Authors: Ren Zeping, Fang Siyuan

Events:On January 13, 2018, the CBRC issued the Circular on further deepening the rectification of chaos in the Banking Market (document No. 4 of the Banking Regulatory Commission (2018)). On the basis of the initial results achieved in the "March 30-40" special project in 2017, it is required to continue to promote the rectification of the banking market chaos, and the document clearly defines the specific work arrangements and requirements of the late-stage chaos rectification work, the relevant work opinions, and the main points of the work.

Interpretation:

1. Overall judgment: supervision has changed from the "30-40" inspection and self-examination stage to the key rectification stage. Defining the key points, establishing the system, returning to the origin and normalizing supervision are the work orientation.

(1) the Central Economic work Conference set the tone that preventing and defusing major risks is the first of the three major battles, document No. 4 reflects the determination of concrete implementation, and supervision has changed from the stage of "30-30-40" inspection and self-examination to the stage of key rectification.On the basis of the preliminary achievements made in the "March 30-40" inspection, the supervision issued another comprehensive rectification notice, reflecting the regulators' determination to thoroughly rectify the financial risks, and the illegal practices that still have the mentality of fluke will be strictly punished by supervision. This article No. 4 focuses on the key points and solves the pain points on the basis of the "3-3-40", reflecting that financial chaos rectification has entered the second stage.

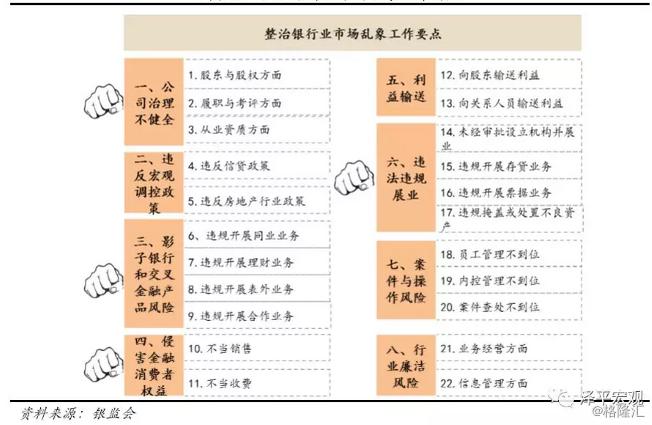

Specific operation, clear 2018 focus on the banking market chaos in 8 aspects 22: first, corporate governance is not sound, including shareholders and equity, performance and evaluation, employment qualifications and other three aspects. Second, it violates macro-control policies, including credit policies and real estate industry policies. The third is the risk of shadow banking and cross-financial products, including the illegal development of inter-bank business, financial management business, off-balance sheet business and cooperative business. The fourth is to infringe upon the rights and interests of financial consumers, mainly improper sales and improper charges directly related to the rights and interests of financial consumers. Fifth, the transfer of benefits, including the transfer of benefits to shareholders and related personnel. Sixth, illegal exhibition industry, including the establishment of institutions without examination and approval, illegal deposit and loan business, illegal bill business, illegal cover-up or disposal of non-performing assets. The seventh is the case and operational risk, mainly enumerating the weak links and outstanding problems in some cases, including inadequate staff management, inadequate internal control management, and inadequate investigation and handling of cases. Eighth, the risk of industry integrity, including business operation and information management. In addition, there is a separate list of negative aspects of regulatory performance.

(2) the supervision document clearly proposes to form a long-term mechanism and regular supervision of "rectification-evaluation-rectification", cultivate a compliance culture in which banks "cannot break the rules, dare not break the rules, and are unwilling to break the rules", and squeeze the space for regulatory arbitrage.More detailed requirements for the responsibilities of regulators are put forward, and it is expected that the situation of loose and soft policy implementation and large regional differences will no longer exist, supervision will be unified, and the space for regulatory arbitrage will be greatly squeezed.

(3)“We will focus on interbank, financial management, off-balance sheet business and shadow banking in 2018, and continue to promote deleveraging, deleveraging and chain deleveraging within the financial system. " Shadow banking and cross-financial risks are the key direction of this round of rectification and reform.Its complex trading structure, long chain and risk accumulation are the directions that the current round of supervision needs to focus on.It is reiterated that getting rid of emptiness to reality and serving the real economy is the key goal, and it is a deterministic trend for banks to return to the main business in order to form a virtuous circle within the financial and real economy, financial and real estate, and financial systems.

(4) the idea of strong supervision since 2017 shows that the traditional commercial banks have lost the room for production by increasing the scale of their assets and liabilities and making false innovations and idling business models. Only when financial institutions actively adjust the capital flow and return to real enterprises is the correct way of thinking in line with the national policy.

(5) preventing and defusing major financial risks and returning to the origin of serving the real economy is an inevitable requirement for promoting high-quality development in the new era. it is an important part of the supply-side structural reform of "eliminating production capacity, removing inventory, deleveraging, reducing costs and making up for deficiencies".

Since the "three cuts, one decline and one supplement" was put forward at the Central Economic work Conference in December 2015, remarkable progress has been made in capacity removal and inventory removal in 2016-2017. deleveraging, cost reduction and replenishment have been put on the agenda in the second half of 2016 as the economy bottomed out and stabilized. We believe that the five major tasks of supply-side structural reform put forward by the Central Economic work Conference in December 2015 is one of the landmark events that have opened a new political and economic cycle. it has not only found the crux of China's economic problems, but also found the correct solution. what is more important is that the ability of organization and mobilization has been greatly enhanced after 2015, ensuring the executive power of "scratching iron, stepping stone and leaving imprints for a long time."

Therefore, we should look forward to the process and results of the three major battles of "preventing and defusing major risks, accurate poverty alleviation, and pollution prevention" in 2018 on the basis of the policy determination, implementation and final results of capacity elimination and inventory elimination from 2016 to 2017. Give full attention and confidence.

Second, the background of the launch: the 3-3-4 inspection has achieved preliminary results, and preventing and defusing major risks is a key battle.

Since the beginning of 2017, under the direct influence of a number of large risk events, based on the judgment of the existence of macro systemic risks, the CBRC has successively issued some supervision documents of great powers, such as "three arbitrage", "three violations", "four improper" and "rectification of inter-bank chaos", to guide the banking industry to return to its origin, prevent and control risks, and improve the quality and efficiency of serving the real economy. The field of supervision affects almost all mainstream transactions, such as bills, financial management, peer-to-peer trading, and so on, and the inherent logic of behavior also goes deep into deep-seated problems such as transaction mode, accounting subject setting, internal and external cooperation, personnel management and so on. After nearly a year of implementation, the chaos in the banking market has been rectified to a certain extent and phased results have been achieved:

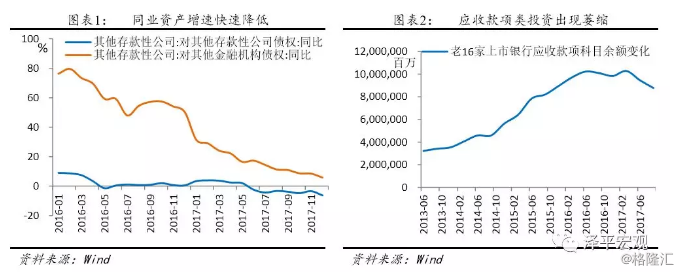

(1) The growth rate of interbank leverage has dropped sharply.The claims of other depository companies to other depository companies and other financial institutions can be used as a reference index to measure the leverage of the same industry. Since the beginning of 2017, the year-on-year growth rates of the two indicators have declined rapidly, with the year-on-year growth rate of claims on other financial institutions falling from nearly 80 per cent at the beginning of 2016 to 6 per cent at the end of 2017, reflecting that the regulatory storm in early 2017 has played a significant role in restricting the expansion of peer leverage.

(2) Report data returns to reality:At the beginning of this wave of inspection, commercial banks will constantly move the data of the subjects to be inspected, and the investment of accounts receivable has once become a safe haven for all kinds of assets. With the deepening of regulation, the data on the subject also shrank after 2017. It can be seen that another positive result caused by the inspection is that the report data gradually return to the truth, and the process of regression is also a process in which leverage is reduced.

(3) A wide range of penalties for institutional violations:According to the administrative penalty information on the official website of the CBRC, more than 2700 fines have been issued by the banking supervision system since 2017, with a total fine of nearly 3 billion yuan. From the perspective of the industries involved, bills, bonds, financial management and other areas have been affected, the determination of regulatory punishment is evident.

However, market chaos still exists in varying degrees, some financial institutions commit crimes against the wind, systemic financial risks have not been completely eliminated, and system construction has a long way to go.The Qiaoxing case, the Hengfeng equity case, the agency repurchase case and the newly issued Heilongjiang financial management case are almost all typical examples of still issuing secrets, abnormal equity changes, private carving of radish chapters, and private contract changes at the forefront of the storm. It can be seen that the implementation of the system itself still needs to be deepened, and it is necessary for supervision to develop in depth. In order to further implement the relevant requirements of the CPC Central Committee, strictly abide by the bottom line that systemic financial risks will not occur, and further rectify the chaos in the banking market, on the basis of the inspection and summary in 2017, the notice on further deepening and rectifying the chaos in the banking market was launched.

Third, this round of supervision is compared with the "3-30-40": sum up and clarify the key points

(1) the content is more prominent, and the case is abstracted into a system and popularized.

Different from the "3-30-40" supervision guided by business investigation, document No. 4 of the CBRC integrates the main contents of previous special rectification and summarizes the problems found since last year's inspection and the latest risk exposures, highlighting the focus of the work. It can be said that it is another abstract theoretical summary of various cases, in order to further guide the new inspection. For example, the Banking Supervision Bureau of Heilongjiang Province announced earlier this month that it had investigated and dealt with six public financial management incidents of 5.47 billion yuan under the jurisdiction of ICBC in Heilongjiang Province in accordance with the law. The punishment shows that most of the institutions under the jurisdiction of ICBC are involved in illegally modifying the version of the financial management contract. Considering that the matter must be reported to the CBRC in advance, we believe that the fourth major point in the work of rectifying chaos is that the provisions on infringing upon the rights and interests of financial consumers (especially improper sales) have been affected by this incident.

(2) the requirements are more specific: there is no gap period in the business, and the main responsibility is more clear.

This rectification is more specific than the previous special action, which not only clearly mentions the demarcation of new and old business, but also clearly defines the respective responsibilities of the main body of operation and supervision. The seventh point of the rectification opinion points out that the new business after May 1, 2017 shall be regulated in strict accordance with laws and regulations and investigated and dealt with in accordance with the law. This is actually warning commercial banks not to take chances and attempt to take advantage of the gap period to increase their positions. The sixth and eighth points also explain the implementation of subject responsibility and the performance of regulatory responsibility. Banking financial institutions need to implement the main responsibility of chaos rectification, and the respective responsibilities of the party committee, discipline inspection commission, board of directors, chairman of the board and senior management have been clearly defined. For the regulators themselves, it is required to adhere to the "supervision surname supervision", in accordance with the law, strict, clean, comprehensive, scientific and targeted. We must insist on strict enforcement of the law and prosecution of violators. Discipline inspection and supervision departments at all levels should also earnestly play a supervisory role.

IV. Regulatory keynote: meet normal regulatory expectations, resolutely promote policy implementation and accountability in place

The notice of the CBRC No. 4 on further deepening the rectification of chaos in the banking market is mainly divided into three parts:Notification bodyMainly deploy the rhythm of future regulatory promotion; annex I"opinions on further deepening the rectification of chaos in the banking market"The ten opinions set the tone and focus for the CBRC to rectify market chaos this year and in the future. Annex II"the main points of the work to rectify the chaos in the banking market in 2018"It is mainly the main points of the work to promote the rectification.

Among them, the "opinions" have defined 10 directions, and we believe that they have established the general tone of this round of supervision and the future regulatory trend. We have summed up the 10 directions into five points, namely, the overall tone, the direction of regulation, the implementation of responsibilities, regulatory principles, and long-term mechanisms:

1. The overall tone first puts forward the long-term nature of future supervision, which gives banks the expectation of regular supervision, and then determines the overall goal of bank chaos regulation, that is, curbing violations of laws and regulations, breaking away from reality, focusing on the main business and cultivating a compliance culture.

1) Raise awareness:The "opinion" proposes in relatively severe terms that it is necessary to fully understand that rectifying market chaos is an important part of preventing systemic financial risks, and requires that we recognize the long-term nature, complexity, and arduousness of rectifying banking market chaos. We believe that the purpose of the opinion is to set good expectations for future supervision. Banking chaos rectification is not done after inspection, nor can it be achieved overnight, but that strict supervision should be carried out in the future and a long-term regulatory mechanism should be established. put an end to all kinds of business chaos in the banking industry for a long time.

2) Define your work objectives:Identify the four key work objectives in the future in terms of work objectives.They are to curb violations of laws and regulations, to promote the return of funds to entities, to continue banks to focus on the main business and differentiated development, and to cultivate a culture of compliance and sound operation.In the No. 4 document of the CBRC and in answering reporters' questions, they all reiterated that it is necessary to promote the return of funds to entities, to prevent them from becoming unreal, and to form a virtuous circle within the financial and real economy, financial and real estate, and financial systems. In the combination of opinions, it is clear that banks continue the trend of focusing on the main business and differentiated development, and the supervision is very firm in the attitude of returning to the origin and sound operation of the banking industry in the future. at the same time, it also respects the differential development of banks, and banks with operating characteristics are in line with the regulatory trend.

2. In terms of the specific direction of rectification, it is no longer as comprehensive as it was during the "30-40" investigation, but to grasp the key points and solve the pain points on the basis of "30-40", reflecting that the banking mess has entered the second stage; while shadow banking and cross-financial risks are still the focus of regulation.

3) Deepen the problem orientationIt is pointed out that to adhere to the key treatment of "targeted" therapy, it is necessary to find and solve problems as the starting point.

4) Highlight the key points of regulation: the basis is to improve corporate governance, focusing on shadow banking and cross-financial product risks, focusing on legal management, and the key is to protect the rights and interests of financial consumers.Opinions through this article to make clear the focus of this round of supervision, we can see that shadow banking and cross-financial risks are still the focus of this round of supervision, and the related business complexity and system design still need to be further improved and supplemented.

5) Strictly investigate the risk of the caseIt is required to seriously investigate and deal with banking cases and major risks, as well as serious accountability.

3. In terms of the implementation of the principal responsibility, in addition to the board of directors, senior management and the board of supervisors of the business subject, it is required to strengthen the implementation of the responsibility of the party committee and the discipline inspection commission for inspection, reflecting the determination of supervision to thoroughly implement the business renovation and put the accountability in place.

6) To implement the principal responsibility:Requires the party committee to strengthen the leadership of the party throughout the process; the Commission for discipline Inspection to strengthen accountability, solve the internal accountability is a mere formality, deal with superficial; the board of directors bear the ultimate responsibility, senior management bear the responsibility of implementation, the board of supervisors fulfill the responsibility of supervision.

4. Put forward three major regulatory principles, focusing on preventing the emergence of "risk management risks", which is consistent with the principles of financial supervision since last year; in addition, it is proposed to fulfill regulatory responsibilities and form a joint force of supervision. more detailed requirements for the duties of regulators are put forward. it is expected that in the future, the situation of loose and soft policy implementation and large regional differences will no longer exist, and the intensity of supervision will be unified.

7) Grasp the rhythm of strength:It is required to persist in making progress in the midst of stability and guard against the "risk of dealing with risks"; cut off between the new and the old, the stock business will be given digestion and transition periods, and the new business after May 2017 will be investigated and dealt with in accordance with the law; self-inspection and self-correction will be lenient, and supervision will be found to be strict. It is worth noting that this document proposes to give a digestion period and a transition period for the stock business, while the new business after May 2017 was investigated and dealt with in accordance with the law, but no transition period was given. We think this is actually stricter than expected. At the same time, it also reflects that the supervision has taken a very strict attitude towards the illegal operation after the 30-30-40 investigation last year. Some of the small and medium-sized banks that do not comply with the rules and face the wind and waves may face greater pressure.

8) Perform regulatory duties:Adhere to the surname of supervision to form a serious regulatory atmosphere; require comprehensive supervision to make up for the blind areas of supervision in a timely manner; focus on solving the problems of inadequate accountability, looseness and softness, and large regional differences.

9) To form a joint force of regulation:Bring institutional supervision, functional supervision, banking supervision bureaus, discipline inspection departments at all levels, inspection departments at all levels, financial management registration and trusteeship centers, banking credit assets registration and transfer centers, trust registration companies, etc. into the scope of joint supervision, we will resolutely promote the landing of supervision.

5. It requires the establishment of a long-term mechanism, which points out the direction for the future regulatory development of the banking industry: the banking industry should form a culture that does not dare to break the rules, supervision should further make up for the regulatory deficiencies, and it is expected that the regulatory measures to make up for the deficiencies of the banking industry will be further implemented this year.

10) establish a long-term mechanism: the banking industry: form a compliance culture of "do not violate the rules, dare not break the rules, and do not want to break the rules"; regulators: further make up for the shortcomings of the regulatory system and effectively solve the problems of the system and mechanism that cause chaos. During the "30-40" inspection last year, the "notice on effectively making up for regulatory deficiencies and improving regulatory efficiency" has clearly defined the next key work items to take over to make up for deficiencies, namely, development category, promotion category, and research category. Up to now, 6 documents have been issued and 5 documents have been solicited from the public. It is expected that under the guidance, the landing progress of various deficiencies this year will be further accelerated.

V. Regulatory points: shadow banking and cross-financial risks are the key direction, and the principle of protecting investors is consistent.

In Annex II of document No. 4, "the main points of work to rectify the chaos in the banking market in 2018", the specific key points of regulation and promotion of 8 major items and 22 minor items are clearly defined. To examine the specific content, we believe that it is generally the summary and refinement of the "30-40" inspection, as well as the abstract summary of recent risk cases, with basically no new or higher-than-expected direction. After an item-by-item investigation of the regulatory storm in the first half of 2017, the CBRC summarized the key points of chaos rectification into eight key points: (1) imperfect corporate governance; (2) violation of macro-control policies; (3) shadow banking and cross-financial product risk; (4) infringement of the rights and interests of financial consumers; (5) transfer of benefits; (6) illegal exhibition; (7) case and operational risk; (8) industry integrity risk.

Combined with the four key points put forward in the guidance of document No. 4: the basis is to improve corporate governance, the focus is on shadow banking and cross-financial product risks, the focus is legal operation, and the key is to protect the rights and interests of financial consumers. We focus on the regulatory logic in these four areas.

(1) Continue to rectify the imperfect corporate governance.Corporate governance, as the basic direction of financial chaos, is an area that the CBRC has been emphasizing and strengthening supervision since the "30-30-40" inspection. This round of supervision re-emphasizes the inventory and rectification of illegal contents such as shareholder qualification, shareholder false capital contribution, proxy, benefit transfer and so on.On January 5, 2018, the CBRC has formally issued the interim measures for the Administration of Equity in Commercial Banks to comprehensively supervise the above violations. It is expected that in the future, whether in the primary or secondary market, the investment of bank equity, especially the issue of agent ownership, will penetrate to the actual controller and be strictly regulated.

(2) The risk of shadow banking and cross-financial products is still the focus of regulation, and the definition of standardized assets will continue to be observed in the future. Shadow banking and cross-financial products have long chains, complex structures, various transaction designs, easy to hide risks, or bypass regulatory indicators through structural design.Although the growth rate of the claims of other deposit companies to other deposit companies and other financial institutions has slowed significantly since the regulatory storm in the first half of 2017, the guidance continues to focus on shadow banking and cross-financial products, reflecting the complexity and arduousness of the rectification.

To sum up, for shadow banking and cross-financial business, this round of supervision still focuses on breaking through regulatory indicators in disguise, hiding underlying assets, inability to penetrate capital sources, invisible guarantee, risk-free isolation of self-management and financial management, capital pool, undesirable investment and other traditional directions.Among them, in the illegal development of off-balance sheet business, it is proposed that "take credit assets or asset management products as basic assets, through specific purpose carriers by means of packaging, layering, share sales, etc., to issue asset securitization products in places other than the interbank market and the stock exchange market, so as to achieve the unclean statement of assets and reduce capital withdrawal", combined with the fuzzy definition of standardized products in the recent draft of the new regulations on asset management. It remains to be seen how the transaction structure is designed and what kind of circulation platform can be defined as a standardized product in the future.

(3) To strictly prevent the infringement of the rights and interests of financial consumers and protect investors is an important direction for the future development of the asset management industry.In the part of infringing on the rights and interests of financial consumers, the regulatory chaos mainly includes the sale of unapproved products, unauthorized change of contracts, consignment of non-compliant products, improper sales, misleading customers, compulsory bundling and improper charges. In the early stage, all kinds of cases such as "financial flyer" and illegal sales have seriously infringed upon the rights and interests of consumers, caused extensive social impact, impacted the social image of banks and other financial institutions, and touched the red line of supervision. Combined with the provisions for the protection of investors in the previous draft of the new regulations on asset management, we believe that the future asset management industry through laws and regulations to protect and cultivate investors is an important direction.

(4) Strictly control illegal exhibition and establish a compliance culture.In the part of illegal exhibition industry, the main contents of supervision and regulation include setting up institutions without examination and approval, carrying out deposit and loan business in violation of regulations, carrying out bill business in violation of regulations, covering up or disposing of non-performing assets in violation of regulations, and so on, which basically match the investigation of "30-40". Combined with the guiding direction of the 10 opinions, the focus of chaos rectification is compliance operation, and it is expected that in the near future, it will continue to strictly punish and implement accountability for violations in accordance with the law; in the long run, supervision aims to create a compliance culture that "cannot break the rules, dare not break the rules, and is unwilling to break the rules."

VI. Promotion of supervision: the formation of regular supervision of "rectification-evaluation-rectification"

In terms of supervision and promotion, the circular clearly defines four requirements, namely, comprehensively carrying out evaluation work, comprehensively promoting all kinds of work, effectively standardizing all kinds of reports, and seriously punishing and accountability in accordance with the law. The node set in the first batch of reports is March 10, 2018, which is mainly aimed at the evaluation of the special governance work that has been carried out in 2017, while phased work reports will continue to be submitted in June and December 2018 to form a regular self-examination and regular "rectification-evaluation-rectification" work model, which aims to thoroughly rectify and standardize the operation of banks.

VII. The enlightening significance of supervision: adapt to the new rules and seek opportunities in compliance.

The idea of strong supervision since 2017 shows that the traditional commercial banks have lost the room for production by increasing the scale of their assets and liabilities and making false innovations and idling business models. Only when financial institutions give up the fluke heart and actively adjust the capital flow to return to the real enterprises is the correct way of thinking in line with the national policy.

(1) maintain moderation and truthfulness around the core of "capital".

The transposition of "capital" should become the driving force rather than an obstacle for commercial banks to adjust their asset-liability strategies. Business innovations for the purpose of avoiding and reducing capital consumption, such as off-balance sheet financial management, bill portfolio transactions, and fake lists of interbank investments, all take advantage of regulatory loopholes, making the business itself dissociated from the monitoring system and difficult to supervise. In fact, the superficial capital adequacy can not cover the real credit risk, market risk and operational risk. Only by truly classifying according to the risk degree of the business itself and accurately calculating the capital, can commercial banks keep their business in a relatively safe range. In the future, if regulators can use information technology to solve the problem of full chain and highly transparent flow of all kinds of non-standardized bond assets, then the capital problem can be effectively monitored by adjusting high-risk weighted assets to low-weight assets or asset fake transfer. Market risk can be maintained at a controllable level.

(2) the transformation from "industry" to "enterprise".

Previous inspections in recent years show that the areas with high amount, many problems, high risk and high outbreak frequency are mainly concentrated in the "big industry fields", such as financial management, trust, bills, bonds, interbank investment and so on. Based on the endorsement of interbank credit, this field continues to use borrowing, repurchase, certificate of deposit, deposit and off-balance sheet financial funds for leveraged expansion, and then flows into restricted, high-risk-weighted industries. After the local risk exposure, the industry chain is broken, which leads to a major market credit crisis. At the same time, the inter-industry expansion of liabilities and assets also greatly improves the level of market leverage and weakens the regulation and control effect of national monetary policy, and its hidden systemic risk far exceeds the crisis of real enterprises. This wave of high-intensity inspection of a number of documents have taken the industry as the focus of regulation, and the result of deleveraging and deleveraging must be the gradual decline of the era of the industry. Commercial banks can save themselves only by changing the mode of relying heavily on their peers for revenue before 2015, responding to national policies, and improving the regenerative capacity of the whole market through "blood transfusions" to enterprises.

(3) cancel the authorization to the branch office and realize the complete monopoly.

With the outbreak of interbank risk after 2014, according to the requirements of document (2014) 140, the vast majority of commercial banks in the market have achieved varying degrees of interbank monopoly. However, based on the fourth point of article 140, "the commercial bank interbank business franchise department can not conduct electronic transactions through the financial transaction market, we can entrust other departments or branches to act as agents for operational matters such as marketing and inquiry, project initiation and customer relationship maintenance." in the market, many banks hand over the interbank business that should have been concentrated to branch marketing. Under the premise of the sharp increase in market risk, the intervention of too many branches gives opportunities to illegal participants such as market intermediaries. If the monopoly can be carried out thoroughly and the head office is responsible for it, then the risk issues such as private trading with the same business will be controlled in a small range, and its moral hazard can also be better controlled.

(4) redesign the incentive and assessment mechanism.

Profit-seeking is the origin of enterprises, but excessive incentives and assessment, not only can not promote commercial banks to move forward steadily, but also may hide greater risks. All the assessment models of commercial banks centered on deposits, loans or performance income help to increase the cost of capital in time and stimulate the occurrence of moral hazard to a certain extent. Only through the scientific redesign of the incentive and assessment mechanism to reduce excessive stimulation, can we fundamentally solve all kinds of problems caused by the profit of "people". The minor problems of people's livelihood, the contraction of community banks and the Hengfeng equity case are all the risk problems caused by improper incentive and assessment mechanism. If such issues are not guided, the degree to which regulatory policies will be implemented will be reduced.

(5) to adapt to the new rules and find a new way out from the compliance system.

In the context of a stricter regulatory environment, if financial institutions try to go against the current in order to evade supervision to expand their business, it is not only likely to increase market risk, but also face very serious regulatory penalties. This wave of inspection is not only a challenge, but also an opportunity. As a result, the abnormal business model is about to be cleared, and the vitality of the participants who can learn and apply the new rules will be greatly enhanced.

Risk hint: supervision is stronger than expected.

(official account of the author: Zeping Macro)