Author: Zhu Ang

Introduction:2017 is coming to an end, and the best-performing sector in S & P this year is technology stocks. Tencent and BABA of China and Amazon.Com Inc, Facebook Inc, Netflix Inc and Alphabet Inc-CL C of the United States have all performed very well. At the end of the year and the beginning of the year, we also need to look forward to 2018 and think about where the relatively most promising companies will be in the future. Today, I would like to share with you one of the Internet companies I am most optimistic about next year: Facebook Inc.

First of all, I am more sure of one thing: the network effect of the Internet industry will continue to promote Qiangzheng Hengqiang. Over the past year, the big Internet giants have been able to maintain faster growth. Tencent, BABA and Facebook Inc all have profit growth rates of 30-50%, and the number of users continues to expand. And small Internet companies have not only seen a decline in the number of users, profit growth is also difficult to compete with the big Internet giants. The characteristics of elephant dancing in the Internet industry are in fact the same as the nature of all economic models.

After the consumer dividend period, it must be the monopoly of the giant.

In our physical life, food and beverage, cars, home appliances, medicine, energy and so on are all monopolized by several big companies. And the Internet is even better than physical enterprises in terms of monopoly. Because the current policy for the regulation of Internet monopoly is relatively loose. For users, the choice must be to find a platform with network effect. Whether the goods of e-commerce are complete, whether the price is low, whether the delivery service is convenient enough, whether the data of the search engine is complete, even whether the brand has credibility, whether there are enough friends of social applications, whether it is convenient to use, and so on. The result of this network effect is that the more people use it, the more people are willing to use it.

Before there is no new technology battlefield, the status of these traditional Internet giants can hardly be shaken. Every major technological change in the past few years has opened up a new battlefield.

The earliest computers were actually mainly tools used by the military. With the end of the Cold War, it began to popularize to the popular market.

At that time, it was accompanied by the research and development of routers and chips, which brought the first bubble of science and technology stocks. The second mobile Internet revolution, also based on the 3G network construction, superimposed Apple Inc's innovation on smartphones. The next technology battlefield may be the wave of the Internet of things brought about by the large-scale popularity of 5G and the improvement of chip performance. But judging from the time schedule, it seems that there are still a few years to go. At present, these big Internet giants will only continue to consolidate their competitive advantage. On the contrary, after the end of the traffic dividend, it becomes more and more difficult for small and medium-sized Internet enterprises to survive.

Secondly, I will make an industry comparison to see which area of Internet application is the most valuable, as well as the differences and competitive advantages between them.

Let's take a look at the four heavenly kings of FANG in the United States:They correspond to social networking, e-commerce, Internet TV and search engines.

We can rule out Internet TV first. Although Netflix Inc has very strong barriers in the United States, the global expansion of Internet TV will be more difficult than other applications. And the ceiling of the market will be relatively low. So what's left are social app Facebook Inc, e-commerce giant Amazon.Com Inc, and search king Alphabet Inc-CL C. Of course, the current three giants based on their traffic entry, have derived a lot of new business, including cloud computing, big data, artificial intelligence and so on.

But whether it is the PC Internet era, or the mobile Internet era, one of the problems solved is the connection. The core of the Internet is the connection between people. From this point of view, social apps will be more valuable. Facebook Inc is the deepest moat among the four kings of FANG.

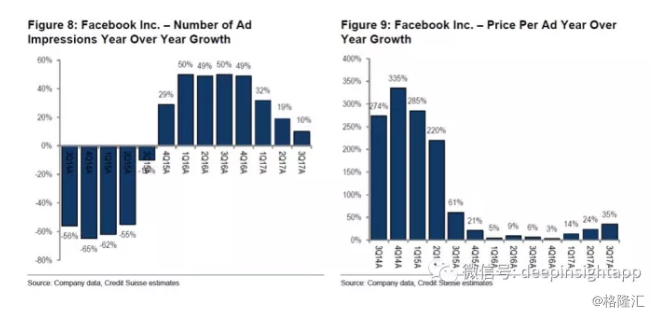

Looking at Facebook Inc's recent financial report, revenue in the third quarter increased by 47 per cent to $10.3 billion. The number of monthly active users reached 2.07 billion, an increase of 3% month-on-month and 16% year-on-year. The number of daily active users also reached 1.37 billion, an increase of 3.2 per cent month-on-month. Facebook Inc's ratio of daily active users to monthly active users has been stable at 66 per cent in the past three quarters. From the perspective of income structure, Facebook Inc basically still relies on advertising, and advertising revenue has reached 10.1 billion US dollars, contributing almost all of the income. With the outbreak of mobile traffic, the exposure and price of advertising are increasing. For advertisers, Facebook Inc's user data is becoming more and more accurate, providing the most cost-effective advertising platform. And from the perspective of advertising revenue structure, mobile advertising revenue accounts for the majority, accounting for 88%.

Judging from Facebook Inc's layout, Zuckerberg is not more concerned about cash.But to improve user stickiness and stay for a long time of product form.

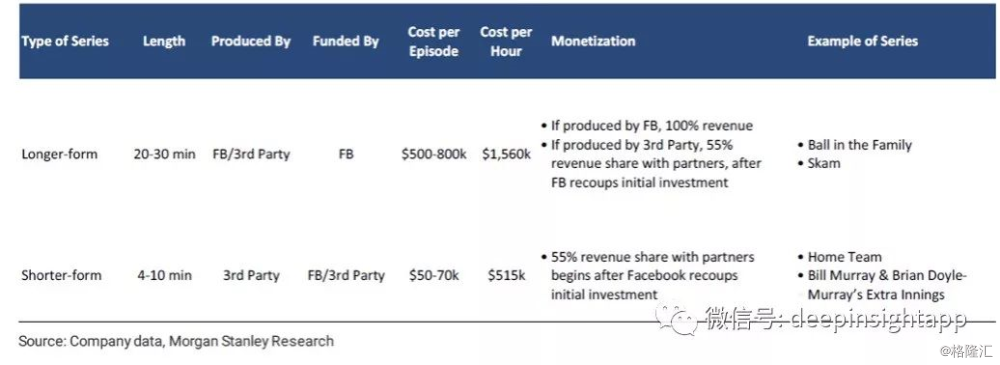

The focus of Facebook Inc's product form in the past few years is video.In fact, the release of video content Facebook Inc began to transform to a new model. In the past, the video content of this kind of social networking site was more suitable for short videos, such as the few-minute videos on Weibo Corp in recent years. Some of these videos are from UGC and some are from PGC. In fact, the earliest social videos were mainly based on UGC, and people would record their own videos and spread them. The first to do this model is Youtube, which was later acquired by Facebook Inc. In recent years, however, Netflix has told the market that head boutiques are worth more. Video does not lie in many, but in the well-produced content. As a result, Facebook Inc recently began to produce higher-quality videos through third parties. According to a research report by Morgan Stanley, there are two kinds of videos made by Facebook Inc:

1. A long video of 20-30 minutes.Similar to American TV series, the cost per episode is $50 to $800000.

2. 4-10 minute short video, developed by a third party.55% of advertising revenue will be distributed to third parties. It costs $50, 000 to $70, 000 to produce a single episode.

We can see that the production cost of Facebook Inc's long video is between $100 and $1.6 million per hour, which is still different from the top American TV series with a cost of $10 million per hour, such as the Song of Ice and Fire. Of course, it's not cheap. So 2018 can be seen as a test of Facebook Inc's homemade videos, and they may also sign the right to broadcast some sports games. If it works well, it may be pushed forward on a large scale in the future.More importantly, in Facebook Inc's function, there is already a video search function. Zuckerberg hopes to greatly extend the stickiness and length of stay of users through video.

Finally, let's think about one more question: Facebook Inc or Tencent, who is more valuable?

From a medium-and long-term point of view, I always think that Facebook Inc is worth more than Tencent. Facebook Inc has three major product matrices:Facebook,Instagram, Whatsapp .Its daily active users add up to more than 3 billion. Surpassed Tencent's Wechat and Mobile QQ. More importantly, Facebook Inc is a truly global social application, and Tencent is also a Chinese localized social application.

Behind social applications is cultural output.We want to see what Americans are doing and what American stars are saying, because the United States has exported its strong culture in the past 20 years of globalization. However, Wechat will not be able to achieve truly global social applications in the next few years due to its lack of cultural output. Do not care too much about the liquidity, as long as there are users and stickiness, the expansion of liquidity is only a matter of time. This also means that the market value of Facebook Inc should not be lower than that of Tencent in the long run. Of course, in our study of Tencent, we also said that the market capitalization of penguins still has room to double in the next few years.

Finally, let's look at it from the perspective of valuation. In the following picture, we can see that Facebook Inc's current valuation is only about 27 times, much lower than the historical average of 35 times. Performance should maintain growth of more than 30% in the next few years.