Source: Wall Street News

The main reason behind the sharp rise in US bond yields is probably the rise in term premiums. Analysts generally believe that the sharp rise in term premiums in recent months is inseparable from the imbalance between supply and demand for US Treasury bonds. However, since the US is still facing a peak in the supply of long-term treasury bonds in the fourth quarter, it may be difficult to see signs of a decline in yield this year.

The 10-year US Treasury yield, known as the “anchor of global asset pricing,” hit 5%. Huge uncertainty envelops the world. It is clear that the market expects the Fed's interest rate hike to be close to the end. Why will US bond yields continue to rise?

A number that cannot be directly observed has become a possibility that Wall Street keeps on mentioning --The “term premium” is soaring.

Theoretically speaking, 10-year US Treasury yields can be broken down into future short-term interest rate expectations plus term premiums (term premiums).The so-called term premium compensates investors for the risk of holding long-term bonds.

In recent weeks, the debate surrounding term premiums has intensified. Some financial models suggest that term premiums are rising rapidly, which has largely driven the recent surge in US long-term bond yields. You need to know that in the past ten years, 10-year US bond term premiums have basically been below zero value (temporarily corrected in March-June 2021)In recent days, the 10-year US Treasury term premium has turned positive, for the first time since June 2021.

According to ACM model data released by the New York Federal Reserve, as of October 6, of the 107 bp increase in 10-year US Treasury yields from the low of July 13, the term premium contributed 100 bps, while short-term policy interest rate expectations only contributed 7 bp — confirming that the market believes that the Fed has limited room to continue raising interest rates.

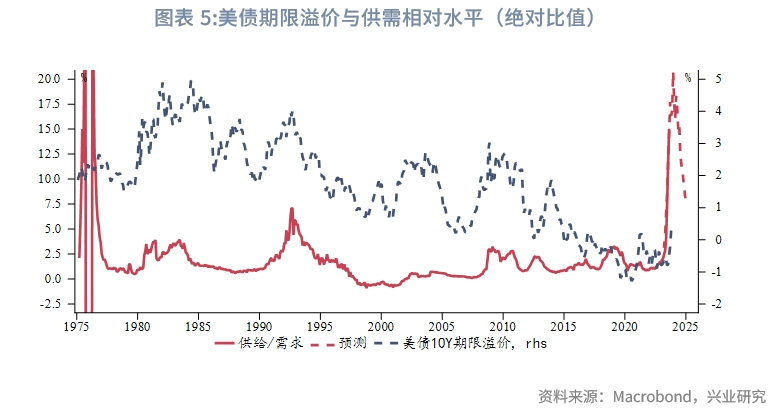

Analysts generally believe that the sharp rise in term premiums is related to the imbalance between supply and demand for US Treasury bonds, and since the US is still facing a peak in the supply of long-term treasury bonds in the fourth quarter, it may be difficult to see signs of a decline in yield this year.

What is a term premium?

Simply put,A “term premium” refers to compensation for losses caused by risks that investors may encounter.

The understanding of term premiums is mainly divided into three aspects: first, the level of inflation and the uncertainty of future monetary policy and currency; second, how monetary policy choices affect economic prospects; and third, the pure relationship between supply and demand for treasury bonds.

Well, that is to say, the current “term premium” is soaring,This means that in the eyes of investors, US economic growth, inflation, and supply and demand for treasury bonds have all changed unexpectedly, and have become uncertain risk factors.

On the one hand, many economic data previously released suggest that the US economy is still overheated, and expectations of the Fed's interest rate hike are heating up. Therefore, the market has to re-examine the Fed's policy path of “staying at a higher level for a longer period of time” and reprice the medium- to long-term uncertainty caused by this. On the other hand, it may be due to the continuing imbalance between supply and demand for US bonds,When the influx of US debt into the market greatly exceeds demand, it will drive up yields.

Is the imbalance between supply and demand the main cause?

Some analysts believe that for the market, marginal changes in supply and demand are more important. Because the US Treasury is aggressively issuing treasury bonds, there is too much supply, which is why yields have skyrocketed.

Societe Generale Securities research shows thatThere is a high correlation between the relative level of supply and demand and term premiums. Due to the surge in the size of US debt in recent years and the trade deficit continuing to narrow, there is currently a relative oversupply.

After the US debt ceiling and the new budget law were adjusted at the beginning of June this year, the size of US debt ushered in an epic explosion. After breaking through 32 trillion US dollars over a period of 8 months, it only took 3 months since then to reach a “new high” of 33 trillion US dollars.

Guotai Junan pointed out,The “proliferation” of US debt on the supply side has broken the original balance between supply and demandIt also further amplified the market's concerns about the rise in America's medium- to long-term inflation center. The yield on US bonds of various matures soared rapidly. In the two periods from the beginning of June, the end of September, and the beginning of October, when US bonds were greatly inflated,The 10-year US Treasury yield increased by 20 bps and 50 bps, respectively.

At the regular refinancing meeting in July 2023, the US Treasury raised the estimated net issuance scale of treasury bonds for the third and fourth quarters of this year to more than 1 trillion US dollars and 852 billion US dollars respectively. This is the second highest net issuance scale for a single quarter since this century. It significantly exceeded market expectations and had a “fiscal impact” on the market.

At the end of September, the US two houses also passed the Short-Term Financing Act, further increasing the supply scale of US debt.

However, the demand side has further exacerbated the imbalance between supply and demand for US bonds. While the supply of US bonds has increased markedly, the Federal Reserve, as the most important holder of US debt, has continued to shrink and sell treasury bonds since June 2022. Coupled with the European Central Bank's continuous interest rate hikes and the Bank of Japan's expected withdrawal from negative interest rates, demand for US bonds has declined marginally from both domestic and overseas investors, which has become an important factor driving the recent rise in maturity premiums on US bonds, which in turn boosts long-term interest rates on US bonds.

How to estimate term premiums?

The calculation of term premiums has always been a complicated issue, and there is no perfect way to know what investors think about future interest rates.

The easiest method is to compare treasury bond yields with future interest rate predictions from survey data in the market. Currently, the most popular calculation method is calculation based on the New York Federal Reserve's ACM model. This model uses treasury bond yields of different matures to predict future short-term interest rates, effectively finding a pattern of their relationship within a few decades:

Looking at the TSY = R+TP framework, the risk-neutral interest rate R characterizes short-term US bond forward interest rate path expectations, which mainly reflect expectations of monetary policy.

Term premium TP is characterized by the risk premium required for the long-term end compared to the rolling short-term interest rate. It reflects risk preferences, including growth risk premiums, inflation risk premiums, and liquidity risk premiums.

According to media analysis, the data output from this term premium model has never stopped being debated in the economics community. Especially after 2016, when the term premium was negative, investors lost their minds. This did not match normal market expectations and experience, and also caused the current term premium to return to a positive value once again sparking controversy.

What do Wall Street and Fed officials think?

Dallas Fed Chairman Lorie Logan said that the signal conveyed by the term premium model made her unwilling to raise interest rates again this year. She believes that an increase in term premiums can cool the overheated economy to a certain extent, which reduces the need for the Fed to further tighten monetary policy:

The increase in term premiums has played a significant role in recent changes in the yield curve, although there is uncertainty about its size and durability.

Logan didn't explore in depth what exactly is driving up the term premium. However, according to Wall Street, when using the term premium model as an explanation, the rise in term premiums is mainly due to a growing federal budget deficit.

Blake Gwinn, head of US interest rate strategy at RBC Capital Markets, said:

In recent months, the US Treasury has not only increased the size of its borrowing but also increased the size of its longer-term bond auctions, which has exceeded investors' expectations. The rise in the relevant term premium is due to changes in supply and demand dynamics.

Will treasury bond yields fall back in the fourth quarter?

According to the analyst,Analyzing future treasury bond yields from the three aspects of soaring term premiums, we may not be able to see any signs of a decline in US long-term treasury bond yields this year. The main reasons are:

1) The US still faced a peak in the supply of long-term treasury bonds in the fourth quarter.According to the quarterly refinancing plan announced by the Ministry of Finance, the planned net financing amount for treasury bonds for the fourth quarter was 852 billion US dollars, of which the net financing amount for medium- to long-term treasury bonds (2 years and above) was 338.55 billion US dollars, up from 177.97 billion US dollars in the third quarter. In particular, November is the peak of seasonal issuance of 10-year, 20-year, and 30-year treasury bonds.

2) The probability of a drastic reduction in fiscal spending is low, and the resilience of the US economy is still supported.A major source of the resilience of the US economy in this round of interest rate hikes is the lack of coordination between fiscal policy and monetary policy. As of September, the US fiscal deficit accounted for 7.6% of GDP, which is at the 88% quantile level since the 80s of the last century. With strong fiscal support, the probability that the US economy will weaken rapidly is relatively low.

3) Government governance, high deficits, and debt problems may have once again aroused market attention, increasing market premium requirements for long-term treasury bonds.Currently, Congress has passed a 45-day temporary funding bill, which has enabled the US government to avoid shutting down. However, in mid-November, the two parties will once again vote on the funding bill for the new fiscal year. Deterioration in US government governance, high deficits, and debt issues may once again influence market sentiment, putting upward pressure on term premiums.

Editor/Somer