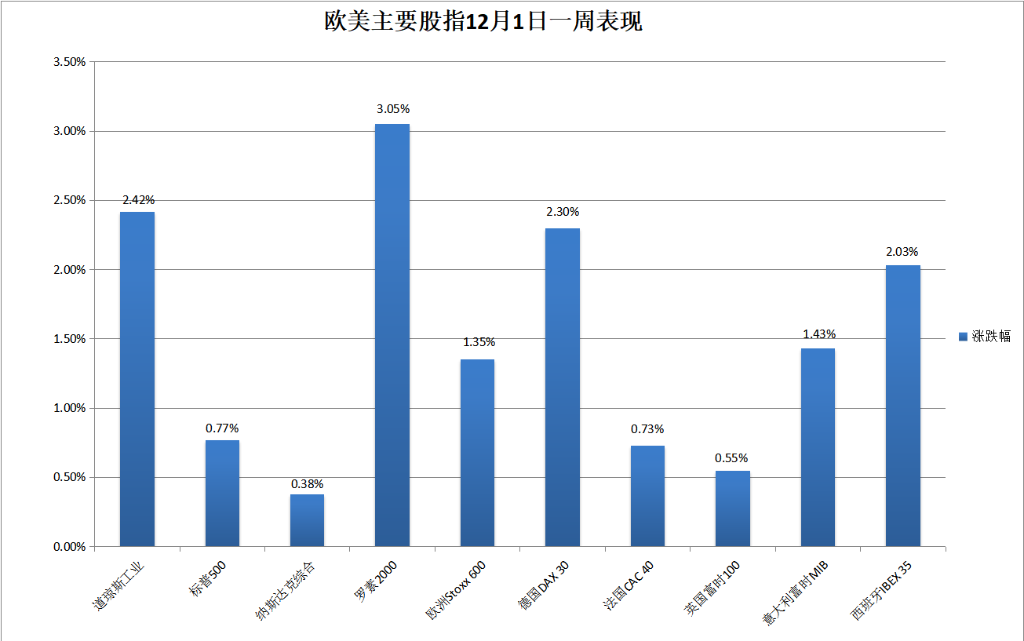

Major US stock indexes continued to rise this week. The Dow rose 2.42%, the S&P rose 0.77%, the NASDAQ rose 0.38%, and the Nasdaq 100 rose 0.1%, all rising for five consecutive weeks. The Dow recorded its longest weekly rise since 2021. Russell 2000 rose 3.05% for three consecutive weeks.

Among the constituent stocks of the Dow Index, pharmacy stock Walgreens led the way with a rise of more than 4% at the close, while Saiftshi (CRM), which surged after the release of its earnings report on Thursday, rose by more than 3%. Followed by a rise of more than 9% on Thursday, SFC has accumulated a cumulative increase of nearly 16% this week.

Among the major sectors of the S&P 500, only Google and Meta, which had fallen more than 0.2%, closed down on Friday, and communication services. Interest rate sensitive real estate rose more than 2%, led by more than 2%, while utilities, industry, materials, and non-essential consumer goods all rose by more than 1%. This week, only two sectors, telecommunications services and energy, declined by about 2.5% and 0.1% respectively. Out of the nine sectors that rose, the real estate sector rose 4.6%, far ahead of other sectors. Finance, materials, and industry all rose by more than 2%.

Leading technology stocks fell sharply in early trading, but later turned upward. Tesla continued to decline the day after starting delivery of Cybertruck and disclosure of pricing details. At the opening of the market, it fell more than 3% and closed down 0.5%. It fell for three consecutive days, as it surged 4.5% on Tuesday and continued to rise throughout the week, rising more than 1.4%.

Among FAANMG's top six technology stocks, Netflix closed down 1.7%, falling to a low level since November 15; Microsoft closed down nearly 1.2%, falling back to a one-week low; Facebook parent company Meta closed down 0.7%, falling to a low since November 9; Google's parent company Alphabet closed down 0.5%, falling to a low level since November 13; falling less than 1%, while Apple closed up nearly 0.7%, rising to a high level for two days to a week; and on Thursday, Amazon, which had been low since November 21, rose more than 0.6%.

Among these technology stocks, only Apple and Amazon rose by about 0.7% and 0.2% respectively this week, Meta fell nearly 4%, Alphabet fell more than 3%, Netflix fell nearly 3%, and Microsoft fell nearly 0.8%.

Chip stocks generally rebounded during the intraday period. The Philadelphia Semiconductor Index and the semiconductor industry ETF SOXX fell more than 1% in early trading, closing up nearly 0.3% and 0.5% respectively. They both rebounded after falling back on Thursday, falling nearly 0.3% and rising more than 0.1% respectively this week. By the close, Intel fell by more than 2%, and Nvidia fell slightly. This week, it fell more than 2%, while Arm rose nearly 4% and AMD rose nearly 0.2%.

The popular Chinese stock market, which mostly rebounded on Thursday, retreated. The Nasdaq Golden Dragon China Index (HXC) closed down 1% and returned to a downward trend after stopping three consecutive declines on Thursday. This week, the cumulative decline was nearly 4.1%. Among the key individual stocks of the week, Pinduo initially fell by more than 3% and closed down nearly 1.5%. It fell for the first time since the earnings report was released on Tuesday, with a sharp rise of 18% on Tuesday and a cumulative increase of 22.4% this week; Station B fell more than 3% at the beginning of the session, reverted to an intraday increase, and closed up about 1.6%. It closed higher for the first time since the financial report was released on Wednesday. It closed higher for the first time since the earnings report was released on Wednesday. It fell by more than 10% on Wednesday, and fell 18.6% this week. After announcing the November delivery volume, Xiaopeng Motor closed down more than 5%, while NIO Auto and Ideal Auto fell by more than 1%. Among other individual stocks, NetEase closed down more than 3%, Alibaba, Baidu, and Tencent Pink closed down more than 1%, and JD fell nearly 1%.

Among the more volatile individual stocks, Ulta Beauty (ULTA), a beauty product retailer whose profit in the third quarter was higher than expected and raised at the bottom of the full-year revenue guidelines, closed 10.8%, leading the S&P 500 constituent stocks; after the media said it and Apple began negotiations to provide discounted bundled streaming services, the media group Paramount (PARA) closed 9.8%, which was also a major driver of S&P; the Internet of Things company Samsara (IOT), whose quarterly results and guidelines were superior to expectations, rose 25.6%; according to the media, “Sister Wood” Cathie Wood's fund After Ark Invest sold its shares for the third time this week, Coinbase (COIN), the largest cryptocurrency exchange in the US, closed up nearly 7.3%; while Pfizer (PFE), which announced that it had abandoned the development of experimental diet drugs due to its high incidence of side effects, fell more than 7% in early trading to close 5.1%; and Dell (DELL), which had lower sales than expected in the third fiscal quarter due to weak demand for personal computers, fell nearly 10% and closed down 5.2% at the beginning of the session.

In terms of European stocks, China's Caixin PMI is improving, and Powell has hinted that a soft landing is taking shape to jointly push the pan-European stock index to rise for the third day in a row. The European Stoxx 600 Index reached a new closing high since July 31. The stock indexes of major European countries rose sharply. 'Among all sectors, the basic resources of mining stocks surged 4.2%, leading the way. Thanks to mining giant Anglo-American Resources, which closed 7.9% and led the stock share of Stoke 600, was upgraded from neutral to bought by UBS, another mining company, Antofagasta, rose 6.2%.

The Stoxx 600 Index rose more than 1% this week, rising for three weeks. National stock indexes have also risen steadily. German stocks and Western stocks have been rising for five weeks, French stocks have been rising for three weeks, and British and Italian stocks, which have declined last week, have rebounded. Due to the sharp rise on Friday, the basic resources sector rose 3.6% this week, and the real estate increase of more than 4% performed better, reflecting the impact of the prospects for interest rate cuts.

Two-year German bond yields fell nearly 40 basis points in a week, US bond yields jumped more than 10 basis points after Powell's speech

The dovish remarks of European Central Bank Governing Council member and Bank of France Governor Villeroy boosted the price of European treasury bonds to rebound after stopping three consecutive increases on Thursday. Yields declined, and yields on interest-sensitive short-term bonds fell the most.

By the end of the bond market, the yield on the 10-year British Treasury bond closed at 4.13%, down 4 basis points during the day; the yield on the 2-year British Treasury bond closed at 4.49%, down 8 basis points during the day; the yield on the benchmark 10-year German treasury bond closed at 2.36%, down 9 basis points during the day; and the yield on the 2-year German bond closed at 2.67%, down 14 basis points during the day.

This week's European bond and US bond yields both declined after rebounding last week, and short-term German bond yields declined sharply, reflecting the impact of the slowdown in Eurozone CPI and central bank officials on Friday. The yield on 10-year British bonds, which rose by about 18 basis points last week, fell by about 15 basis points, and the yield on 2-year British bonds fell by about 18 basis points; the yield on 10-year bonds fell by about 28 basis points last week, and the yield on 2-year German bonds fell by about 39 basis points.

The US 10-year benchmark treasury bond yield rose above 4.35% before the US stock market to a new high, and was above 4.30% before Powell's speech. After his speech, it quickly fell below 4.30%, and the decline continued to expand. US stocks were downgraded 4.20% after closing, breaking a new low since the beginning of September. By the end of the bond market, it was about 4.20% at the end of the day, falling by nearly 13 basis points during the day. After rising by about 3 basis points last week, a cumulative decline of about 27 basis points this week.

The yield on 2-year US Treasury bonds, which are more sensitive to interest rate prospects, rose above 4.71% before Powell's speech and continued to decline after Powell's speech. The US stock market fell 4.60% at the end of early trading and fell by 4.54% at the end of the session, breaking the intraday low since early June. It was about 4.54% at the end of the bond market, falling by about 14 basis points during the day.

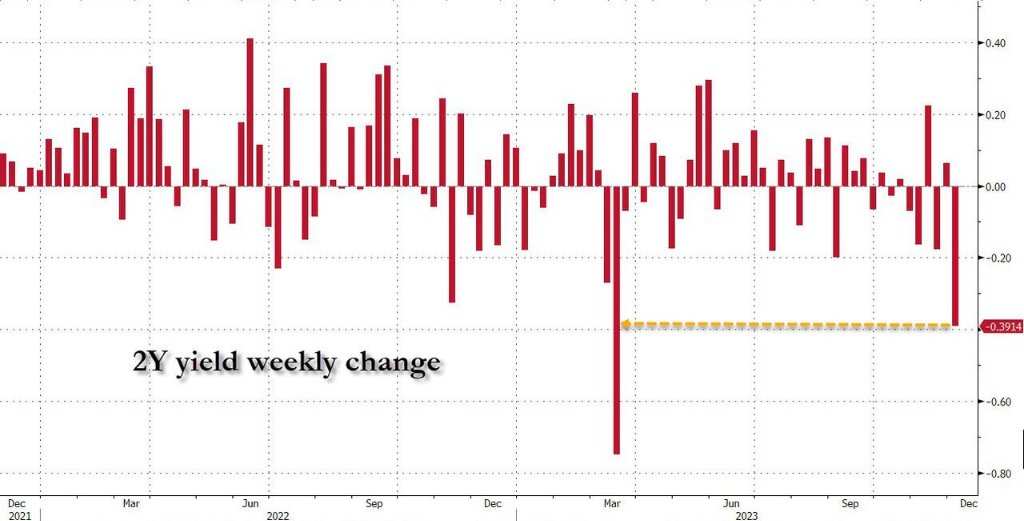

After rebounding and rising by about 6 basis points last week, 2-year US Treasury yields fell sharply by about 41 basis points this week, marking the biggest weekly decline since the collapse of Silicon Valley banks triggered the banking crisis in March this year. This means that short-term US debt recorded the best weekly performance in eight months.

After Powell's speech, the US dollar index made a U-turn and declined for the first time in five months, falling for three weeks, and the offshore renminbi recovered 7.13 in the intraday period and was close to a four-month high

The ICE US Dollar Index (DXY), which tracks the exchange rate of the US dollar against a basket of six major currencies, including the euro, rose above 103.70 in early trading after turning higher before the US market, breaking the high since November 24, rising more than 0.2% during the day. Powell quickly turned down after beginning his speech. At noon, the US stock market was close to 103.10 to a new daily low, falling close to 0.4% during the day.

By the time the US stock market closed on Friday, the US dollar index was hovering around the 103.20 line, falling nearly 0.3% during the day, and falling 0.2% this week; the Bloomberg dollar spot index, which tracks the exchange rate of the US dollar against ten other currencies, fell nearly 0.4% this week, and the US dollar index both fell after two consecutive days and fell for three weeks for the first time since June 16, the longest consecutive week of decline in more than five months.

Non-US currencies rebounded in the intraday period. The yen rebounded sharply in early trading in US stocks, and the dollar fell below 146.70 in midday trading, breaking the two-month intraday low set by Thursday, falling 1% during the day; GBP/USD fell below 1.2620 in early US trading to a new daily low, then quickly rebounded and accelerated upward. At noon, US stocks rose above 1.2710, beginning to rise close to Wednesday's fresh three-month high of 1.2730; EUR/USD fell below a fresh three-month high of 1.2730 in early trading; EUR/USD fell below 1.2730 in early trading Low, falling more than 0.5% during the day. US stocks turned upward in midday trading. At closing, they fell slightly during the day, hovering The 1.0880 line is still not close to the three-month high of close to the 1.1020 refresh on Wednesday.

The offshore renminbi (CNH) hit a new daily low of 7.1558 against the US dollar in the European stock market. US stocks continued to rebound and turned higher in early trading. After recovering 7.13 in midday trading, they hit a new daily high of 7.1237, beginning to approach Wednesday's rise above 7.12 to 7.1126 on July 27, rising to a high since 7.1161, rising 321 points from a daily low. At 5:59 on December 2, Beijing time, the offshore renminbi was 7.1,242 yuan against the US dollar, up 217 points from the end of Thursday's New York session. It rebounded after falling back on Thursday. It rose 248 points this week, rising for three consecutive weeks.

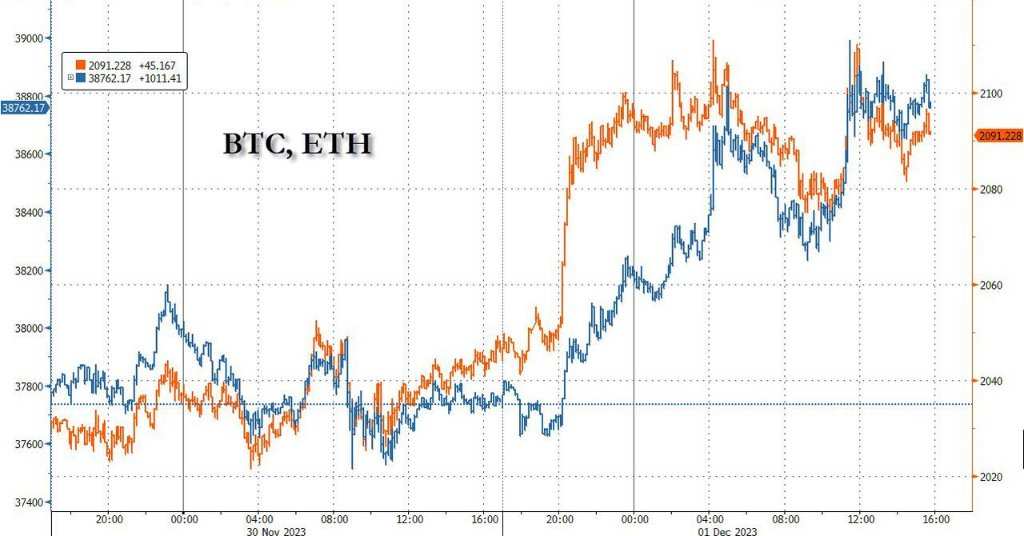

Bitcoin (BTC) increased intraday gains in the US stock market. US stocks were close to 39,000 US dollars after closing, breaking the high since May last year set last Friday. It rose more than 1,300 US dollars, up nearly 4% from the intraday low in early Asian trading, then fell back below 38,900 US dollars. It has risen nearly 3% in the last 14 hours and more than 3% in the last 7 days.

After the OPEC+ meeting, crude oil fell to a two-week low for two consecutive weeks and fell for six weeks

International crude oil futures reversed several times during the intraday period on Friday, but failed to rebound successfully. When US stocks hit a new daily high in early trading, US WTI crude oil was close to 76.80 US dollars, up more than 1% during the day, and Brent crude oil rose above 81 US dollars, up more than 0.8% during the day. After the midday trading, the decline in US stocks all widened to more than 2%, and crude oil fell below the $80 mark.

In the end, WTI's January crude oil futures closed down nearly 2.49% to 74.07 US dollars/barrel; Brent's February crude oil futures closed down 2.45% to 78.88 US dollars/barrel. Both US oil and US oil closed down for two consecutive days, breaking new closing lows since November 16.

This week, U.S. oil fell by a cumulative total of 1.94%, while crude oil fell by about 2%, falling for six weeks in a row. Since the outbreak of the Arab-Israeli conflict for eight weeks, crude oil has only been rising in the first two weeks, and has continued to decline since then.

U.S. gasoline and gas futures have had mixed ups and downs. NYMEX January gasoline futures closed down 2.5% to $2.12 per gallon. After three days of continuous increases, they fell 0.7% this week for six weeks; NYMEX January gas futures for January closed up 0.43% to $2.8140 per million British thermal units, leaving behind the new low since September 20 on Thursday, falling 6.17% this week, falling 6.17% for four weeks.

Lun Tong rose twice in a row to a four-month high, Lun Nickel rebounded more than 5% in one week, and gold rebounded for three weeks

London basic metals futures mostly rose on Friday. Luntong rose for two consecutive days, breaking 8,600 US dollars for the first time since the beginning of August. Lun Lu, who had been down for 8 days, and Lun Zn, which had been down for 4 days, both rebounded, leaving behind their respective one-month lows on Thursday. Both Renkel and Lentsig, which fell back on Thursday, rose more than 2%. Renkel did not continue to be close to the closing low since April 2021 set on Monday, nor did Renxi approach the low since late March set on Monday.

Basic metals have had mixed ups and downs this week. Last week's decline of more than 4.5% led the decline by more than 5%, the first increase in the last six weeks, and Lundance rose more than 2%, rising for three consecutive weeks. Meanwhile, Lun lead fell more than 3% for two weeks, Lun Zinc fell more than 1%, and Lun Xi fell close to 0.6%. They all fell for three weeks. Lun Aluminum, which rebounded last week, fell 0.3%.

New York gold futures, which fell on Thursday, rebounded strongly. The main futures contract in February rose above $2,090 in midday trading on Friday. At one point, it was close to $2096 to $2095.7, breaking the intraday high of $2089.20 on August 7, 2020, and rising nearly 1.9% during the day.

In the end, COMEX December gold futures closed up 1.61% to 2017 US dollars/ounce. COMEX February gold futures closed up 1.58% to $2089.7 per ounce, breaking the closing record of $2069.40 set on August 6, 2022, leveling off Thursday's decline and reaching a record high.

Spot gold rose to 2075.41 US dollars/ounce at noon in the US stock market, approaching the record high of 2075.47 US dollars/ounce set on August 7, 2020, and rose more than 1.8% during the day.

In this week, which closed down only on Thursday, New York futures continued to rise for the third week in a row. Since the Arab-Israeli conflict, they have only been declining for the week ending November 10.

edit/ruby