① COSCO Haineng's foreign trade tanker business had a gross profit of 715 million yuan in the third quarter and 723 million yuan for China Merchants; ② COSCO Haineng had 97 foreign trade tankers, including 47 VLCCs plus 5 (leasing); China Merchants Steamship had 57 foreign trade tankers, of which 52 were VLCCs; ③ It is difficult for oil tanker shipbuilding to have a wave of orders. The oil transport market will gradually rise in prosperity in the next two years. Crude oil and refined oil products complement each other.

Financial News Agency, October 30 (Reporter Hu Haoqiong)As major domestic oil transportation leaders, COSCO Marine (600026.SH) and China Merchants Shipping (601872.SH) announced their Q3 results one after another. Compared to that, who can be superior?

Some have larger fleets, and some are more profitable

Looking at the main financial indicators of the two companies, in the first three quarters of this year, COSCO Hyneng achieved operating income of 16.535 billion yuan, an increase of 33.37% over the previous year; net profit attributable to shareholders of listed companies was 3,714 billion yuan, an increase of 480.49% over the previous year. China Merchants Shipping achieved operating income of 19.023 billion yuan, a year-on-year decrease of 11.85%; net profit attributable to shareholders of listed companies was 3.758 billion yuan, a year-on-year decrease of 2.81%.

Among them, in the third quarter, COSCO Marine Energy achieved operating income of 4.959 billion yuan, an increase of 1.52% over the previous year, and net profit of 908 million yuan, an increase of 88.69% over the previous year. China Merchants Shipping achieved operating income of 6.032 billion yuan, a decrease of 23.17% over the previous year; net profit of the mother was 988 million yuan, an increase of 1.13% over the previous year.

However, it is not possible to completely clearly judge the dominant position of the two from the main financial indicators. COSCO Hyneng's main financial indicators include LNG business, while China Merchants Shipping includes businesses such as transportation, steam rolling ships, and bulk transportation. Therefore, it is more intuitive from the perspective of foreign trade tanker business alone.

According to the announcement and reports from the Financial Association, COSCO Haineng's foreign trade oil transportation business achieved gross profit of 3.489 billion yuan in the first three quarters of 2023, an increase of 3681% over the previous year, of which the gross profit for the third quarter was 715 million yuan. In terms of China Merchants Shipping, the tanker business achieved gross operating profit of 723 million yuan and net profit of 533 million yuan in a single quarter in the third quarter.

Looking further at the fleet structure, according to the reporter's understanding, up to now, COSCO Marine has 97 foreign trade tankers, of which 47 are VLCC (owned) +5 (leased); China Merchants has 57 foreign trade tankers, including 52 VLCCs. Although COSCO Marine Energy has a larger fleet, its operating profit is not as good as that of China Merchants. The competition between the two seems to have already been determined.

Based on this, China Merchants Shipping also announced a name change. China Merchants Shipping said in the announcement that in order to reflect the company's oil and gas and dry dispersion business and medium- to long-term strategic development vision, the original “China Merchants Energy Transportation Co., Ltd.” was changed to “China Merchants Shipping Co., Ltd.”, keeping the company's Chinese abbreviation and stock abbreviation “China Merchants Shipping” unchanged.

Capacity growth is limited, and the market is still in an upward cycle

Looking back at the oil transport market, as stated in China Merchants Shipping's financial report, Saudi Arabia and Russia voluntarily cut production by 1 million b/d and 300,000 b/d respectively in the third quarter on the basis of the original OPEC+ production reduction agreement, and announced in early September that the additional production reduction plan was extended until the end of the year, which directly led to a marked contraction in the VLCC Middle East market shipment volume and weakening the spot market; after mid-July, Russia's Ural oil broke through the price limit, and some small and medium-sized tankers (Suezmax, Aframax) returned to regular trade, leading to excess capacity supply in the Atlantic market, small and medium-sized tankers Prices have dropped sharply, The unit price advantage of VLCC for small and medium-sized tankers in the western market temporarily disappeared; at the same time, the WTI arbitrage window was reduced due to oil prices. Demand for oil tankers in the third quarter was concentrated during the off-season.

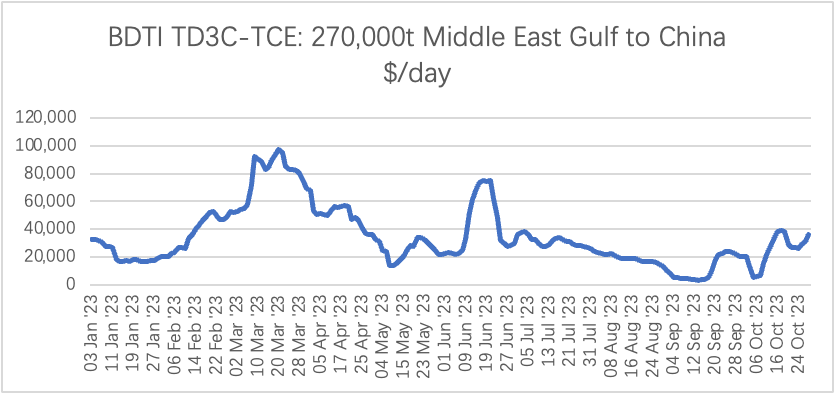

This can also be seen from the performance of the BDTI TD3C-TCE. However, based on still being optimistic about the future market, many shipowners took advantage of the off-season and market downturn to concentrate docks to repair and install desulfurization towers, partly to hedge against supply pressure.

BDTI TD3C-TCE chart from this year to October 27 (Source: Baltic Exchange)

However, since the fourth quarter, the oil transport market has begun to show a “thriving” trend. Some industry insiders told the Financial Services Association reporter that with the peak season in the fourth quarter approaching, shipments to the Middle East and the US Gulf are likely to exceed expectations. Combined with the US beginning to sanction two tankers that ship Russian oil at excessive prices, the market expects that the efficiency of the shadow fleet will decrease as a result, and tanker capacity will be tightened.

How is this year's oil operation compared to last year? According to a report obtained by a reporter from the Financial Services Association, in reality, the oil transport market conditions last year and this year and beyond are two different things. Oil transportation was booming from the middle to the second half of last year. The root cause was the rush to buy energy products in anticipation of the Russian-Ukrainian war and sanctions. Beginning this year, it is a real historic opportunity for oil transportation — the actual restructuring of the energy supply chain led by traditional industrial countries represented by the European Union and the US. This is a real big game of chess that will continue for a long time.

In terms of capacity, according to this report, tanker owners are not affected by the “winner-take-all” law in the container ship market, and their impulse for centralized and large-scale ship bookings has always been limited, compounded by the lack of decision-making information mentioned earlier, so it is difficult to see a rush of orders.

As for the future prospects of the oil transportation market and which market is better for crude oil or refined oil products, the above minutes show that the oil transportation market in the next two years should be a situation where prosperity gradually rises, and crude oil and refined oil products complement each other. “As refining and chemical production capacity becomes more centralized, the number of tonnautical miles of distribution routes for supply and marketing has been lengthened. Judging from past experience, there is a rhythm of “crude oil first, then refined oil”. This is a natural transmission process in the industrial chain from raw materials to the consumer side.