Pengana Capital Group (ASX:PCG) investors are sitting on a loss of 55% if they invested five years ago

We think intelligent long term investing is the way to go. But no-one is immune from buying too high. For example, after five long years the Pengana Capital Group Limited (ASX:PCG) share price is a whole 65% lower. That is extremely sub-optimal, to say the least. And we doubt long term believers are the only worried holders, since the stock price has declined 39% over the last twelve months. The falls have accelerated recently, with the share price down 10% in the last three months. However, one could argue that the price has been influenced by the general market, which is down 5.7% in the same timeframe.

It's worthwhile assessing if the company's economics have been moving in lockstep with these underwhelming shareholder returns, or if there is some disparity between the two. So let's do just that.

View our latest analysis for Pengana Capital Group

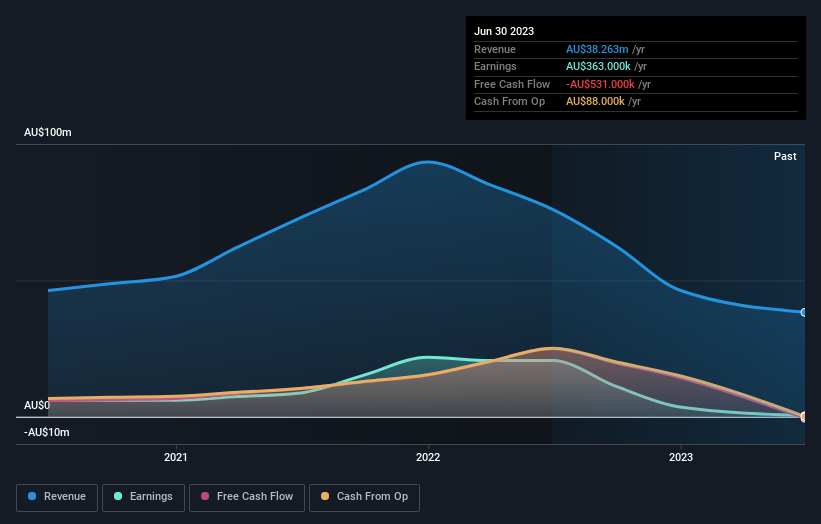

We don't think that Pengana Capital Group's modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

Over five years, Pengana Capital Group grew its revenue at 8.0% per year. That's a fairly respectable growth rate. The share price return isn't so respectable with an annual loss of 11% over the period. It seems probably that the business has failed to live up to initial expectations. That could lead to an opportunity if the company is going to become profitable sooner rather than later.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

This free interactive report on Pengana Capital Group's balance sheet strength is a great place to start, if you want to investigate the stock further.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. As it happens, Pengana Capital Group's TSR for the last 5 years was -55%, which exceeds the share price return mentioned earlier. This is largely a result of its dividend payments!

A Different Perspective

Investors in Pengana Capital Group had a tough year, with a total loss of 37% (including dividends), against a market gain of about 7.0%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 9% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Pengana Capital Group better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with Pengana Capital Group , and understanding them should be part of your investment process.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.