This year, luxury sports brands continued to be popular, so the Internet once joked that the “middle class three-piece set” had become Archeopteryx, Salomon, and Lululemon.

The reason behind this phenomenon may be reflected that in China or even around the world, the integration of sports and light luxury racing tracks may continue to penetrate the hearts of the people and exert impressive power.

Among them, it can be verified from the performance of A-share or Hong Kong-listed companies. For example, Biehenleven and HONMA Golf, which focus on golf sportswear and products, can be verified.

According to financial reports, Biehenlöfen's operating profit and net profit on the return account increased by 80.8% and 78.9%, respectively, compared to '19.

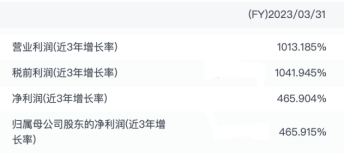

As for the latter, HONMA Golf, its operating profit and net profit increased by 1013.2% and 465.9% respectively from three years ago.

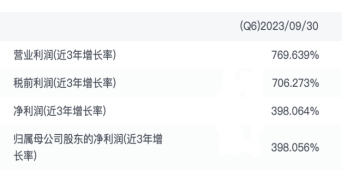

Even judging from the first half of the year's financial report (FY23/24) data just released a few days ago, HONMA Golf's operating profit and net profit on the return account increased by 769.6% and 398.1%, respectively, compared to three years ago.

Undoubtedly, Biehenleven and HONMA golf have shown extraordinary ability to withstand risks and cross over a long period of time. However, the market is quite “stingy” in terms of valuation levels. The former has a dynamic price-earnings ratio of less than 20 times that of A shares (only 19.8 times), while the latter is only close to 10 times in the Hong Kong stock market.

There seems to be a big gap between the reality of long-term growth in the past and future growth expectations.

However, if you think about it a bit, you will get the answer: if a listed company (especially consumer stocks) can maintain a gross profit margin of 50% +, a net profit margin of 20-25% +, and an ROE of 15% + for a long time, its PE valuation can be at least 15 times or more under a single-digit revenue growth rate, and PB should not fall below 2.25 times.

Therefore, this company sells products in about 50 countries around the world and is owned by HONMA, the most famous iconic brand in the golf industry. Its listed company is more like buried gold. As to when will it change from “Don't Use Metal Gear Solid” to “Flying Dragon in Heaven”? You might as well take advantage of the release of a new financial report to track and dig again.

Profitability increased and net operating cash flow was abundant in the first half of the fiscal year

In recent years, in the face of a very challenging market environment, HONMA Golf has been steadfastly implementing its growth strategy. From the negative growth and restorative growth of the special environment in 2019-2022 to this year's steady growth, which emphasizes qualitative growth, these contexts can all be found in the changes in performance over the past few years.

In the first six months up to September 30, that is, the first half of the fiscal year, HONMA Golf achieved total revenue of 13.195 billion yen and net profit of 3,330 billion yen, an increase of 7.8% over the previous year. Correspondingly, HONMA Golf's net interest rate was 25.2%, an increase of 4.6 percentage points over the previous year. However, gross margin remained relatively high, at 52.1%.

During the period, the net operating cash flow generated by the company was 3,251 million yen, and the net operating cash flow/net profit was about 97.6%. This indicator shows that the profit realized by the company included most of the return of cash, which reflects the high quality of profit.

In the first half of this fiscal year, the company's inventory management was in place, and it also focused on the management of distribution channels and retail operations. The inventory on account was only 11.197 billion yen, which recorded a year-on-year and month-on-month decline. This is the first time since the same period in 2017 that inventory has declined month-on-month. The reduction in inventory is equivalent to saving on the use of cash. This is one of the reasons why the company received relatively good figures in terms of operating cash flow in the first half of the fiscal year.

In terms of categories, the growth momentum of golf apparel business continues to be stronger than golf clubs and products. During the period, HONMA Golf's global apparel business revenue increased 2.1% year on year. Among them, China's apparel business revenue increased 21.4% year on year. The reason for the good results is, on the one hand, that the company has launched a fashion golf series for young players since the second half of last year, and has also benefited from a shift in channel focus to self-management. In order to enhance brand awareness and fashion tone, during the period, HONMA collaborated with Japanese fashion designers to launch the HMG1959 capsule series and Bored Ape IP co-branded clothing series, which was very eye-catching.

During the review period, the performance of self-operated stores continued to be strong, with a steady increase of 13.2% year-on-year, mainly due to strong growth of 30.7% and 23.6% in Japan and China, respectively. On the other hand, revenue from third party retailers and wholesalers fell 22.5% year over year, mainly because HONMA continued to restructure its distribution strategy in North America and Europe during the period, reducing the number of dealer customers.

It can be seen that in the future, the focus of channel optimization and construction will come from continuously upgraded self-operated stores, so as to become the “main channel” for expanding retail business. Among them, Japan and China (market) may become key strategic bases for the high-quality operation of self-operated stores, thereby strengthening the company's many core advantages in the Asian market.

According to the announcement, as of September 30, the total number of HONMA Golf self-operated stores was 95, all located in Asia. These self-operated stores can all provide customers with a 360-degree experience of the HONMA brand and products. Self-operated stores were in the process of opening new stores in the first half of the fiscal year.

During the period, the revenue of self-operated stores was about 5.171 billion yen. Based on this, it can be deduced that the average store turnover was 54.43 million yen, equivalent to about RMB 2,614 million, and over 5 million yuan on a yearly basis.

In a horizontal comparison, this data is unquestionably in the leading position among chain golf sports brands.

However, compared to some popular and successful light luxury sports brands, the average annual sales volume of a single store (generally at the level of 8 to 10 million) is not very large. At the top, there is still potential for development. How to succeed in the industry and how to find key points can capture signals in subsequent direct-run store operations and performance improvement processes.

As far as the present situation is concerned, HONMA Golf is on a healthy upward path in the operation of its own stores, benefiting from the multiplier effect of the increase in the number of stores combined with the increase in the turnover of a single store. It's important to understand and recognize this. In the future, the author expects that HONMA Golf's revenue from its own stores may continue to be optimized, and that this portion of revenue will continue to increase.

Rooted in the ultra-high-end and ultra-performance segments

Summarizing the successful experiences of many light luxury sports brands, one point can be found that it is inseparable from the brand's professional success in the vertical field and integration with trendy design, technological innovation methods, etc. This is something I have always emphasized, and it is also one of the tricks that HONMA Golf can find and continue to strengthen.

The main reason why HONMA Golf is able to do well in the ultra-high-end and ultra-performance segments of golf is its craftsmanship — focusing on polishing club products that best represent Japanese craftsmanship and world-standard innovative technology.

The TOUR WORLD club family, which represents super performance, and the ultra-high-end BERES club family. These two major club product lines have always been the two “trump cards” of HONMA Golf, and these two major club product lines are still being refined to meet the development trend of the market and demand. For example, this year, HONMA added a swing enhancement club series for double penalty players to the TOUR WORLD club family, and upgraded the BERES club family, which is the most iconic in the ultra-high-end field, to adopt a modern and artistic face design and craftsmanship to meet the growing and diversified high-end needs of today's golfers.

Clearly distinguishing priorities and following the path of differentiation and specialization is one of the most prominent development characteristics that HONMA Golf has always adhered to. It is also the greatest motivation and ultimate reliance for the brand's development.

Using high-end, high-value core niche brand positioning to drive applications in larger, more, and more frequent scenarios (other than professional scenarios), such as popular casual trend products or extended expansion of business leisure product lines, this may explain the underlying logic of why HONMA Golf continues to adhere to and strengthen the “origin”, “ingenuity,” and “genetic” beliefs of its products.

As long as it can be confirmed that this remains the same, the core values of the brand have the necessary conditions for the “foundation” to survive.

Build an evergreen enterprise leading the global golf lifestyle

Earlier, the author showed the company's core competitive advantage, that is, the conditions and possibilities for the “foundation industry” to survive. Next, the author believes that the more important point is to prove whether HONMA Golf is an “evergreen” (sustainable) enterprise.

The reason an enterprise has the ability to achieve sustainable development is inseparable from the ability to continuously adapt to the changing environment and the ability to persist in innovation. Simply put, it means adapting and innovating.

In order to attract more young consumers in the Internet age, HONMA is committed to reinventing the brand into a dynamic, contemporary and international golf brand. The way to adapt is to reinvent the HONMA brand and create a 360-degree comprehensive brand experience.

For example, HONMA has redesigned its global website, reorganized social media platforms, and made frequent multimedia content updates on all electronic platforms to continuously increase the popularity and appeal of its brands and products among young golfers, thereby attracting a highly loyal group of young fans concerned about golf. These efforts have been increasingly accumulated, and the ability of the company's brand to monetize online has been enhanced, and in the end, significant growth in online revenue has been achieved. E-commerce sales increased 19.1% year over year in the first half of the year.

Additionally, HONMA employs leading design and marketing companies to refurbish its retail space with a view to providing customers with a high-end brand experience and a unique tailored consumer journey in core markets. In the first six months of September 30, 2023, HONMA Golf has used advanced technology to uniformly adopt new retail visual images, design concepts and consumer experience elements, and has opened 11 self-operated stores in China and the rest of Asia, respectively. In July of this year, HONMA's first central store in the city center of the country was opened in Taikoo Li, Chengdu; at the end of this year, the country's first “HONMA Home” brand flagship store will also be unveiled in Xintiandi, Shanghai. At that time, a HONMA lifestyle space integrating brand display, full product experience, and high-end customized service experience will bring a new style of golf lifestyle.

ending

Finally, returning to the capital market, HONMA Golf's desire for sustainable development may also be reflected in the stable dividend strategy it has adhered to over the years and continued to reward shareholder actions. Since going public at the end of 2016, the company's cumulative number of dividends has reached 14 times over a period of more than 7 years. Basically, it is a dividend distribution habit twice a year. In the just-released results announcement for the first half of the fiscal year 23/24, the board of directors of HONMA Golf recommended paying an interim dividend of 1.5 yen per share, with a distribution ratio of about 27.3%. This ratio is also higher than the 23.5% announced by Bieinleffen in the 22nd annual report.

May I ask, how can a professional sports brand with core competitive advantages and sustainable development, and continue to actively promote upgrading and reshaping fall into a “value trap” investment type where value is constantly being depreciated. Once this possibility is ruled out, then the valuation correction or value return to the market due to the large underestimation of HONMA Golf is only a matter of time, starting from general sense.

However, time and long-term principles will ultimately prove that the brand has always adhered to the correctness of the route. It is also time that has made HONMA Golf stand more and more on the favorable side.