According to the saying that "post-80s are already elderly", it is time for "post-90s" to think about buying an insurance.

The tradition of buying insurance for unknown risks has a long history, dating back to 2000 BC. In order to avoid the destruction of ships and goods, businessmen sailing in the Mediterranean often sell part of the goods, and the losses are shared by all parties, thus forming the average sharing principle of "one person for all, everyone for one person".

George, a businessman from Genoa, on October 23, 1347. Leckvinen issued his first voyage insurance policy. Today, the insured has changed from cargo to people, flight times, and even the long legs of Victoria's Secret models. Whether it is social security in the mainland or corporate insurance for Hong Kong workers, insurance has been closely integrated into our daily life.

The most fundamental purpose of buying insurance is to seek protection against the risk of accidents. Buying insurance stocks is a pure investment.

In 2018, the market was more and more optimistic about insurance stocks. Chinese Huatai, Soochow, Guotai Junan, and foreign investors Goldman Sachs Group, Bank of America Merrill Lynch and JPMorgan Chase & Co shouted one after another. Chief Zhang Yidong, who just won the first place in the "New Wealth" strategy, also took insurance stocks as his first choice in his speech.

Why does Daxing push insurance so hard? The main reason is the core assets and the positive market cycle. If ordinary investors want to understand the investment opportunities and risks of the insurance industry in 2018, it is very important to find the right angle and entry point. good

Which insurance company is better?

Which insurance company has the best products? There are different explanations from different angles, just like asking which researcher has the most accurate analysis, it is estimated that Huashan will not get an authoritative answer in ten years.

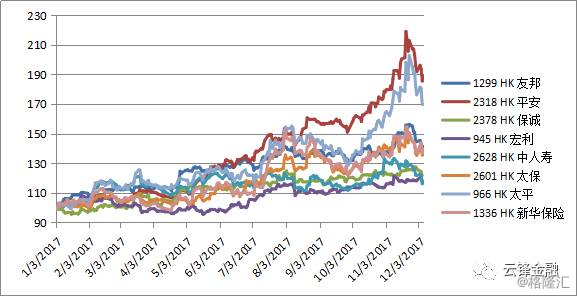

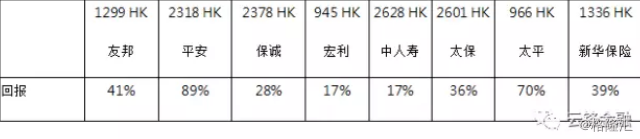

But which insurance company has performed best in the stock market this year? The data are fair. Among the insurance stocks listed in Hong Kong with a market capitalization of more than 50 billion this year, apart from PICC Property and Casualty, who does not do life insurance business, the biggest gains were Ping An Insurance and China Taiping, which not only far outperformed the Hang Seng Indices, but also significantly shaken off the gains of other insurance companies.

Photo: 2017 Hong Kong listed insurance stocks as of December 7 return Source: Bloomberg, Yunfeng Financial consolidation

What's the average? If you exclude the newly listed Zhong an and Asian Finance with a market capitalization of less than 10 billion, as well as Taiga Insurance, the Hong Kong insurance sector has risen an average of 43% this year, which is also higher than the Hang Seng Index benchmark.

Yang! Eyebrows! Puke! Angry!

But have insurance stocks always been so strong? The time period has been extended to three years, with the exception of Ping an, the stock price returns of most insurance companies are almost 10% at an annual rate, which is in an awkward position. The shares of Prudential plc (2378.HK) in the UK have barely risen in the past three years, and China Life Insurance Company Limited (2628.HK) has even lost 10%.

Fortunately, most insurers have a dividend policy, and the figure might look better if dividend returns are taken into account (note that H-share dividends need to be deducted from 10% dividend tax).

It can also be observed from the chart below that without taking into account the gains this year, the returns of most insurance stocks are not satisfactory, so many analysts are optimistic about the insurance sector because the spring of insurance is coming.

Picture: returns on Hong Kong listed insurance stocks in the past three years (as of December 7, 2017) Source: Bloomberg, Yunfeng Financial consolidation

The profit model of insurance companies

If you want to understand whether the spring of insurance companies is coming, it is very important to understand the profit model of insurance companies.

The traditional term "three differences" refers to the spread (the difference between the investment return and the pricing rate), the fee difference (the difference between the actual rate and the pricing rate) and the death difference (the difference between the death incidence or accident rate and pricing is the hypothetical probability of occurrence).

To put it more bluntly, the profit of the insurance company isThe profit from the sale of the insurance policy and the retained income after the policy is invested. The former includes the income brought by the operation of the company, such as death difference, fee difference, surrender fund and reserve release, while the latter is mainly interest rate spread.

Source: Dr.Finance

So for insurance companies, making money depends on two wheels rolling together--It is necessary to keep up with the investment income as well as the continuous expansion of the business.. Among them, the most profitable but also the riskiest often appear in the investment.

During the Lehman mini-debt crisis in 2008, AIG Group, the world's largest insurer, nearly collapsed because its subsidiary, AIG FP (AIG Financial Products Corp), lost a lot of money. AIG FP designed ultra-advanced credit default swap CDS products to guarantee higher debt, including corporate loans and personal home mortgages facing bubble bursting. After the outbreak of the Lehman crisis, AIG FP caused 28 billion dollars in losses to the parent company in 2008, and the group eventually survived with a bailout from the U. S. government.

Relatively speaking, the risk of operation will be much smaller.General insurance products, especially life insurance and serious illness insurance, are paid by installments and have no income at all for a certain period of time, or it is very rare for a certain period of time to have a large number of claims (such as war or nuclear explosion and other irresistible environmental factors are generally non-insurance regulations).

Even if there is an accident such as the explosion in Tianjin that year, the amount of claims is estimated to be about 3 to 10 billion yuan, which is only 1 to 2.6 per cent of the 380 billion yuan paid by property insurance in 2014. And some of the property insurance claims need to be accounted for for a year or even years, which has little impact on the business of insurance companies.

But the risks and benefits are relative, and it is difficult for insurance companies to achieve rapid business growth by relying on their operations-for example, a large number of customers surrender insurance and bring a lot of one-time benefits, or everyone who lives a thousand years old will never get sick. I know it can only be a pipe dream.The increase in the number of people insured and the increase in the number of insurance products purchased by a single customer are the core sources of business growth.

There will be some differences in the advantageous products of different companies.Take Ping An Insurance as an example, the growth rate of personal life insurance business in the past ten years is much higher than that of group insurance and bank insurance business, accounting for the absolute majority of the total income. The growth rate of personal life insurance business accelerated in 2016, reaching an all-time high.

According to the company's annual report, the number of new customers reached 38.42 million in 2016, up 25 per cent from 30.73 million in the same period in 2015. But by the mid-term report of 2017, the growth rate of individual customers had fallen sharply to 9.3% from a year earlier.

Picture: Ping An Insurance 2318.HK income composition (unit RMB 10,000), source: wind, Yunfeng Financial arrangement

But it is worth noting that, unlike the general consumer industry, which can increase prices to increase gross margins, it is almost difficult for insurance companies to raise prices significantly. For insurance companies, industry barriers are not as strong as imagined. If a company's product premium increases, it often means a decline in market share for insurance companies.

The market has a large space for development, but it is a trend that the strong will always be strong.

From 2003 to 2016, the average annual growth rate of insurance premium income in mainland China was 17.32 per cent, much higher than the compound growth rate of 11.05 per cent of per capita household disposable expenditure of urban residents. The main reason is that the demand for insurance continues to break out with the rise of middle-income groups and the aging population. The latest trend is that insurance products, which have both consumer protection and financial attributes, will gradually become consumer substitutes.

The increasing trend of population aging provides an endogenous environment for the development of the industry. From 2003 to 2016, the proportion of people aged 65 and above increased from 7.30% to 10.80%, according to relevant data. With reference to overseas development experience, the aging population will increase the insurance demand, which is an important cornerstone of the development of the insurance industry.

Source: insurance Application Research Institute

The depth of insurance in China still lags behind the international level. According to the data of China Industrial Information Network in 2016, premiums account for 4.16% of GDP, but there is still a considerable distance compared with developed countries.

Driven by the gradual rise of Internet insurance and the increase in middle-class and elderly customersInsurance depthIt is expected to accelerate in the next few years.,Corresponding to the insurance market is large enough room for development.At the same time, large insurance companies have channel advantages (mainly forming individual insurance channel advantages that small and medium-sized insurance companies are difficult to establish) and brand advantages, and can sell insurance policies to obtain premiums at a lower debt cost.

Source: iResearch Information

The advantage of small insurance companies to break out is to design more special products and adopt more flexible strategies in investment choices. But risks and benefits coexist, and it is fair for both retail investors and insurance companies.

In recent years, some small and medium-sized insurance companies have frequently raised their cards and used the money raised by insurance channels represented by universal insurance to operate on a large scale in the financial market, which has aroused heated discussion in the market and more stringent supervision.

With the notice on standardizing medium-and short-term life insurance products issued by the CIRC, some radical private insurance companies are facing the reorganization of business structure and investment style, which indirectly reduces the competitive advantage with large insurance companies. Therefore, from the investment point of view, large domestic insurance companies have a better business environment.

Raising interest rates is good for insurance stocks

If the growth in business basically ensures that one wheel of insurance stocks rolls up, the global cycle of raising interest rates will help the other even more. For insurance funds, especially for the funds of large insurance companies, the investment style pursues assets with a higher safety level, and the investment targets of a large amount of premium income are mainly bonds and monetary products. If the market enters the interest rate-raising cycle, government bonds and corporate bonds are forced to raise interest rates to remain attractive enough, and the return on new investments by insurance companies will also rise.

If a further explanation is allowed, insurance products will generally have a guaranteed return at the time of design, in addition to a floating non-guaranteed dividend. In the low-interest cycle, the yield on many high-rated bonds is only about 3%, and the yield on China's 10-year treasury bonds has fallen below 3%. If the guaranteed return of insurance products is only 3%, the return will become a chicken rib for customers. If dividends are forced to rise higher, it will erode the investment returns of insurance companies.

Picture: Chinese 10-year bond yield source: Bloomberg

On the contrary, when the market enters the interest rate hike cycle, interest rates can rise to 6% or even 8% at any time, leaving insurance companies with more room for spreads. At the same time, raising interest rates is a big killer of the stock market and the property market. If the dividend of insurance products can be better, it can also increase the attractiveness of the products to a certain extent, thus attracting more customers to take out insurance.

Is the cycle of raising interest rates clear? The path of the United States and the Federal Reserve is already very clear, considering that Trump's tax reform policy will also attract money back to some extent, and market expectations of China's "passive interest rate hike" have increased. Sun Guofeng, director of the Institute of Finance of the people's Bank of China, said on December 5: "the central bank cannot give the market long-term low interest rate expectations to prevent the market from taking excessive risks to force the central bank." He also pointed out that the international coordination of monetary policy helps to guard against the risk of cross-border capital flows.

Picture: changes in US benchmark interest rates (yellow line is Fed forecast)

In a relatively clear macro context, everyone has shouted to buy some insurance stocks, I believe it is not difficult to understand (of course, the chance of shouting wrong is also relatively small).

Investors may need to think more about whether investors should buy Ping an or HSBC or both if interest rate hikes are also good for bank stocks, and Ping An Insurance recently raised his shares and HSBC Holdings PLC's shares reached HK $77 billion to become the second largest shareholder.

Disclaimer:

This article is authorized by Yunfeng Financial Group Co., Ltd. to be published on this platform and does not constitute specific investment recommendations. Investors are invited to note that investment involves risks.