Source: Wall Street News

The real horror is the interference with market liquidity. If capital flows back from US debt to the Fed's reverse repurchase and the Fed's QT, liquidity will be quickly drained, and market demand for risk and safe assets will decline rapidly.

The US debt situation may be far less optimistic than the market thinks!

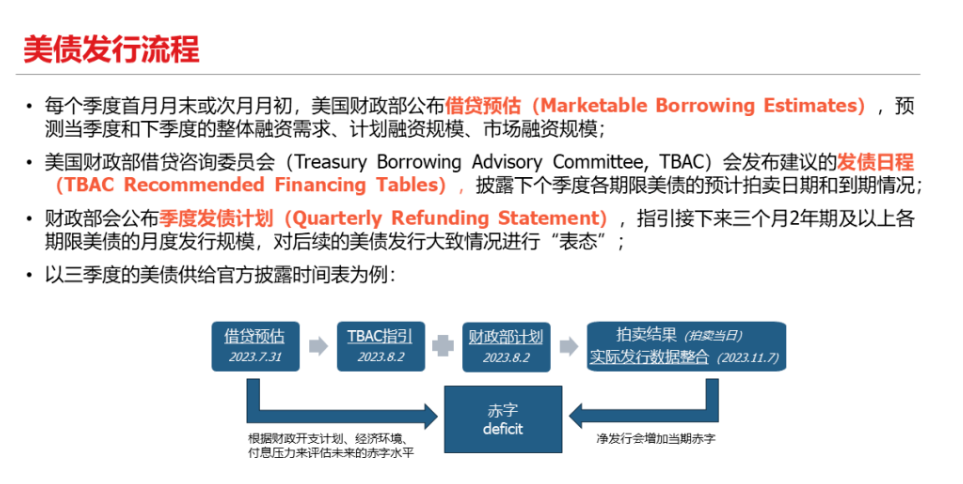

Last week, the US debt issuance plan for the fourth quarter was settled. The US Treasury Department announced that in the fourth quarter of this year from October to December, it expects the federal government to borrow 776 billion US dollars, down 760 US dollars from the 8520 US dollar forecast at the end of July. The reduction in supply shocks is compounded by the Fed's suspension of interest rate hikes once again. Many analysts are optimistic that the inflection point of US debt has arrived.

However, according to the latest analysis by the media and Goldman Sachs, the US Treasury's slowdown in debt issuance in the fourth quarter was guiding market expectations, and it is expected that the scale of debt issuance will remain high in the future.

Under the issuance of Tianliang bonds, the market is facing many challenges. From the demand side, the Fed is implementing quantitative austerity policies, which the private sector alone may be unable to digest; from a further perspective, the real horror is the interference with market liquidity. If capital flows back from US debt to the Fed's reverse repurchases and the Fed's QT, liquidity will be quickly drained, and the market demand for risk and safe assets will drop sharply.

Slowing down debt issuance? The US Treasury is just diverting market attention

According to media analysis, the current US Treasury bond issuance plan is actually just “imitating the Federal Reserve” to guide market expectations and divert market attention.

Specifically, although the US Treasury slowed down debt issuance in the fourth quarter, it indicated that the scale of debt issuance will increase in the future:

According to the predicted medium- to long-term loan demand,The plan is to “gradually” increase the size of most bond auctions in the quarter from November 2023 to January 2024, and it is expected that the scale will need to be increased by another quarter after thatto meet its financing needs.

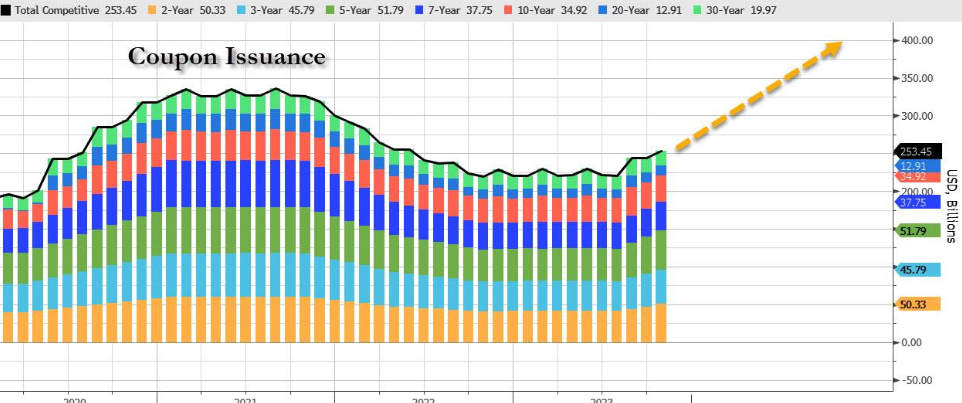

As can be seen from the chart below, after the scale of long-term bond issuance declined slightly in 2022, the volume of long-term bonds issued rose again, and is likely to continue indefinitely. Because looking forward to the future, the total amount of US bond issuance regulations will be huge. According to the US Congressional Budget Office (CBO) forecast, in the long run, the share of US debt in the US GDP may rise from 120% now to 200%.

However, the US Treasury Department offered a “delay plan” -- less long-term debt, more short-term US debt,The aggressive short-term US bond issuance frenzy brought its share of tradable debt to 20.4%, higher than the 15-20% range proposed by TBAC, although TBAC stated that short-term US debt “under reasonable assumptions, is expected to remain above 20% until the second quarter of 2025.”

TBAC refers to the US Treasury Loans Advisory Committee, a group composed of major participants in the bond market, such as Citibank, J.P. Morgan, and BlackRock. They are responsible for providing debt issuance advice to the Treasury.

TBAC also expressed concern about the supply of US debt. In its report to the US Treasury, TBAC stated:

The large and continuing deficit has fueled expectations of a significant increase in the supply of bonds;

With the exception of periods of economic recession/high unemployment, the US deficit is at the upper end of its range, which makes the supply of US bonds the focus (the recent rise in US bond yields is mainly due to rising term premiums);

The narrowing of swap spreads may once again indicate an imbalance between supply and demand due to an increase in the issuance of US bonds.

The wording adjustments also followed TBAC's suggestions. TBAC clearly stated in its report that in August, after the Ministry of Finance issued the wording “it may be necessary to further gradually increase the issuance scale in the next few quarters,” 10-year US Treasury yields rose sharply.Therefore, the Ministry of Finance adjusted the wording in the November report to “increase the scale for one more quarter.”

TBAC explained that if the Treasury maintains the growth pattern announced in August for the next two quarters, it would indicate:

The supply of US Treasury bonds will set a new record, which will significantly increase the long-term supply of treasury bonds next year.

The analysis points out that the Ministry of Finance's wording “one more quarter” will help delay the onset of a disastrous time.Yellen actually did not emphasize the Treasury's reliance on long-term debt, but instead tried to shift attention to short-term US bond issuance and the Fed's reverse repurchase mechanism. Most people expect this mechanism to be the source of funding for all short-term US bonds until the Fed's reverse repurchase balance is exhausted.

Facing Tianliang Bonds, the Private Sector Is Unbearable

From the demand side, the Federal Reserve is implementing quantitative austerity policies, and the private sector may not be able to absorb the huge amount of bonds.

First, Tier 1 traders (that is, banks that buy bonds at auctions and then market the bonds) are the key to the US bond issuance system.

And as the volume of debt issued surges, they are buying more US bonds than they can sell. As a result, the yield on US bonds maturing for 10 years or more has risen from higher than the yield on swap transactions (that is, swap spreads have narrowed). However, traders originally hedged bond price risks through swap transactions and earned the interest rate difference between the two. Thus, there is no reason for Tier 1 traders to bear large amounts of US debt. Therefore, it is reasonable for the US Treasury to reduce the issuance of long-term bonds,Currently, the cost of borrowing 30-year US bonds is 0.6 percentage points higher than swap interest rates.

Another problem is that financial regulation after the 2008 financial crisis prevented banks from absorbing bonds without restrictions. The Fed's quantitative easing policy made up for this shortcoming, but this is no longer the case; the Fed is actively selling bonds to carry out quantitative tightening.

Second, less regulated participants — hedge funds, US Commodity Futures Trading Commission (CFTC) data show that leveraged funds' net short positions on US Treasury futures rose to the highest level since 2006, probably because they acted as traders by buying treasury bonds and selling treasury bond futures.

However, as the Bank for International Settlements warned in a September report, this is a risky deal that could soon unravel. In March 2020, when the pandemic raised risk concerns, US bonds were instead sold off。 This proves that although people expect safe haven assets to appreciate in times of trouble, funds and traders have reduced leverage ratios to have the opposite effect.

The above situation shows that the private sector may not be able to provide as much liquidity to the bond market as implied by official financial plans.

Further, historically, the positions of US traders are negatively correlated with the steepness of the US bond yield curve, which means that only when bond yields greatly exceed the yield of depositing cash in banks will such buyers step in. This situation has already begun to occur: Overwhelmed traders price long-term bonds at discounted prices, which has led to an increase in “term premiums,” leading to higher borrowing costs and pressure on stock markets, and term premiums are likely to rise further in the future.

The real black swan: market liquidity “instantaneously” evaporates

The analysis points out that compared to weak demand, interference with market liquidity is the real “black swan.”

As TBAC points out, since June 1, the US Treasury has issued $1.5 trillion in US Treasury bonds to meet borrowing needs and rebuild the TGA from a lower level. (Simply put, TGA is the “wallet” of the US federal government. US treasury bond issuance and tax revenue are remitted to this account, and almost all expenses of the US federal government are also remitted through this account)

However, most of this cash does not come from bank balance sheets, but from the more than 1 trillion US dollars stored in reverse repurchases with the Federal Reserve. With the US bond issuance/the explosive growth in Treasury cash, the total amount of reverse repurchases by the Federal Reserve has shrunk sharply.

Looking at the relationship between “ON RRP, short-term US debt, and TGA cash”, the following chart shows that for most of the second half of this year, every dollar raised from issuing short-term treasury bills and used to supplement the TGA account came from the Federal Reserve's reverse repurchase mechanism, and as TGA account capital continued to rise, the Fed's reverse repurchase balance was being exhausted little by little.

Looking further, long-term bonds are different from short-term US bonds. Currently, there are no reserve limits. Theoretically, as long as the reverse repurchase capital is sufficient, they can be sold without any market problems. However, although there is currently sufficient capital for reverse repurchases, it is also rapidly being consumed: as of November 7, the scale of use of the Fed's overnight reverse repurchase agreement (RRP) was just over 1 trillion US dollars, down 1.5 trillion US dollars from the peak on December 30 last year. At this rate, the most important reverse repurchases — a seemingly endless source of liquidity — are likely to run out completely in January.

As Goldman Sachs strategist Borislav Vladimirov pointed out in his report:

The US Treasury's shift to more reliance on issuing treasury bonds to fund the US deficit has caused interest rates on short-term US bonds to be higher than PPR interest rates, while higher returns continue to attract investors to transfer capital from ON RRP to undertake short-term US bonds, which has also led to the decoupling of US bonds from risk assets.

As money market capital shifts from ON RRP to short-term US debt, this has taken about $80 billion in liquidity from the Fed's overnight reverse repurchase agreement (RRP), while also offsetting some QT's impact on market liquidity.

Borislav Vladimirov believes that the problem lies in:

If the volume of US bond issuance declines and the correlation between US bond yields and risky assets normalizes, we may see capital reversal back to ON RRP in a short period of time. Coupled with the Fed's QT, this may cause reserves to quickly reach the upper limit level.

In fact, Goldman Sachs believes this development is likely to trigger significant risk parity fluctuations and dollar fluctuations, leading to the third phase of the R** event, forcing the Fed to immediately relax its policy and stop quantitative easing.

It is worth mentioning that the Federal Reserve can prevent liquidity fluctuations in advance by setting an RRP upper limit. This will suppress short-term US bond yields in a risk-averse environment, keep bank reserves in line with quantitative easing, and put some downward pressure on short-term US bond yields. Therefore, the RRP limit will benefit risky assets in the short term.

The media concluded that currently, the Fed's reverse repurchase balance is being exhausted. As with the overall financial conditions of the market, the RRP operation had a similar reaction. Once the Fed seems to have let go of its hawkish footsteps and the market starts to binge, it will force the Fed to become more hawkish. If the continued reduction of RRP operations is considered to have adverse consequences for the market, then the flow of capital in the market will be reversed immediately.

Well, it is possible that in just a few weeks, the Fed's reverse repurchase balance will rise sharply, short-term US bonds will be sold off in the open market, and cash will be stored in a safe warehouse with “the Fed as a counterparty.”This means that market liquidity will evaporate instantaneously, and market demand for risk and safe assets will drop dramatically.

Editor/Somer